AFFORDABLE CARE ACT INFORMATION REPORTING

AFFORDABLE CARE ACT INFORMATION REPORTING

Beginning in 2024, most employers obligated to report under the Affordable Care Act (ACA) must file returns electronically by March 31, 2024. Employers filing fewer than 10 returns a year are allowed to use paper filing. Since March 31 falls on a weekend, the deadline this year is April 1, 2024.

Applicable large employers (ALEs) and smaller employers with self-insured health plans are required to e-file Forms 1095-C or 1095-B, as well as the accompanying Forms 1094-C or 1094-B, using the IRS’ Affordable Care Act Information Returns (AIR) system. Employers can apply for a 30-day extension for filing these forms by submitting Form 8809 by the original due date.

2023 HEALTH SAVINGS ACCOUNT CONTRIBUTIONS AND CORRECTIONS

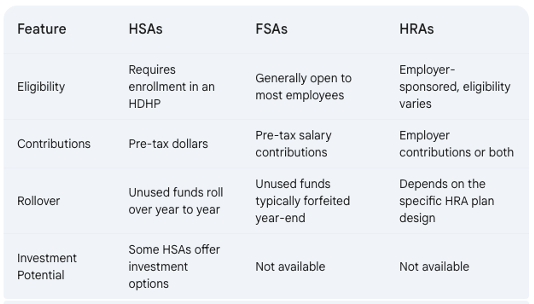

For employers offering a health savings account (HSA), contributions toward the 2023 HSA limits and corrections for the 2023 calendar year must be made by April 15, 2024. Employers and employees can contribute to HSAs and make adjustments until the tax filing deadline, which is typically the individual’s tax filing due date.

Contributions that exceed the annual allowed limit are subject to a 6% tax on the excess contribution. That tax is assessed each year that the excess funds and their earnings remain in the account. Additionally, excess contributions are taxed as income.

Remember that using HSA funds for non-qualified expenses can result in significant penalties. Individuals under age 65 who use HSA money for non-qualified expenses will face a 20% penalty and pay income taxes on the withdrawal. After age 65, HSA funds may be used for non-qualified expenses without incurring the 20% penalty, however the funds will be considered taxable income.

EMPLOYER CONSIDERATIONS

Employers should ensure that employees are aware of the annual contribution limits and the deadline for contribution adjustments, as well as potential tax penalties.

PREPARING FOR JUNE PRESCRIPTION DRUG DATA (RXDC) REPORTING

The third season of Prescription Drug Data Collection (RxDC) reporting is underway, with the annual deadline set for June 1 each year, reporting on the previous calendar year. The Consolidated Appropriations Act requires all group medical plans to file a report with the Centers for Medicare & Medicaid (CMS) detailing the cost and other medical data for the group health plans’ prescription drug and other benefits, excluding excepted benefits. RxDC reporting is mandatory regardless of the group’s insurance status, size, or whether it is a grandfathered plan.

The filing must be completed electronically through the CMS Enterprise Portal. While employers are ultimately responsible for RxDC filing, most third-party administrators (TPAs) pharmacy benefit managers (PBMs) contracted to provide services to the group health plan will assist or submit filings on behalf of the group health plan.

Changes for 2024 RxDC Reporting

The average monthly premium calculation has been simplified. Instead of calculating per member per month, this is stated as the total annual premium divided by 12.

CMS has introduced restrictions on data aggregation. Data in files D1 and D3 through D8 must match the level of detail in the D2 file. This means that if the D2 data is specific to an employer’s plan, the data in files D3 through D8 must be equally specific.

EMPLOYER CONSIDERATIONS

- Insurance carriers will handle RxDC reporting on behalf of employers with fully insured plans. However, employers should confirm with carriers that the reporting has been completed and provide any necessary information.

- Employers with self-insured plans have final responsibility for RxDC filing. If they rely on TPAs or PBMs to assist with filing, it’s crucial to ensure that it is completed on time.

NEW YORK CITY WORKERS ALLOWED TO SUE FOR SICK LEAVE VIOLATIONS

On March 20, the New York City Council enacted a provision allowing an individual to initiate a private legal action against employers for non-compliance with the Earned Safe and Sick Time Act (ESSTA).

Individuals may now file lawsuits for alleged violations of the Act directly in court, bypassing the need to file an administrative complaint with the Department of Consumer and Worker Protection. Legal action can be initiated within two years from the date the individual became aware or should have been aware of the alleged violation and may seek penalties, injunctive and declaratory relief, legal fees, costs, and other pertinent damages against the violating entity or individual.

Under the Act, the amount of safe and sick leave provided is contingent on the size of the employer.

- Employers with 100 or more employees are required to provide up to 56 hours of paid leave annually.

- Employers with 5 to 99 employees must offer up to 40 hours of paid leave annually.

- Small employers with four or fewer employees and an annual net income exceeding $1 million are obligated to provide up to 40 hours of paid leave. In contrast, if the employer’s net income is less than $1 million, they are only required to offer up to 40 hours of unpaid leave annually.

- Employers with one or more domestic workers must provide up to 40 hours of paid leave annually, with an increase to 56 hours for employers with 100 or more domestic workers.

Eligible employees are entitled to use accrued safe and sick leave immediately, including newly hired personnel. In cases of unforeseen leave, employers cannot mandate advance notice but can request documentation for absences exceeding three consecutive workdays. Employers must provide employees with written policy details regarding safe and sick leave, including information about accrued, utilized, and total leave balances, either on paystubs or via an accessible electronic system.

Significant amendments to the were implemented on October 15, 2023, to clarify the Act:

- The assessment of an employer’s size is based on the total number of employees nationwide, determined by the peak number of concurrently employed staff within a calendar year.

- Full time, part-time, joint employees, and employees on leave of absence are included in the employee count for determining employer size.

- Employees telecommuting from outside New York City are not considered employed within the city.

- Employees based outside of New York City that are “expected to regularly perform work in New York City during a calendar year” will be counted, but only for hours worked by the employee within New York City.

EMPLOYER CONSIDERATIONS

In light of these developments, it is imperative for New York City employers to thoroughly review their safe and sick leave policies to ensure full compliance and mitigate the risk of potential litigation.

QUESTION OF THE MONTH

Q: If an employee carries her full family on a qualified high deductible health plan (QHDHP) but her children are mandated to also be enrolled in Medicaid, can she contribute the full family amount to her health savings account (HSA)?

A: If the owner of the HSA (employee) is only eligible for the HDHP and the employee has enrolled in family coverage, the employee can contribute the full family limit to the HSA even if the employee’s dependents are not otherwise eligible due to Medicaid.

Answers to the Question of the Week are provided by Kutak Rock LLP. Kutak Rock provides general compliance guidance through the UBA Compliance Help Desk, which does not constitute legal advice or create an attorney-client relationship. Please consult your legal advisor for specific legal advice.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. | |

| ©2024 United Benefit Advisors |