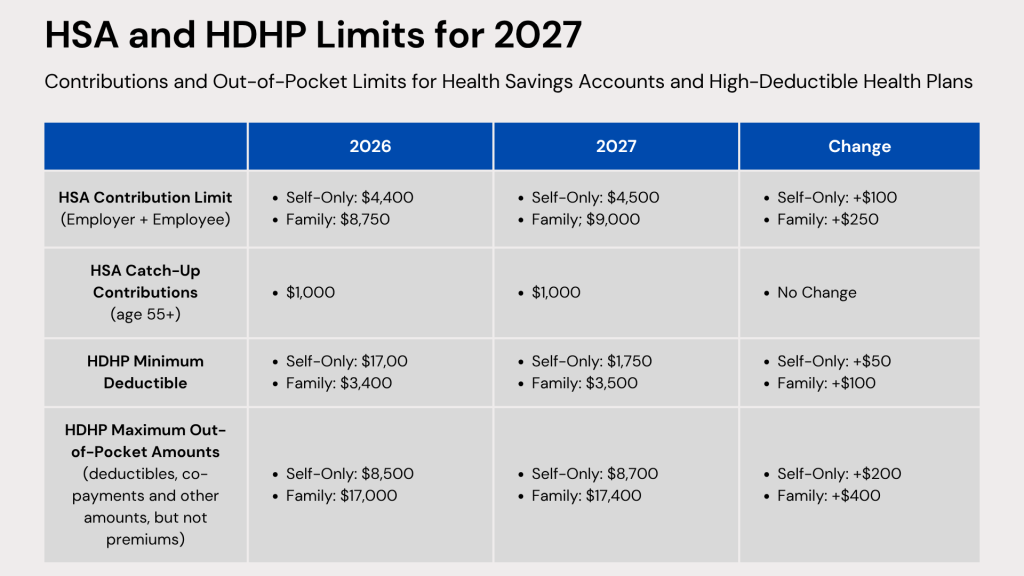

On May 29, 2026, the IRS issued Revenue Procedure 2026-24, which sets the inflation-adjusted limits for health savings accounts (HSAs) and high deductible health plans (HDHPs) for 2027.

The updated limits address:

The maximum allowable HSA contribution

The minimum deductible required for HDHPs

The maximum out-of-pocket expenses permitted for HDHPs

Each of these limits differs depending on whether the coverage is for an individual or a family under an HDHP.

On May 4, 2026, the IRS announced updated penalty amounts for 2027 under the Affordable Care Act’s (ACA) employer shared responsibility, or “pay-or-play,” rules. For the 2027 calendar year, the $2,000 penalty has been adjusted to $3,780, and the $3,000 penalty has increased to $5,670. This marks a rise from 2026 levels of $3,340 and $5,010, respectively.

Understanding Pay-or-Play Requirements

The ACA requires applicable large employers (ALEs)—those with 50 or more full-time and full-time equivalent employees—to offer affordable, minimum value (MV) health coverage to full-time employees and their dependents. Employers that fail to meet these requirements may face IRS penalties if at least one employee receives a premium tax credit through a Health Insurance Marketplace.

Penalties may apply if an ALE:

Fails to offer coverage to at least 95% of full-time employees and their dependents;

Offers coverage to most employees but not to a specific individual who receives a subsidy; or

Offers coverage that is unaffordable or does not meet minimum value standards.

How the Penalties Work

There are two potential penalties under the pay-or-play rules:

Section 4980H(a): Applies when an ALE does not offer coverage to substantially all full-time employees. If at least one employee receives subsidized coverage through the Marketplace, the employer pays a monthly penalty based on total full-time employees, minus 30. For 2027, this penalty is calculated using the adjusted annual amount of $3,780.

Section 4980H(b): Applies when an ALE offers coverage to most employees but fails to meet affordability or minimum value requirements, or excludes certain employees. The penalty is assessed monthly for each full-time employee who receives a subsidy. For 2027, this amount is $5,670 annually. However, the total penalty cannot exceed the 4980H(a) maximum.

With rising penalty amounts, it’s more important than ever for employers to review their health coverage offerings to ensure compliance and avoid unnecessary costs.

On January 29, 2026, the U.S. Department of Health and Human Services (HHS) officially released the maximum cost-sharing limits for the 2027 plan year. These figures represent a significant 13.2% increase over the 2026 limits, marking a substantial shift in potential out-of-pocket expenses for plan participants.

2027 Maximum Out-of-Pocket Limits

For 2027, the maximum annual limitation on cost-sharing is:

Self-Only Coverage: $12,000 (Up from $10,600 in 2026)

Family Coverage: $24,000 (Up from $21,200 in 2026)

Employers must review their current plan designs to ensure they remain compliant with these updated Affordable Care Act (ACA) mandates.

Understanding the Out-of-Pocket Maximum (OOPM)

The ACA requires most health plans to set an annual cap on total enrollee cost-sharing for Essential Health Benefits (EHBs). This limit is commonly known as the Out-of-Pocket Maximum (OOPM).

Scope of Coverage:

Applicability: These limits apply to all non-grandfathered health plans, including self-insured, level-funded, and fully insured plans of all sizes.

Included Costs: Deductibles, copayments, and coinsurance all count toward the limit. Premiums and spending for non-covered services are excluded.

Essential Health Benefits: Limits apply to the 10 EHB categories, such as emergency services, hospitalization, prescription drugs, and maternity care. Plans are not required to apply the OOPM to non-EHB services.

Network Status: Plans generally do not have to count out-of-network expenses toward the ACA’s cost-sharing limit.

The “Embedded” Individual Limit

Even within a family plan, the ACA’s self-only cost-sharing limit applies to each individual. This means that if a family plan has a total OOPM higher than the self-only limit ($12,000 for 2027), the plan must include an “embedded” individual OOPM.

Once any single individual in a family reaches the $12,000 threshold, the plan must cover 100% of their qualified expenses for the rest of the year, even if the total family limit has not yet been met.

HSA-Compatible High Deductible Health Plans (HDHPs)

It is important to note that HDHPs compatible with Health Savings Accounts (HSAs) are subject to lower out-of-pocket limits set by the IRS.

While the 2027 HDHP limits have not yet been released, for comparison, the 2026 HDHP limits are capped at $8,500 for self-only and $17,000 for family coverage. Employers with HSA-qualified plans should watch for separate IRS guidance later this year.

Next Steps for Employers:

Audit 2027 plan designs for compliance with the $12,000/$24,000 thresholds.

Ensure payroll and benefits systems are updated to handle the embedded individual maximums.

Consult with your benefits advisor to prepare for the upcoming open enrollment cycle.

The Internal Revenue Service (IRS) has issued Notice 2025-61, announcing a significant increase to the Patient-Centered Outcomes Research Institute (PCORI) fee amount. Employers with self-insured health plans and health insurance issuers must take note of the new rate and upcoming compliance deadlines.

What is the New PCORI Fee Amount?

The PCORI fee is increasing to $3.84 per covered life. This new rate applies to plan years that end on or after October 1, 2025, and before October 1, 2026.

For comparison, the previous fee amount (for plan years that ended on or after Oct. 1, 2024, and before Oct. 1, 2025) was $3.47 multiplied by the average number of lives covered under the plan.

Background and Applicability

The PCORI fee was originally established by the Affordable Care Act (ACA) to fund comparative effectiveness research. Though initially set to expire in 2019, federal legislation extended the fee for an additional 10 years. The PCORI fee is now scheduled to apply through the plan or policy year ending before October 1, 2029.

The fee is imposed on:

Health insurance issuers

Sponsors of self-insured health plans

The fee is calculated based on the average number of covered lives under the plan, which generally includes employees, their enrolled spouses, and dependents (unless the plan is an HRA or FSA).

Reporting and Payment Deadlines

The PCORI fee must be reported and paid annually using IRS Form 720 (Quarterly Federal Excise Tax Return).

The fee is always due by July 31st of the year following the last day of the plan year.

Action for Self-Insured Plans: Employers with self-insured health plans should ensure they use the correct rate and meet the upcoming July 31st deadline corresponding to their plan year end.

The U.S. Department of Health and Human Services (HHS) has issued a final rule that requires covered entities—including many health plans—to update their Notice of Privacy Practices (Privacy Notice). This change enhances privacy protections for highly sensitive Substance Use Disorder (SUD) treatment records.

Why the Update is Necessary

The HIPAA Privacy Rule already mandates that covered entities provide a Privacy Notice to explain how an individual’s Protected Health Information (PHI) is used.

However, the April 2024 final rule specifically addresses patient records involving SUD treatment from federally assisted programs (often referred to as “Part 2 programs”). Any covered entity that receives or maintains these Part 2 records must now update their Privacy Notice to reflect these additional, heightened protections.

The mandatory deadline for updating and distributing these notices is February 16, 2026.

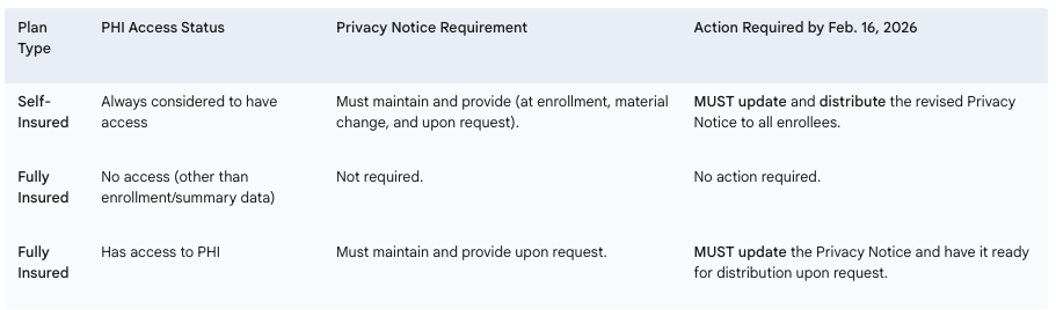

Required Employer Actions by Plan Type

Employers sponsoring health plans must determine their level of responsibility based on their plan’s funding structure and access to PHI.

Next Steps for Employers: Employers with self-insured health plans, or fully insured plans that manage PHI, must immediately begin the process of updating their Privacy Notices to incorporate the new requirements for SUD treatment records. It is currently uncertain if HHS will release updated model privacy notices before the deadline.

Employers with insured health plans may have received a Medical Loss Ratio (MLR) rebate from their health insurance carrier this year. Rebates were required for plans not meeting the 2024 MLR standards and had to be issued by September 30, 2025, either as premium credits or lump-sum payments.

If any part of the rebate qualifies as a plan asset under ERISA, it must benefit plan participants and beneficiaries exclusively. Employers can fulfill this requirement by distributing the plan asset portion using a fair and reasonable allocation method. Alternatively, if direct payments aren’t practical, the rebate can be used for other allowable plan purposes, such as future premium reductions or benefit enhancements.

ERISA generally requires that plan assets be kept in trust, but this is waived if any rebate amount considered a plan asset is used within three months of receipt, so employers must pay careful attention to the timeline. For example, rebates received on September 30, 2025, must be used by December 30, 2025.

Key points:

Under the Affordable Care Act, health insurers must spend a minimum percentage of premiums on medical care and quality improvements; if not, rebates are required.

Employers must determine if any rebate portion qualifies as a plan asset under ERISA.

Plan assets must only benefit plan participants and beneficiaries and generally must be used within three months of receiving the rebate to remain ERISA-compliant.

Employers should review current obligations to ensure any rebate qualifying as a plan asset is properly allocated and used in accordance with federal requirements.