by admin | Aug 5, 2024 | Flexible Spending Accounts, HSA/HRA

Medical expense accounts can help you save on all kinds of healthcare costs. Here are some you may not know about yet.

HSA, FSA, and HRA can typically be used for:

- Medical expenses: Doctor visits, surgeries, prescriptions, dental and vision care, and mental health services.

- Over-the-counter (OTC) medications: Many OTC medications, including pain relievers, allergy medications, and cold remedies, are now eligible.

- Medical equipment: Items like crutches, wheelchairs, and diabetic supplies often qualify.

- Qualified medical transportation: Expenses related to getting to and from medical appointments

- Women’s healthcare products: As of 2020, many women’s healthcare and hygiene items—including pads and tampons—were added to the list. Birth control and other contraceptives also count as qualified medical expenses with a prescription.

- Sunscreen: If you buy sunscreen with a sun protection factor (SPF) of 15 or higher, you can pay for it with your FSA or HSA account.

- Health insurance premiums: In some cases, you can use HSA or FSA funds to pay for COBRA premiums or health insurance premiums during periods of unemployment.

- Alcohol or drug treatment: If you need treatment at a hospital for alcohol or drug abuse, you can cover those costs with your FSA or HSA. That includes meals and a treatment center stay. You can also include rides to and from meetings for groups like Alcoholics Anonymous.

Expenses that might be covered, but check your plan:

- Long-term care: Some plans may cover long-term care expenses, but this is often limited.

- Cosmetic surgery: Generally not covered unless medically necessary.

- Weight loss programs: May be eligible if medically supervised.

- Gym memberships: While some plans cover gym memberships, it’s often dependent on specific medical conditions or doctor referrals.

Important Considerations:

- Keep receipts: You’ll generally need receipts to claim reimbursement for your purchases.

- Check eligibility: Not all items are covered, so verify with your plan administrator.

- Maximize your savings: Use your accounts strategically to reduce out-of-pocket costs.

Additional Tips:

- Shop around: Compare prices for medical goods and services to maximize your savings.

- Take advantage of online resources: Many health insurance providers offer online tools and resources to help you understand your coverage.

- Consult with your healthcare provider: Your doctor can recommend treatments and products that may be eligible for reimbursement.

By understanding the nuances of HSAs, FSAs, and HRAs, you can make informed decisions about how to use these accounts to your advantage and maximize your healthcare savings.

by admin | May 30, 2023 | Employee Benefits, HSA/HRA

Are you the type of person who loves to save money? You’ll be happy to know that there’s a way to do so with your health care costs. It starts with medical expense accounts which let you set aside money to pay for certain health products and services. One type of medical expense account is a Health Savings Account (HSA).

How Does An HSA Work?

An HSA is a type of personal savings account you can use to pay certain health care costs. An HSA lets you pay for qualified health, dental and vision care costs for yourself, spouse and dependents with tax-free money. The money you contribute comes out of your paycheck – before taxes – and that is how you save to pay for your out-of-pocket health care expenses. Like a regular savings account, your HSA has an interest rate that allows your money to grow while sitting in the account. Your employer also has the option of contributing to your HSA, helping it to grow faster.

If you don’t use all of your HSA funds during the calendar year, you can roll that money over. An HSA is owned by you so you take it with you no matter if you change plans, change jobs or if you decide to retire. You will get a debit card which is linked to your HSA when you set up your account that you use to pay for eligible expenses.

You must be enrolled in a High Deductible Health Plan (HDHP) to open and contribute to an HSA. HDHPs medical plans aim to minimize your health care costs if you don’t use your plan a lot but keep you financially protected in cases of illness or emergency. Similar to a car insurance policy, you pay for your expenses up to the point that you meet your deductible and then the insurance coverage begins. The higher the deductible you choose, the smaller the monthly cost will be. But it also means that when you have health expenses, you are responsible for all of the costs up to your deductible amount. Rather than pay for your health expenses that occur before hitting your deductible out of your pocket, you can pay for those expenses using pre-tax dollars from your HSA account.

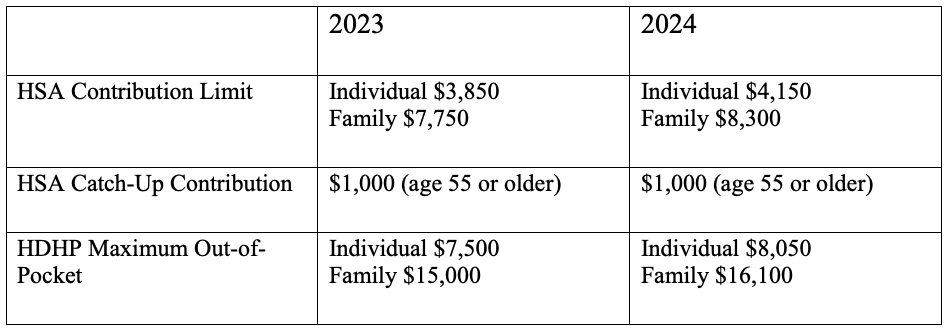

Federal law includes strict guidelines for HSAs including HDHP cost sharing and annual limits on contributions. The amount you contribute can be adjusted throughout the year but they do have an annual limit on how much you can contribute per year. This limit is set by the IRS and usually increases each year. Contribution limits for 2023 and 2024 are:

What Are the Benefits of Having an HSA?

- Money goes in tax-free – Your HSA contributions are made on a pre-tax basis and are also tax deductible

- Money comes out tax-free – Eligible healthcare purchases can be made directly from the HSA account

- Earn interest, tax-free – The interest on HSA funds grows on a tax-free basis. Unlike most savings accounts, interest earned on an HSA is not considered taxable income when funds are used for eligible medical expenses.

- Your HSA balance can be invested – Depending on your HSA, you may be eligible to invest your HSA similar to a 401k or IRA – in an interest-bearing account, mutual fund, stocks or bonds.

- Your HSA balance can be carried over – Unlike a Flexible Spending Account (FSA), an HSA is not a use-it-or-lose-it account. You can carry over your balance year after year.

- You can use your HSA to add to your retirement funds – After the age of 65, you can withdraw funds from your HSA for any reason without penalty.

The Bottom Line

HSAs are often referred to as triple tax-advantaged and are one of the best savings and investment tools available under the U.S. tax code. As a person ages, medical expenses tend to increase, particularly when reaching retirement age and beyond. Therefore, starting an HSA early and allowing it to accumulate over a long period, can contribute greatly to securing your financial future.

by admin | Aug 24, 2021 | Benefit Management, Flexible Spending Accounts, HSA/HRA

We all know how confusing and complex benefits and healthcare terms can be- the difference between deductible and co-insurance is a common question for many and there are plenty of others like it. When you are comfortable and confident in how your plan works, you can make an informed decision on HOW to use and take advantage of your benefits!

We all know how confusing and complex benefits and healthcare terms can be- the difference between deductible and co-insurance is a common question for many and there are plenty of others like it. When you are comfortable and confident in how your plan works, you can make an informed decision on HOW to use and take advantage of your benefits!

We have created a list and explanation of the most common terms to help you understand and better utilize your health benefits:

- Co-payment: An amount you pay as your share of the cost for a medical service or item, like a doctor’s visit. Co-pays are most common for emergency room, urgent care and prescription drugs. In some cases, you may be responsible for paying a co‐pay as well as a percentage of the remaining charges.

- Co-insurance: Your share of the cost for a covered health care service, usually calculated as a percentage (like 20%) of the allowed amount for the service. For example, if your plan has a 30% co-insurance rate, the carrier will pay 70% of the allowed amount while you pay the balance.

- Deductible: The amount you owe for covered health care services before your health insurance or plan begins to pay. For example, many plans require an individual to pay $1,000 in cumulative deductibles before they begin paying out.

- Dependent coverage: Health insurance coverage extended to the spouse and unmarried children up to age 26 who are totally or substantially reliant on their parents for support, thereby defined as “dependent children”.

- Explanation of Benefits (EOB): Every time you use your health insurance, your health plan sends you a record called an “explanation of benefits” (EOB) or “member health statement” that explains how much you owe. The EOB also shows the total cost of care, how much your plan paid and the amount an in-¬network doctor or other healthcare professional is allowed to charge a plan member (called the “allowed amount”).

- In-Network Provider: A provider who has a contract with your health insurer or plan to provide services to you at a discount. In-Network Providers have contracted with the insurance carrier to accept reduced fees for services provided to plan members. Using in-network providers will cost you less money. When contacting an In-Network Provider, remember to ask, “are you a contracted provider with my plan?” Never ask if a provider “takes” your insurance, as they will all take it. The key phrase is contracted.

- Open Enrollment: A period during which a health insurance company is required to accept applicants without regard to health history.

- Out-of-Network Provider: A provider who doesn’t have a contract with your health insurer or plan to provide services to you at a pre-negotiated discount. You’ll pay more to see an out-of-network provider, sometimes referred to as an out-of-network provider.

- Out-of-Pocket Maximum: The limit or most you’ll pay out of your own pocket for services during your insurance plan period (usually one year).

- Premium: The amount you pay for your health insurance or plan each month.

- Qualifying Life Event (QLE): A change in your life that allows you to make changes to your benefits’ coverage outside of the annual open enrollment period. These changes include a change in marital status (marriage, divorce, death of spouse), a change in the number of eligible children (birth, adoption, death, aging-out), and a change in a family member’s benefits eligibility under another plan (losing a job, Medicare or Medicaid eligibility, etc.)

In addition to understanding these common terms, there are other ways to utilize your benefits, save money and make an informed decision based on your specific needs.

- Flexible Spending Account (FSA): Funded through pre-tax payroll deductions, an FSA is a cost-savings tool that allows you to pay for qualified healthcare-related expenses with pre-tax dollars. Funds deposited in an FSA must be spent in the same year in which they are set aside, or they are forfeited. This rule is often referred to as “use it or lose it.”

- Health Reimbursement Account (HRA): An employer-funded savings plan that will reimburse you for out-of-pocket medical expenses. Unlike an FSA, however, you don’t “use it or lose it” – unused balances will roll over and accumulate over time, though the account cannot be “cashed-out.”

- Health Savings Account (HSA): A savings product that serves as a substitute for traditional health insurance. HSAs enable you to pay for current health costs. They also allow you to save for future medical and retiree health costs tax-free. Unlike an FSA, however, you don’t “use it or lose it” – unused balances will roll over and accumulate over time and can be “cashed-out.”

Understanding all of the terms and acronyms can feel like learning a new language, so it’s helpful to have a basic reference chart. With a good understanding of what some healthcare “benefits lingo” means, it will be easier to find a plan that meets your needs and budget. To explore more healthcare terms, visit https://www.shrm.org/resourcesandtools/hr-topics/benefits/pages/common-health-benefit-terms-glossary.aspx

by admin | Jun 1, 2021 | HSA/HRA

On May 10, 2021, the Internal Revenue Service (IRS) released Revenue Procedure 2021-25 announcing the annual inflation-adjusted limits for health savings accounts (HSAs) for calendar year 2022. An HSA is a tax-exempt savings account that employees can use to pay for qualified health expenses.

To be eligible for an HSA, an employee:

- Must be covered by a qualified high deductible health plan (HDHP);

- Must not have any disqualifying health coverage (called “impermissible non-HDHP coverage”);

- Must not be enrolled in Medicare; and

- May not be claimed as a dependent on someone else’s tax return.

The limits vary based on whether an individual has self-only or family coverage under an HDHP. The limits are as follows:

- 2022 HSA contribution limit:

- Single: $3,650 (an increase of $50 from 2021)

- Family: $7,300 (an increase of $100 from 2021)

- Catch-up contributions for those age 55 and older remains at $1,000

- 2022 HDHP minimum deductible*

- Single: $1,400 (no change from 2021)

- Family: $2,800 (no change from 2021)

- 2022 HDHP maximum out-of-pocket limit:

- Single: $7,050 (an increase of $50 from 2021)

- Family: $14,100** (an increase of $100 from 2021)

* The deductible does not apply to preventive care services nor to services related to testing for COVID-19. An HDHP also may choose to waive the deductible for coverage of COVID-19 treatment, and/or telehealth and other remote care services.

** If the HDHP is a non-grandfathered plan, a per-person limit of $8,700 also will apply due to the Affordable Care Act’s cost-sharing provision for essential health benefits.

By Kathy Berger

Originally posted on Mineral.com

by admin | Oct 1, 2020 | Benefit Management, HSA/HRA

Health Savings Accounts (HSA) are great ways to save tax-free money for medical expenses both in the current term, and for your retirement years. By making wise choices, you can maximize the benefit of these fantastic savings accounts. Let’s take a quick look at the basics and then explore some tips on how to make your HSA money grow.

What is an HSA?

According to the website HealthCare.gov, a Health Savings Account is a type of savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. By using untaxed dollars in an HSA to pay for deductibles, copayments, coinsurance, and some other expenses, you may be able to lower your overall health care costs. HSA funds generally may not be used to pay premiums.

In order to contribute to an HSA, you must be enrolled in a High Deductible Health Plan (HDHP). A HDHP is defined as a plan with a higher deductible than a traditional insurance plan. The monthly premium is usually lower, but you pay more health care costs yourself before the insurance company starts to pay its share (your deductible). A high deductible plan (HDHP) can be combined with a health savings account (HSA), allowing you to pay for certain medical expenses with money free from federal taxes.

HSA vs Traditional Insurance

As mentioned, you are able to open a Health Savings Account when you enroll in your employer’s High Deductible Health Plan. A HDHP is different from traditional insurance in that with traditional insurance, you and your employer both contribute to the cost of your health insurance each month—otherwise known as the premium. You then have a fixed cost—a “co-pay”—that you pay when you visit a doctor, pay for prescriptions, or have a health procedure. With a HDHP, the patient is incentivized to shop around for lower cost doctor visits and procedures since they are paying for those costs out of their pocket at the full amount from the beginning until the high deductible amount is met.

Now, when used in tandem, the two components of the HDHP and the HSA have the potential to save the insured party money on their health care expenses. Here’s how it works:

- Contribution Limits

Each year, the government puts a cap on the amount of money that an individual and a family can contribute to their HSA. For 2020, an individual can contribute up to $3550 and a family can add in $7100 to their account. In 2021, the amounts both increase: individuals will be $3600 and families will be able to deposit $7200.

- Triple Tax Benefits

When you contribute to your HSA, your money gets a triple tax benefit. There is a 0% tax on deposited money, your money grows tax-free while in the account, and, when used for qualified medical expenses, you can withdraw the money tax-free.

- Roll-over

The money that you deposit into your HSA is yours to keep–forever. If you change jobs, the money follows you. If you don’t use the money you’ve contributed by the end of the year, it rolls over to the next year with no penalty.

Tips to Maximize the Benefits of Your HSA This Year

Don’t be complacent to let your tax-free hard-earned money simply sit in your HSA all year! You can by making some wise choices. Here’s some tips on how to do this:

- Do you get a bonus at the end of the year? You can use that bonus money to bulk up your HSA until April 15 of the following calendar year. Just make sure you don’t contribute more than the annual allowed amount or you will pay a 6% tax on the overage.

- Once you hit the minimum contribution amount for your particular plan, you can invest a portion of the contributions in an IRA account and watch your tax-free dollars grow even more! Check with your plan manager regarding the minimum amount required.

- There is a once-in-a-lifetime allowance for you to move money over from a traditional or Roth IRA to your HSA. This allows you to kickstart that HSA so that you can begin using that money for expenses right away. The annual contribution limit still applies to this scenario for the individual and family amount.

- Long term care insurance is expensive and you can use your HSA money to help pay for those insurance premiums. Again, check with your plan manager to make sure you are staying within the allowed range for using this money for those premiums.

- Finally, name your spouse as the beneficiary of your account. When you pass away, your spouse will have access to these funds with the same tax benefits as you did. In fact, your HSA money can even continue to grow tax-free after you pass.

Finding ways to save money is always a good idea. Finding ways to maximize the benefit of your already saved money is even better!

by admin | Feb 20, 2019 | Benefit Management, HSA/HRA

The Internal Revenue Service (IRS) released its inflation-adjusted limits for various benefits. For example, the maximum contribution limit to health flexible spending arrangements (FSAs) will be $2,700 in 2019. Also, the maximum reimbursement limit in 2019 for Qualified Small Employer Health Reimbursement Arrangements will be $5,150 for single coverage and $10,450 for family coverage.

Read more about the 2019 limits.

By Karen Hsu

Originally posted on UBABenefits.com