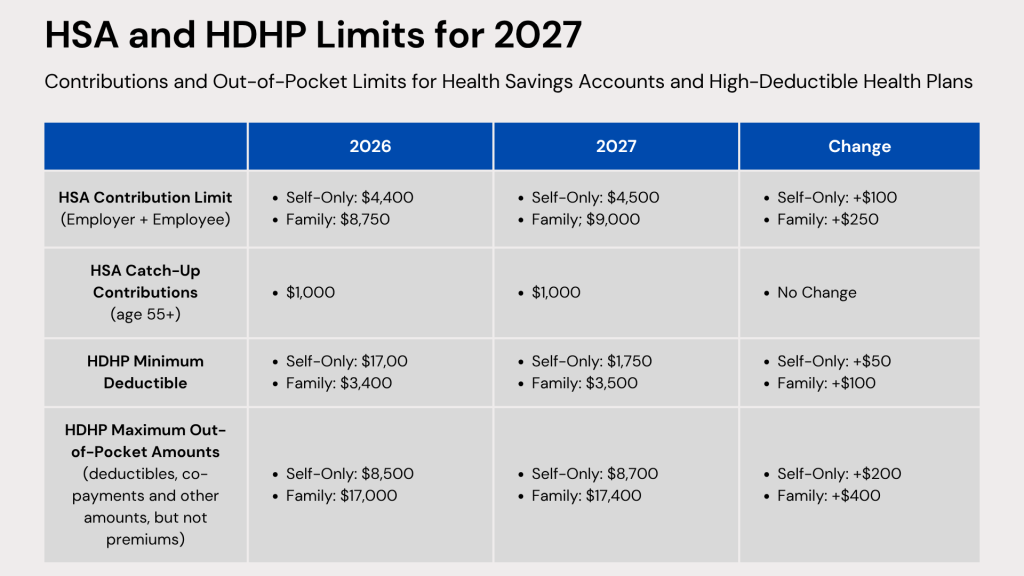

On May 29, 2026, the IRS issued Revenue Procedure 2026-24, which sets the inflation-adjusted limits for health savings accounts (HSAs) and high deductible health plans (HDHPs) for 2027.

The updated limits address:

The maximum allowable HSA contribution

The minimum deductible required for HDHPs

The maximum out-of-pocket expenses permitted for HDHPs

Each of these limits differs depending on whether the coverage is for an individual or a family under an HDHP.

Exhausted employees do not innovate, and burned-out managers cannot build strong, thriving cultures. For nearly a decade, corporate wellness has been siloed into superficial initiatives: wellness apps, awareness weeks, or reactive crisis counseling.

Human sustainability recognizes that employee health, energy, resilience, and mental capacity are finite resources. Like any organizational asset, these can either be supported and replenished or overused until they are exhausted.

Today’s workforce is under growing strain. Many employees come to work carrying significant personal burdens, including financial pressure, caregiving responsibilities, trauma, chronic illness, or mental health challenges such as anxiety, loneliness, and burnout. Others are navigating menopause, neurodiversity, addiction recovery, or persistent sleep issues.

A useful analogy is that of a backpack. Every employee arrives at work carrying one, filled with their health, confidence, coping abilities, relationships, financial security, optimism, and resilience. The heavier that backpack becomes, the harder it is for individuals to perform effectively, engage fully, and maintain positive workplace relationships.

In this sense, employee wellbeing and productivity are inseparable.

When workplace pressures overload an employee’s personal resources, the economic and operational fallout is severe:

Economic Inactivity: Long-term sickness has driven millions of individuals out of the global workforce, costing economies hundreds of billions annually in lost productivity and healthcare strains.

Public Health Risks: Chronic workplace stress is a major public health hazard, contributing heavily to cardiovascular disease and severe psychiatric injuries.

Corrosive Workplace Environments: While “good work” provides structure, identity, and purpose, poorly structured work environments, marked by understaffed teams and overextended management, actively damage organizational stability.

Making Human Sustainability a Strategic Priority

Organizations seeking sustainable performance must place human sustainability at the center of their strategy.

1. Elevate Human Sustainability to a Board-Level Issue

Businesses routinely monitor financial performance, operational efficiency, customer outcomes, and risk exposure. Yet few measure workforce depletion with the same level of attention. Leaders should be asking:

How healthy is our workforce?

Where are the greatest pressure points?

What factors are driving stress?

Which teams are carrying unsustainable workloads?

What challenges are managers facing?

What is the organizational cost of human depletion?

If people are truly an organization’s greatest asset, safeguarding their sustainability must be viewed as a core leadership responsibility.

2. Shift from Reactive Wellbeing to Preventative Design

The most successful organizations are not relying on wellbeing perks alone; they are redesigning work itself. This includes strengthening leadership capability, improving role clarity, managing workloads effectively, fostering psychological safety, increasing autonomy and flexibility, promoting inclusion, and equipping managers with the support they need.

Research consistently shows that organizational and cultural interventions have a far greater impact on reducing stress than isolated wellbeing initiatives.

3. Develop Managers as Human Sustainability Leaders

Managers play a critical role in shaping employee experience. When managers are disengaged, the impact is felt across entire teams.

Managers do not need to become counselors, but they do need the skills to lead people effectively. This includes building capability in psychological safety, stress prevention, difficult conversations, early intervention, conflict resolution, inclusive leadership, and creating healthy performance cultures.

Investing in manager development not only improves wellbeing outcomes but also strengthens engagement, productivity, and overall organizational performance.

The Future Belongs to Human-Centered Organizations

The organizations that will succeed in the years ahead will not be those that extract the most from their people. They will be those that can sustain human energy, resilience, trust, and performance over the long term.

Exhausted people do not innovate. Burned-out managers do not create thriving cultures. And economies cannot prosper when the workforce that supports them is steadily depleted.

Human sustainability is no longer just a wellbeing conversation. It is a leadership, economic, and societal priority.

Taking prescription medication is a common part of modern life. In fact, more than 131 million American adults take at least one prescription regularly. As we age, managing these medications becomes a vital part of staying healthy.

While healthy habits and doctor visits are key, taking your medication correctly is just as important. Your pharmacist is your best resource for understanding new prescriptions, but the label on your bottle is your daily roadmap.

7 Things to Know About Your Prescription Label

Pharmacy Details: Located at the top of your label, including pharmacy name, address, and phone number. Keep this for quick reference or refills.

Prescription Number (Rx#): A unique identifier used for refills and pharmacy records.

Medication Name & Instructions: Shows drug name and dosage. Pay attention to “Sig,” which explains exactly how and when to take it.

Refill Status: Indicates remaining refills and prescription expiration date, not the medication’s expiration.

Discard Date: Also labeled “Do not use after.” After this date, the medication may lose effectiveness or safety.

Warning Labels & Stickers: Includes safety instructions such as take with food, avoid alcohol, or do not crush.

Physical Description: Details pill appearance, such as color, shape, and imprint, to help verify the correct medication.

Pro Tip: Before leaving the pharmacy, always confirm what the medication is for, how to take it, and possible side effects. Your pharmacist is there to help with questions about safety, cost, and interactions.

A successful open enrollment starts long before the first form is signed. By reviewing and tailoring your benefits now, you can create a rewarding experience that truly enhances your employees’ overall health and financial security. Here are several key steps to help you prepare for your best enrollment period yet.

Plan and Prepare Early (8–12 Weeks Before)

Use the Right Tools: Implement a 24/7 benefits portal so employees can review options at their convenience.

Learn from the Past: Analyze last year’s questions, pain points, and participation trends.

Build Clear Resources: Create a concise, easy-to-navigate benefits guide with side-by-side plan comparisons.

Develop Education Materials: Prepare FAQs, short videos, and simple explainers to break down complex topics.

Confirm Vendors & Rates: Finalize plan details early to avoid last-minute confusion.

Communication Kick-Off (4 Weeks Before)

Launch a Multi-Channel Campaign: Use email, chat tools, intranet, and meetings to reach employees where they are.

Train Managers: Provide leaders with talking points and FAQs so they can confidently guide their teams.

Promote Key Dates: Add enrollment deadlines to calendars, email signatures, and company announcements.

Segment Messaging: Tailor communications for different employee groups, such as new hires, families, and remote staff.

The Final Countdown (1–2 Weeks Before)

Host Live Sessions: Offer webinars, Q&A forums, and optional 1:1 meetings for personalized guidance.

Share Printed/Downloadable Materials: Ensure everyone has access to key information, even offline.

Highlight “What’s Changing”: Clearly call out plan updates, cost changes, or new benefits.

Prep Your Support Team: Make sure HR or benefits admins are ready to respond quickly to questions.

During Open Enrollment

Centralize Information: Provide easy access to plan summaries, rates, and enrollment instructions.

Offer Ongoing Support: Extend office hours, live chat, or help desks for real-time assistance.

Send Timely Reminders: Use countdown emails or alerts as deadlines approach.

Encourage Action Early: Prompt employees to enroll sooner rather than waiting until the last day.

Post Open Enrollment (1–2 Weeks After)

Review and Submit: Audit elections for completeness and accuracy before final submission.

Confirm Compliance: Ensure all regulatory and reporting requirements are met.

Communicate Next Steps: Let employees know when benefits take effect and what to expect next.

Gather Feedback: Survey employees to identify opportunities to improve next year’s process.

Track Metrics: Evaluate participation rates, common questions, and engagement to refine future strategies.

A strong open enrollment season doesn’t just check a box. It reinforces trust, improves retention, and ensures employees feel informed and supported in their benefits decisions.

Health insurance can be complex, especially when your employer introduces new benefit structures. One option you may encounter is the Individual Coverage Health Reimbursement Arrangement (ICHRA). Unlike traditional group plans where the employer selects a single policy for everyone, an ICHRA changes how benefits are delivered.

Under an ICHRA, your employer decides on a monthly allowance to provide tax-free funds to reimburse you for individual health insurance premiums and eligible medical expenses. Because of federal regulations, an ICHRA serves as your designated benefit plan—it replaces, rather than supplements, traditional group coverage.

Debunking Common ICHRA Myths

If you’ve heard conflicting information about ICHRAs, here is the reality behind three common misconceptions:

Myth: ICHRAs are only for small businesses.

Fact: Organizations of all sizes are increasingly adopting ICHRAs. Because they offer predictable budgeting and administrative flexibility, many large employers now use them to accommodate employees across different states or job categories.

Myth: Selecting your own insurance is too complicated.

Fact: Many employees actually prefer the control an ICHRA provides. Modern, user-friendly digital tools allow you to compare plans tailored to your specific needs, often making the selection process straightforward and efficient.

Myth: ICHRAs create more hassle and offer less support.

Fact: ICHRAs are designed for simplicity. Employers typically utilize dedicated platforms and mobile apps that streamline enrollment, simplify the reimbursement process, and provide access to administrators who can answer your coverage questions.

Why Consider an ICHRA?

The primary advantage of an ICHRA is flexibility. Instead of being locked into a one-size-fits-all group plan, you have the autonomy to select an individual health insurance policy that truly aligns with your personal health needs and preferences.

If your employer offers an ICHRA, reach out to your HR department to learn more about the specific platforms and support resources available to you.

Exhausted employees do not innovate, and burned-out managers cannot build strong, thriving cultures. For nearly a decade, corporate wellness has been siloed into superficial initiatives: wellness apps, awareness weeks, or reactive crisis counseling.

Exhausted employees do not innovate, and burned-out managers cannot build strong, thriving cultures. For nearly a decade, corporate wellness has been siloed into superficial initiatives: wellness apps, awareness weeks, or reactive crisis counseling.

Taking prescription medication is a common part of modern life. In fact, more than

Taking prescription medication is a common part of modern life. In fact, more than  A successful open enrollment starts long before the first form is signed. By reviewing and tailoring your benefits now, you can create a rewarding experience that truly enhances your employees’ overall health and financial security. Here are several key steps to help you prepare for your best enrollment period yet.

A successful open enrollment starts long before the first form is signed. By reviewing and tailoring your benefits now, you can create a rewarding experience that truly enhances your employees’ overall health and financial security. Here are several key steps to help you prepare for your best enrollment period yet.