by admin | Jan 31, 2017 | Health Plan Benchmarking

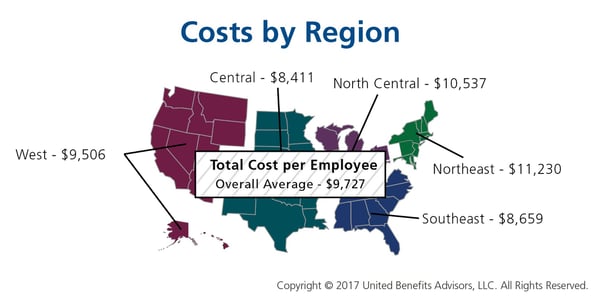

Many employers benchmark their health plan against carrier provided national data. While that is a good place to start, regional cost averages vary, making it essential to benchmark both nationally and regionally—as well as state by state. For example, a significant difference exists between the cost to insure an employee in the Northeast versus the Central U.S.—plans in the Northeast continue to cost the most since they typically have lower deductibles, contain more state-mandated benefits, and feature higher in-network coinsurance, among other factors.

Drilling down even more, comparing yourself to your industry peers can tell a very different story.

Consider a manufacturing plant in Georgia that offers a PPO. Its premium cost for single coverage is $507 per month. Compare this with the benchmarks for all plans and you can see that it is $2 per month less than the national average. When compared with other PPOs in the Southeast region, this employer’s cost is actually $2 more than the average. This employer’s cost appears to be higher or lower compared with national and regional benchmarks, depending on which benchmark is used. Yet this employer’s cost is actually higher than its closest peers’ costs when using the state-specific benchmark, which in Georgia is $468. Bottom line, this employer’s monthly single premium is actually $39 more than its competitors in the state.

As our CEO, Les McPhearson, recently stated, “Benchmarking by state, region, industry, and group size is critical. We see it time and time again, especially with new clients. An employer benchmarks their rates nationally and they seem at or below average, but once we look at their rates by plan type across multiple carriers and among their neighboring competitors or like-size groups, we find many employers leave a lot on the bargaining table.”

By RJ Nelson, Originally Published By United Benefit Advisors

by admin | Jan 18, 2017 | ACA, Compliance, ERISA

Proposed regulations for revising and greatly expanding the Department of Labor (DOL) Form 5500 reporting are set to take effect in 2019. Currently, the non-retirement plan reporting is limited to those employers that have more than 100 employees enrolled on their benefit plans, or those in a self-funded trust. The filings must be completed on the DOL EFAST2 system within 210 days following the end of the plan year.

What does this expanded number of businesses required to report look like? According to the 2016 United Benefit Advisors (UBA) Health Plan Survey, less than 18 percent of employers offering medical plans are required to report right now. With the expanded requirements of 5500 reporting, this would require the just over 82 percent of employers not reporting now to comply with the new mandate.

While the information reported is not typically difficult to gather, it is a time-intensive task. In addition to the usual information about the carrier’s name, address, total premium, and payments to an agent or broker, employers will now be required to provide detailed benefit plan information such as deductibles, out-of-pocket maximums, coinsurance and copay amounts, among other items. Currently, insurance carriers and third party administrators must produce information needed on scheduled forms. However, an employer’s plan year as filed in their ERISA Summary Plan Description, might not match up to the renewal year with the insurance carrier. There are times when these schedule forms must be requested repeatedly in order to receive the correct dates of the plan year for filing.

In the early 1990s small employers offering a Section 125 plan were required to fill out a 5500 form with a very simple 5500 schedule form. Most small employers did not know about the filing, so noncompliance ran very high. The small employer filings were stopped mainly because the DOL did not have adequate resources to review or tabulate the information.

While electronic filing makes the process easier to tabulate the information received from companies, is it really needed? Likely not, given the expense it will require in additional compliance costs for small employers. With the current information gathered on the forms, the least expensive service is typically $500 annually for one filing. Employers without an ERISA required summary plan description (SPD) in a wrap-style document, would be required to do a separate filing based on each line of coverage. If an employer offers medical, dental, vision and life insurance, it would need to complete four separate filings. Of course, with the expanded information required if the proposed regulations hold, it is anticipated that those offering Form 5500 filing services would need to increase with the additional amount of information to be entered. In order to compensate for the additional information, those fees could more than double. Of course, that also doesn’t account for the time required to gather all the data and make sure it is correct. It is at the very least, an expensive endeavor for a small business to undertake.

Even though small employers will likely have fewer items required for their filings, it is an especially undue hardship on many already struggling small businesses that have been hit with rising health insurance premiums and other increasing costs. For those employers in the 50-99 category, they have likely paid out high fees to complete the ACA required 1094 and 1095 forms and now will be saddled with yet another reporting cost and time intensive gathering of data.

Given the noncompliance of the 1990s in the small group arena, this is just one area that a new administration could very simply and easily remove this unwelcome burden from small employers.

By Carol Taylor, Originally published by United Benefit Advisors – Read More