by admin | May 30, 2023 | Employee Benefits, HSA/HRA

Are you the type of person who loves to save money? You’ll be happy to know that there’s a way to do so with your health care costs. It starts with medical expense accounts which let you set aside money to pay for certain health products and services. One type of medical expense account is a Health Savings Account (HSA).

How Does An HSA Work?

An HSA is a type of personal savings account you can use to pay certain health care costs. An HSA lets you pay for qualified health, dental and vision care costs for yourself, spouse and dependents with tax-free money. The money you contribute comes out of your paycheck – before taxes – and that is how you save to pay for your out-of-pocket health care expenses. Like a regular savings account, your HSA has an interest rate that allows your money to grow while sitting in the account. Your employer also has the option of contributing to your HSA, helping it to grow faster.

If you don’t use all of your HSA funds during the calendar year, you can roll that money over. An HSA is owned by you so you take it with you no matter if you change plans, change jobs or if you decide to retire. You will get a debit card which is linked to your HSA when you set up your account that you use to pay for eligible expenses.

You must be enrolled in a High Deductible Health Plan (HDHP) to open and contribute to an HSA. HDHPs medical plans aim to minimize your health care costs if you don’t use your plan a lot but keep you financially protected in cases of illness or emergency. Similar to a car insurance policy, you pay for your expenses up to the point that you meet your deductible and then the insurance coverage begins. The higher the deductible you choose, the smaller the monthly cost will be. But it also means that when you have health expenses, you are responsible for all of the costs up to your deductible amount. Rather than pay for your health expenses that occur before hitting your deductible out of your pocket, you can pay for those expenses using pre-tax dollars from your HSA account.

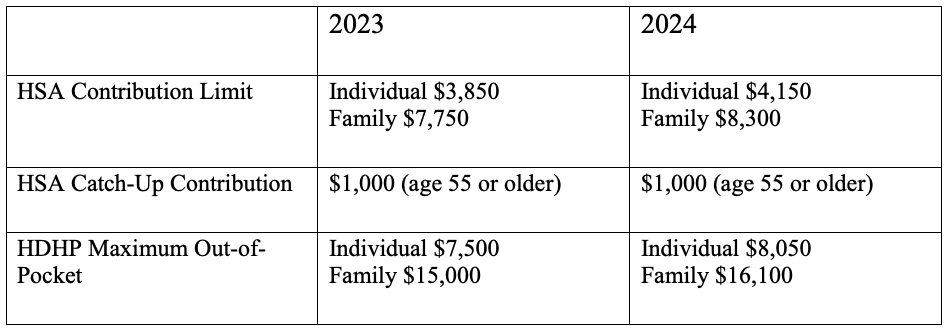

Federal law includes strict guidelines for HSAs including HDHP cost sharing and annual limits on contributions. The amount you contribute can be adjusted throughout the year but they do have an annual limit on how much you can contribute per year. This limit is set by the IRS and usually increases each year. Contribution limits for 2023 and 2024 are:

What Are the Benefits of Having an HSA?

- Money goes in tax-free – Your HSA contributions are made on a pre-tax basis and are also tax deductible

- Money comes out tax-free – Eligible healthcare purchases can be made directly from the HSA account

- Earn interest, tax-free – The interest on HSA funds grows on a tax-free basis. Unlike most savings accounts, interest earned on an HSA is not considered taxable income when funds are used for eligible medical expenses.

- Your HSA balance can be invested – Depending on your HSA, you may be eligible to invest your HSA similar to a 401k or IRA – in an interest-bearing account, mutual fund, stocks or bonds.

- Your HSA balance can be carried over – Unlike a Flexible Spending Account (FSA), an HSA is not a use-it-or-lose-it account. You can carry over your balance year after year.

- You can use your HSA to add to your retirement funds – After the age of 65, you can withdraw funds from your HSA for any reason without penalty.

The Bottom Line

HSAs are often referred to as triple tax-advantaged and are one of the best savings and investment tools available under the U.S. tax code. As a person ages, medical expenses tend to increase, particularly when reaching retirement age and beyond. Therefore, starting an HSA early and allowing it to accumulate over a long period, can contribute greatly to securing your financial future.

by admin | Oct 1, 2020 | Benefit Management, HSA/HRA

Health Savings Accounts (HSA) are great ways to save tax-free money for medical expenses both in the current term, and for your retirement years. By making wise choices, you can maximize the benefit of these fantastic savings accounts. Let’s take a quick look at the basics and then explore some tips on how to make your HSA money grow.

What is an HSA?

According to the website HealthCare.gov, a Health Savings Account is a type of savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. By using untaxed dollars in an HSA to pay for deductibles, copayments, coinsurance, and some other expenses, you may be able to lower your overall health care costs. HSA funds generally may not be used to pay premiums.

In order to contribute to an HSA, you must be enrolled in a High Deductible Health Plan (HDHP). A HDHP is defined as a plan with a higher deductible than a traditional insurance plan. The monthly premium is usually lower, but you pay more health care costs yourself before the insurance company starts to pay its share (your deductible). A high deductible plan (HDHP) can be combined with a health savings account (HSA), allowing you to pay for certain medical expenses with money free from federal taxes.

HSA vs Traditional Insurance

As mentioned, you are able to open a Health Savings Account when you enroll in your employer’s High Deductible Health Plan. A HDHP is different from traditional insurance in that with traditional insurance, you and your employer both contribute to the cost of your health insurance each month—otherwise known as the premium. You then have a fixed cost—a “co-pay”—that you pay when you visit a doctor, pay for prescriptions, or have a health procedure. With a HDHP, the patient is incentivized to shop around for lower cost doctor visits and procedures since they are paying for those costs out of their pocket at the full amount from the beginning until the high deductible amount is met.

Now, when used in tandem, the two components of the HDHP and the HSA have the potential to save the insured party money on their health care expenses. Here’s how it works:

- Contribution Limits

Each year, the government puts a cap on the amount of money that an individual and a family can contribute to their HSA. For 2020, an individual can contribute up to $3550 and a family can add in $7100 to their account. In 2021, the amounts both increase: individuals will be $3600 and families will be able to deposit $7200.

- Triple Tax Benefits

When you contribute to your HSA, your money gets a triple tax benefit. There is a 0% tax on deposited money, your money grows tax-free while in the account, and, when used for qualified medical expenses, you can withdraw the money tax-free.

- Roll-over

The money that you deposit into your HSA is yours to keep–forever. If you change jobs, the money follows you. If you don’t use the money you’ve contributed by the end of the year, it rolls over to the next year with no penalty.

Tips to Maximize the Benefits of Your HSA This Year

Don’t be complacent to let your tax-free hard-earned money simply sit in your HSA all year! You can by making some wise choices. Here’s some tips on how to do this:

- Do you get a bonus at the end of the year? You can use that bonus money to bulk up your HSA until April 15 of the following calendar year. Just make sure you don’t contribute more than the annual allowed amount or you will pay a 6% tax on the overage.

- Once you hit the minimum contribution amount for your particular plan, you can invest a portion of the contributions in an IRA account and watch your tax-free dollars grow even more! Check with your plan manager regarding the minimum amount required.

- There is a once-in-a-lifetime allowance for you to move money over from a traditional or Roth IRA to your HSA. This allows you to kickstart that HSA so that you can begin using that money for expenses right away. The annual contribution limit still applies to this scenario for the individual and family amount.

- Long term care insurance is expensive and you can use your HSA money to help pay for those insurance premiums. Again, check with your plan manager to make sure you are staying within the allowed range for using this money for those premiums.

- Finally, name your spouse as the beneficiary of your account. When you pass away, your spouse will have access to these funds with the same tax benefits as you did. In fact, your HSA money can even continue to grow tax-free after you pass.

Finding ways to save money is always a good idea. Finding ways to maximize the benefit of your already saved money is even better!

by admin | Jun 4, 2019 | Employee Benefits, IRS

On May 28, 2019, the Internal Revenue Service (IRS) released Revenue Procedure 2019-25 announcing the annual inflation-adjusted limits for health savings accounts (HSAs) for calendar year 2020. An HSA is a tax-exempt savings account that employees can use to pay for qualified health expenses.

To be eligible for an HSA, an employee:

- Must be covered by a qualified high deductible health plan (HDHP);

- Must not have any disqualifying health coverage (called “impermissible non-HDHP coverage”);

- Must not be enrolled in Medicare; and

- May not be claimed as a dependent on someone else’s tax return.

The limits vary based on whether an individual has self-only or family coverage under an HDHP. The limits are as follows:

- 2020 HSA contribution limit:

- Single: $3,550 (an increase of $50 from 2019)

- Family: $7,100 (an increase of $100 from 2019)

- Catch-up contributions for those age 55 and older remains at $1,000

- 2020 HDHP minimum deductible (not applicable to preventive services):

- Single: $1,400 (an increase of $50 from 2019)

- Family: $2,800 (an increase of $100 from 2019)

- 2020 HDHP maximum out-of-pocket limit:

- Single: $6,900 (an increase of $150 from 2019)

- Family: $13,800* (an increase of $300 from 2019)

*If the HDHP is a nongrandfathered plan, a per-person limit of $8,150 also will apply due to the Affordable Care Act’s cost-sharing provision for essential health benefits.

Originally posted on ThinkHR.com

by admin | Nov 7, 2018 | ACA, Compliance, Human Resources, IRS

On November 5, 2018, the Internal Revenue Service (IRS) released Notice 2018-85 to announce that the health plan Patient-Centered Outcomes Research Institute (PCORI) fee for plan years ending between October 1, 2018 and September 30, 2019 will be $2.45 per plan participant. This is an increase from the prior year’s fee of $2.39 due to an inflation adjustment.

Background

The Affordable Care Act created the PCORI to study clinical effectiveness and health outcomes. To finance the nonprofit institute’s work, a small annual fee — commonly called the PCORI fee — is charged on group health plans.

The fee is an annual amount multiplied by the number of plan participants. The dollar amount of the fee is based on the ending date of the plan year. For instance:

- For plan year ending between October 1, 2017 and September 30, 2018: $2.39.

- For plan year ending between October 1, 2018 and September 30, 2019: $2.45.

Insurers are responsible for calculating and paying the fee for insured plans. For self-funded health plans, however, the employer sponsor is responsible for calculating and paying the fee. Payment is due by filing Form 720 by July 31 following the end of the calendar year in which the health plan year ends. For example, if the group health plan year ends December 31, 2018, Form 720 must be filed along with payment no later than July 31, 2019.

Certain types of health plans are exempt from the fee, such as:

- Stand-alone dental and/or vision plans;

- Employee assistance, disease management, and wellness programs that do not provide significant medical care benefits;

- Stop-loss insurance policies; and

- Health savings accounts (HSAs).

HRAs and QSEHRAs

A traditional health reimbursement arrangement (HRA) is exempt from the PCORI fee, provided that it is integrated with another self-funded health plan sponsored by the same employer. In that case, the employer pays the PCORI fee with respect to its self-funded plan, but does not pay again just for the HRA component. If, however, the HRA is integrated with a group insurance health plan, the insurer will pay the PCORI fee with respect to the insured coverage and the employer pays the fee for the HRA component.

A qualified small employer health reimbursement arrangement (QSEHRA) works a little differently. A QSEHRA is a special type of tax-preferred arrangement that can only be offered by small employers (generally those with fewer than 50 employees) that do not offer any other health plan to their workers. Since the QSEHRA is not integrated with another plan, the PCORI fee applies to the QSEHRA. Small employers that sponsor a QSEHRA are responsible for reporting and paying the PCORI fee.

PCORI Nears its End

The PCORI program will sunset in 2019. The last payment will apply to plan years that end by September 30, 2019 and that payment will be due in July 2020. There will not be any PCORI fee for plan years that end on October 1, 2019 or later.

Resources

The IRS provides the following guidance to help plan sponsors calculate, report, and pay the PCORI fee:

Originally posted on thinkhr.com

by admin | Aug 7, 2018 | Group Benefit Plans, Hot Topics

Q.For a high deductible health plan (HDHP) to qualify for health savings account (HSA) eligibility, what is the minimum amount that an embedded individual deductible can be?

A.For 2018, the embedded individual deductible must be at least $2,700. For an HDHP to qualify for HSA eligibility, an individual with family coverage would need to satisfy the required minimum annual deductible for family HDHP coverage (which is at least $2,700 for 2018) before any amounts are paid from the HDHP.