by admin | Mar 24, 2017 | ACA, Group Benefit Plans, IRS

A fixed indemnity health plan pays a specific amount of cash for certain health-related events (for example, $40 per office visit or $100 per hospital day). The amount paid is neither related to the medical expense incurred, nor coordinated with other health coverage. Further, a fixed indemnity health plan is considered an “excepted benefit.”

Under HIPAA, fixed dollar indemnity policies are excepted benefits if they are offered as “independent, non-coordinated benefits.” Under the Patient Protection and Affordable Care Act (ACA), excepted benefits are not subject to the ACA’s health insurance requirements or prohibitions (for example, annual and lifetime dollar limits, out-of-pocket limits, requiring individual and small-group policies to cover ten essential health benefits, etc.). This means that excepted benefit policies can exclude preexisting conditions, can have dollar limits, and do not legally have to guarantee renewal when the coverage is cancelled.

Further, under the ACA, excepted benefits are not minimum essential coverage so a large employer cannot comply with its employer shared responsibility obligations by offering only fixed indemnity coverage to its full-time employees.

Some examples of fixed indemnity health plans are AFLAC or similar coverage, or cancer insurance policies.

Recently, the IRS released a Memorandum on the tax treatment of benefits paid by fixed indemnity health plans that addresses two questions:

- Are payments to an employee under an employer-provided fixed indemnity health plan excludible from the employee’s income under Internal Revenue Code §105?

- Are payments to an employee under an employer-provided fixed indemnity health plan excludible from the employee’s income under Internal Revenue Code §105 if the payments are made by salary reduction through a §125 cafeteria plan?

By Danielle Capilla, Originally Published By United Benefit Advisors

by admin | Mar 15, 2017 | ACA, Benefit Plan Tips, Tricks and Traps, COBRA, Compliance, Medicare

Our Firm is making a big push to provide compliance assessments for our clients and using them as a marketing tool with prospects. Since the U.S. Department of Labor (DOL) began its Health Benefits Security Project in October 2012, there has been increased scrutiny. While none of our clients have been audited yet, we expect it is only a matter of time and we want to make sure they are prepared.

We knew most fully insured groups did not have a Summary Plan Description (SPD) for their health and welfare plans, but we have been surprised by some of the other things that were missing. Here are the top five compliance surprises we found.

- COBRA Initial Notice. The initial notice is a core piece of compliance with the Consolidated Omnibus Budget and Reconciliation Act (COBRA) and we have been very surprised by how many clients are not distributing this notice. Our clients using a third-party administrator (TPA), or self-administering COBRA, are doing a good job of sending out the required letters after qualifying events. However, we have found that many clients are not distributing the required COBRA initial notice to new enrollees. The DOL has recently updated the COBRA model notices with expiration dates of December 31, 2019. We are trying to get our clients to update their notices and, if they haven’t consistently distributed the initial notice to all participants, to send it out to everyone now and document how it was sent and to whom.

- Prescription Drug Plan Reporting to CMS. To comply with the Medicare Prescription Drug Improvement and Modernization Act, passed in 2003, employer groups offering prescription benefits to Medicare-eligible individuals need to take two actions each year. The first is an annual report on the Centers for Medicare & Medicaid Services (CMS) website regarding whether the prescription drug plan offered by the group is creditable or non-creditable. The second is distributing a notice annually to Medicare-eligible plan members prior to the October 15 beginning of Medicare open enrollment, disclosing whether the prescription coverage is creditable or non-creditable. We have found that the vast majority (but not 100 percent) of our clients are complying with the second requirement by annually distributing notices to employees. Many clients are not complying with the first requirement and do not go to the CMS website annually to update their information. The annual notice on the CMS website must be made within:

- 60 days after the beginning of the plan year,

- 30 days after the termination of the prescription drug plan, or

- 30 days after any change in the creditability status of the prescription drug plan.

- ACA Notice of Exchange Rights. The Patient Protection and Affordable Care Act (ACA) required that, starting in September 2013, all employers subject to the Fair Labor Standards Act (FLSA) distribute written notices to all employees regarding the state exchanges, eligibility for coverage through the employer, and whether the coverage was qualifying coverage. This notice was to be given to all employees at that time and to all new hires within 14 days of their date of hire. We have found many groups have not included this notice in the information they routinely give to new hires. The DOL has acknowledged that there are no penalties for not distributing the notice, but since it is so easy to comply, why take the chance in case of an audit?

- USERRA Notices. The Uniformed Services Employment and Reemployment Rights Act (USERRA) protects the job rights of individuals who voluntarily or involuntarily leave employment for military service or service in the National Disaster Medical System. USERRA also prohibits employers from discriminating against past and present members of the uniformed services. Employers are required to provide a notice of the rights, benefits and obligations under USERRA. Many employers meet the obligation by posting the DOL’s “Your Rights Under USERRA” poster, or including text in their employee handbook. However, even though USERRA has been around since 1994, we are finding many employers are not providing this information.

- Section 79. Internal Revenue Code Section 79 provides regulations for the taxation of employer-provided life insurance. This code has been around since 1964, and while there have been some changes, the basics have been in place for many years. Despite the length of time it has been in place, we have found a number of groups that are not calculating the imputed income. In essence, if an employer provides more than $50,000 in life insurance, then the employee should be paying tax on the excess coverage based on the IRS’s age rated table 2-2. With many employers outsourcing their payroll or using software programs for payroll, calculating the imputed income usually only takes a couple of mouse clicks. However, we have been surprised by how many employers are not complying with this part of the Internal Revenue Code, and are therefore putting their employees’ beneficiaries at risk.

There have been other surprises through this process, but these are a few of the more striking examples. The feedback we received from our compliance assessments has been overwhelmingly positive. Groups don’t always like to change their processes, but they do appreciate knowing what needs to be done.

By Bob Bentley, Originally Published By United Benefit Advisors

by admin | Mar 2, 2017 | ACA, Group Benefit Plans, Human Resources

Last fall, President Barack Obama signed the Protecting Affordable Coverage for Employees Act (PACE), which preserved the historical definition of small employer to mean an employer that employs 1 to 50 employees. Prior to this newly signed legislation, the Patient Protection and Affordable Care Act (ACA) was set to expand the definition of a small employer to include companies with 51 to 100 employees (mid-size segment) beginning January 1, 2016.

If not for PACE, the mid-size segment would have become subject to the ACA provisions that impact small employers. Included in these provisions is a mandate that requires coverage for essential health benefits (not to be confused with minimum essential coverage, which the ACA requires of applicable large employers) and a requirement that small group plans provide coverage levels that equate to specific actuarial values. The original intent of expanding the definition of small group plans was to lower premium costs and to increase mandated benefits to a larger portion of the population.

The lower cost theory was based on the premise that broadening the risk pool of covered individuals within the small group market would spread the costs over a larger population, thereby reducing premiums to all. However, after further scrutiny and comments, there was concern that the expanded definition would actually increase premium costs to the mid-size segment because they would now be subject to community rating insurance standards. This shift to small group plans might also encourage mid-size groups to leave the fully insured market by self-insuring – a move that could actually negate the intended benefits of the expanded definition.

Another issue with the ACA’s expanded definition of small group plans was that it would have resulted in a double standard for the mid-size segment. Not only would they be subject to the small group coverage requirements, but they would also be subject to the large employer mandate because they would meet the ACA’s definition of an applicable large employer.

Note: Although this bill preserves the traditional definition of a small employer, it does allow states to expand the definition to include organizations with 51 to 100 employees, if so desired.

By Vicki Randall, Originally Published By United Benefit Advisors

by admin | Feb 20, 2017 | Group Benefit Plans, Health Plan Benchmarking

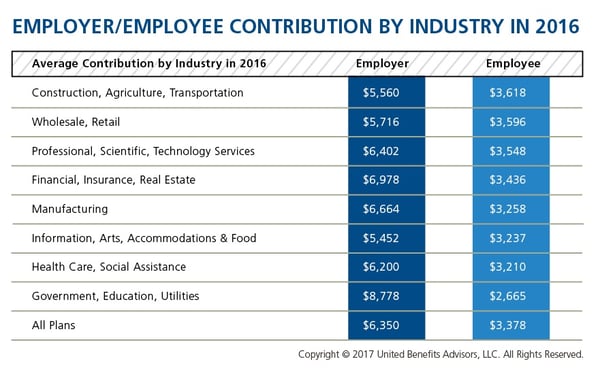

We recently shared healthcare cost benchmarking best practices and reported on the best and worst industries/states for group healthcare. But how much are you contributing toward healthcare costs vs. your employees? That’s a key benchmark, especially when “cost-shifting” is the main strategy for mitigating risk for employers. You may have the most affordable plan, but if you are passing most of that cost on to your employees, you may not be a competitive employer.

According to the latest UBA Health Plan Survey, total costs per employee for the retail, construction, and hospitality sectors are 4.3 percent to 11.3 percent lower than average, making employees in these industries among the least expensive to cover. But employees in the retail and construction sectors pay 6.3 percent and 6.8 percent above the average employee contribution, respectively (hospitality employees pay slightly below the average employee contribution).

On the other end of the cost spectrum, the government sector has the priciest plans ($11,443 per employee) and passes on the least cost to employees, whose average contributions are more than 23 percent less than average. (Surprisingly, these employees are experiencing sticker shock this year since they’ve seen a 26.6 percent increase in their contributions, which were 45.2 percent below average last year.)

When employees’ out of pocket costs are rising, carefully considering and benchmarking their contributions toward the total cost is important—and not nationally, but compared to your peers. Here’s a look at all the average employer/employee contributions by industry:

By RJ Nelson, Originally Published By United Benefit Advisors

by admin | Feb 2, 2017 | Compliance, Hot Topics, Human Resources

Recently, the Equal Employment Opportunity Commission (EEOC) issued new guidance on national origin discrimination. National origin discrimination is discrimination because an individual is, or the individual’s ancestors are, from a certain place or has the physical, cultural, or linguistic characteristics of a particular national origin group, including Native American tribes. A member of one national origin group can discriminate against a member of the same group. While many of the previous rules and regulations remain intact, new protections have been added.

One of the key changes is the addition of perceived national origin to the definition. Title VII of the Civil Rights Act of 1964 prohibits employment discrimination based on the belief that an individual is (or the individual’s ancestors are) from one or more particular countries, or belongs to one or more particular national origin groups. The EEOC’s example describes discrimination against someone who is perceived to be from the Middle East, regardless of whether he or she is from the Middle East or ethnically Arab. It is also unlawful to discriminate based on association; for example, you cannot discriminate against an employee because the employee is married to, friends with, or has a child with someone of a different national origin or ethnicity.

Language issues are also emphasized in the new guidance. Specifically, business necessity and material impact on job performance are the only legitimate reasons for basing employment decisions on linguistic characteristics, such as accents. Applying uniform fluency requirements to a broad range of jobs or requiring a greater level of fluency than necessary may result in a violation of Title VII. The EEOC’s long-standing English-only guidelines, issued in 1980, provide that rules requiring employees to speak English in the workplace at all times are presumed to violate Title VII.

Title VII applies to all employment decisions, including those involving:

- Recruitment

- Hiring

- Promotion

- Work assignments

- Segregation and classification

- Transfer

- Wages and benefits

- Leave

- Training and apprenticeship programs

- Discipline

- Layoff and termination

- Other terms and conditions of employment

The new EEOC guidance reinforces and clarifies standing obligations of employers who may be in violation of Title VII if they implement discriminatory practices based on customer, client, or employee preferences. This includes but is not limited to:

- Segregation of employees by protected class, such as one ethnic group working in back rooms while others are customer-facing.

- Failure by employers to take steps to protect employees who are harassed by customers based on the employees’ national origin.

- Failure to take advantage of preventive or corrective opportunities when a supervisor or employees engage in discrimination.

- An employer may also be jointly liable with staffing firms that provide workers if the employer knowingly ignores discriminatory practices. Human trafficking that includes employer misconduct has been added to the definition of unlawful harassment.

The guidance includes “promising practices” for employers that are meant to reduce the risk of Title VII violations. This includes:

- Avoiding word-of-mouth recruitment to attract a diverse applicant pool.

- Establishing written criteria for hiring and promotion and applying the standards consistently.

- Offering training in the languages spoken by employees.

- Developing objective, job-related criteria for identifying the unsatisfactory performance or conduct that can result in discipline, demotion, or discharge.

- Clearly communicating to employees through policies and actions that harassment will not be tolerated and that employees who violate the prohibition against harassment will be disciplined.

Employers should keep in mind that national origin discrimination is often intersectional; individuals can be members of two or more protected classes, such as race, national origin, and sex. Intersectionality can add complexity to discrimination claims.

On the heels of an acrimonious election that has frequently placed national origin in the spotlight, employers should revisit workplace practices, including talent acquisition policies, training and development protocols, anti-harassment training, and complaint resolution practices.

By Nancy Bourque, Originally Published By United Benefit Advisors