by admin | Aug 2, 2024 | Employee Benefits

Managing healthcare costs can feel like deciphering a complex code. Three acronyms frequently pop up: HSAs, HRAs, and FSAs. But what exactly do they mean, and which one is right for you? Let’s break down these accounts and explore how they can help you save on qualified medical expenses.

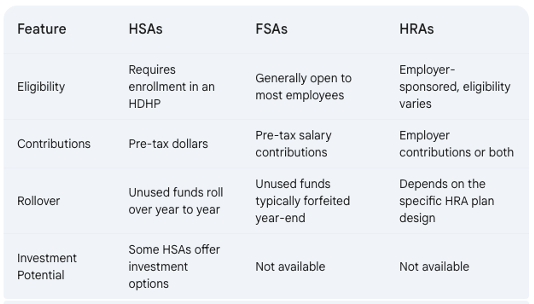

Understanding the Accounts:

-

Health Savings Accounts (HSAs): You contribute pre-tax dollars to your HSA, which acts like a savings account dedicated to qualified medical expenses, including most over-the-counter (OTC) medications. However, to be eligible for an HSA, you must be enrolled in an High Deductible Health Plan (HDHP), which has a higher deductible than traditional health insurance plans. This means you’ll pay more out-of-pocket before your insurance kicks in. HSAs essentially act as a safety net to offset these higher deductible costs.

-

Flexible Spending Accounts (FSAs): These accounts allow you to set aside pre-tax salary contributions to cover qualified medical and dependent care expenses throughout the year. Think of it like a prepaid debit card for approved healthcare costs. Most OTC medications are eligible for reimbursement through an FSA debit card or claim submission process. Unlike HSAs, FSAs are not tied to a specific health insurance plan type, so you might have the option to contribute to an FSA even with a traditional plan (though some employers may have restrictions based on your plan selection). o FSAs have a “use it or lose it” provision: Generally, you must use the money in a FSA within the plan year (but occasionally your employer can offer a grace period of a few months).

-

Health Reimbursement Arrangements (HRAs): These employer-sponsored accounts let companies contribute funds to cover qualified employee medical expenses. The specific eligible expenses, including OTC items, vary depending on the HRA plan design set by your employer. Unlike HSAs and FSAs, you don’t directly contribute to an HRA. Instead, your employer contributes on your behalf, or in some cases, a combination of employer and employee contributions may be allowed.

Who Can Use Them?

-

HSAs: Eligibility hinges on having an HDHP.

-

FSAs: Generally available to most employees, regardless of health plan type (though some employers may restrict enrollment based on plan selection).

-

HRAs: Offered at the discretion of your employer, who determines eligibility and contribution levels.

Tax Benefits:

All three accounts offer tax advantages:

-

Contributions: Reduce your taxable income by contributing pre-tax dollars.

-

Growth: Interest earned on the funds in HSAs and some FSAs (depending on the plan) grows tax-free, allowing your savings to accumulate faster.

-

Withdrawals: When used for qualified medical expenses, withdrawals are tax-free for all three accounts.

Key Differences:

Choosing the Right Account for You:

The best account for you depends on your individual circumstances. Here are some factors to consider:

- Health Status: If you’re generally healthy and have predictable medical expenses, an FSA might be a good choice, allowing you to use the funds throughout the year.

- Financial Risk Tolerance: HSAs offer long-term savings potential with rollovers and investment options (in some plans). However, they require enrollment in an HDHP, which means you’ll shoulder higher upfront costs before insurance kicks in. Consider your comfort level with potentially higher out-of-pocket expenses.

- Employer Benefits: HRAs depend on your employer’s plan design. If your employer offers a generous HRA with significant contributions, it might be a good option for you.

Additional Considerations:

- Use-It-or-Lose-It vs. Rollover: FSAs typically operate on a “use-it-or-lose-it” basis, so plan your contributions carefully to avoid losing funds.

Making an Informed Decision:

By thoroughly understanding HSAs, FSAs, and HRAs, you can choose the account that best aligns with your health needs, financial goals, and employer benefits, ultimately saving you money on healthcare expenses.

by admin | Nov 14, 2018 | Compliance, Hot Topics

The Department of the Treasury (Treasury), Department of Labor (DOL), and Department of Health and Human Services (HHS) (collectively, the Departments) released their proposed rule regarding health reimbursement arrangements (HRAs) and other account-based group health plans. The DOL also issued a news release and fact sheet on the proposed rule.

The proposed rule’s goal is to expand the flexibility and use of HRAs to provide individuals with additional options to obtain quality, affordable healthcare. According to the Departments, these changes will facilitate a more efficient healthcare system by increasing employees’ consumer choice and promoting healthcare market competition by adding employer options.

To do so, the proposed rules would expand the use of HRAs by:

- Removing the current prohibition against integrating an HRA with individual health insurance coverage (individual coverage)

- Expanding the definition of limited excepted benefits to recognize certain HRAs as limited excepted benefits if certain conditions are met (excepted benefit HRA)

- Providing premium tax credit (PTC) eligibility rules for people who are offered an HRA integrated with individual coverage

- Assuring HRA and Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) plan sponsors that reimbursement of individual coverage by the HRA or QSEHRA does not become part of an ERISA plan when certain conditions are met

- Changing individual market special enrollment periods for individuals who gain access to HRAs integrated with individual coverage or who are provided QSEHRAs

Public comments are due by December 28, 2018. If the proposed rule is finalized, it will be effective for plan years beginning on or after January 1, 2020.

by Karen Hsu

Originally posted on ubabenefits.com

by admin | Nov 7, 2018 | ACA, Compliance, Human Resources, IRS

On November 5, 2018, the Internal Revenue Service (IRS) released Notice 2018-85 to announce that the health plan Patient-Centered Outcomes Research Institute (PCORI) fee for plan years ending between October 1, 2018 and September 30, 2019 will be $2.45 per plan participant. This is an increase from the prior year’s fee of $2.39 due to an inflation adjustment.

Background

The Affordable Care Act created the PCORI to study clinical effectiveness and health outcomes. To finance the nonprofit institute’s work, a small annual fee — commonly called the PCORI fee — is charged on group health plans.

The fee is an annual amount multiplied by the number of plan participants. The dollar amount of the fee is based on the ending date of the plan year. For instance:

- For plan year ending between October 1, 2017 and September 30, 2018: $2.39.

- For plan year ending between October 1, 2018 and September 30, 2019: $2.45.

Insurers are responsible for calculating and paying the fee for insured plans. For self-funded health plans, however, the employer sponsor is responsible for calculating and paying the fee. Payment is due by filing Form 720 by July 31 following the end of the calendar year in which the health plan year ends. For example, if the group health plan year ends December 31, 2018, Form 720 must be filed along with payment no later than July 31, 2019.

Certain types of health plans are exempt from the fee, such as:

- Stand-alone dental and/or vision plans;

- Employee assistance, disease management, and wellness programs that do not provide significant medical care benefits;

- Stop-loss insurance policies; and

- Health savings accounts (HSAs).

HRAs and QSEHRAs

A traditional health reimbursement arrangement (HRA) is exempt from the PCORI fee, provided that it is integrated with another self-funded health plan sponsored by the same employer. In that case, the employer pays the PCORI fee with respect to its self-funded plan, but does not pay again just for the HRA component. If, however, the HRA is integrated with a group insurance health plan, the insurer will pay the PCORI fee with respect to the insured coverage and the employer pays the fee for the HRA component.

A qualified small employer health reimbursement arrangement (QSEHRA) works a little differently. A QSEHRA is a special type of tax-preferred arrangement that can only be offered by small employers (generally those with fewer than 50 employees) that do not offer any other health plan to their workers. Since the QSEHRA is not integrated with another plan, the PCORI fee applies to the QSEHRA. Small employers that sponsor a QSEHRA are responsible for reporting and paying the PCORI fee.

PCORI Nears its End

The PCORI program will sunset in 2019. The last payment will apply to plan years that end by September 30, 2019 and that payment will be due in July 2020. There will not be any PCORI fee for plan years that end on October 1, 2019 or later.

Resources

The IRS provides the following guidance to help plan sponsors calculate, report, and pay the PCORI fee:

Originally posted on thinkhr.com

by admin | Mar 14, 2018 | ACA, HSA/HRA, IRS

Taking control of health care expenses is on the top of most people’s to-do list for 2018. The average premium increase for 2018 is 18% for Affordable Care Act (ACA) plans. So, how do you save money on health care when the costs seems to keep increasing faster than wage increases? One way is through medical savings accounts.

Medical savings accounts are used in conjunction with High Deductible Health Plans (HDHP) and allow savers to use their pre-tax dollars to pay for qualified health care expenses. There are three major types of medical savings accounts as defined by the IRS. The Health Savings Account (HSA) is funded through an employer and is usually part of a salary reduction agreement. The employer establishes this account and contributes toward it through payroll deductions. The employee uses the balance to pay for qualified health care costs. Money in HSA is not forfeited at the end of the year if the employee does not use it. The Health Flexible Savings Account (FSA) can be funded by the employer, employee, or any other contributor. These pre-tax dollars are not part of a salary reduction plan and can be used for approved health care expenses. Money in this account can be rolled over by one of two ways: 1) balance used in first 2.5 months of new year or 2) up to $500 rolled over to new year. The third type of savings account is the Health Reimbursement Arrangement (HRA). This account may only be contributed to by the employer and is not included in the employee’s income. The employee then uses these contributions to pay for qualified medical expenses and the unused funds can be rolled over year to year.

There are many benefits to participating in a medical savings account. One major benefit is the control it gives to employee when paying for health care. As we move to a more consumer driven health plan arrangement, the individual can make informed choices on their medical expenses. They can “shop around” to get better pricing on everything from MRIs to prescription drugs. By placing the control of the funds back in the employee’s hands, the employer also sees a cost savings. Reduction in premiums as well as administrative costs are attractive to employers as they look to set up these accounts for their workforce. The ability to set aside funds pre-tax is advantageous to the savings savvy individual. The interest earned on these accounts is also tax-free.

The federal government made adjustments to contribution limits for medical savings accounts for 2018. For an individual purchasing single medical coverage, the yearly limit increased $50 from 2017 to a new total $3450. Family contribution limits also increased to $6850 for this year. Those over the age of 55 with single medical plans are now allowed to contribute $4450 and for families with the insurance provider over 55 the new limit is $7900.

Health care consumers can find ways to save money even as the cost of medical care increases. Contributing to health savings accounts benefits both the employee as well as the employer with cost savings on premiums and better informed choices on where to spend those medical dollars. The savings gained on these accounts even end up rewarding the consumer for making healthier lifestyle choices with lower out-of-pocket expenses for medical care. That’s a win-win for the healthy consumer!

by admin | Jun 9, 2017 | HSA/HRA, IRS

IRS Releases 2018 Amounts for HSAs

The IRS released Revenue Procedure 2017-37 that sets the dollar limits for health savings accounts (HSAs) and high-deductible health plans (HDHPs) for 2018.

For calendar year 2018, the annual contribution limit for an individual with self-only coverage under an HDHP is $3,450, and the annual contribution limit for an individual with family coverage under an HDHP is $6,900. How much should an employer contribute to an HSA? Read our latest news release for information on modest contribution strategies that are still driving enrollment in HSA and HRA plans.

For calendar year 2018, a “high deductible health plan” is defined as a health plan with an annual deductible that is not less than $1,350 for self-only coverage or $2,700 for family coverage, and the annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) do not exceed $6,650 for self-only coverage or $13,300 for family coverage.

Retroactive Medicare Coverage Effect on HSA Contributions

The Internal Revenue Service (IRS) recently released a letter regarding retroactive Medicare coverage and health savings account (HSA) contributions.

As background, Medicare Part A coverage begins the month an individual turns age 65, provided the individual files an application for Medicare Part A (or for Social Security or Railroad Retirement Board benefits) within six months of the month in which the individual turns age 65. If the individual files an application more than six months after turning age 65, Medicare Part A coverage will be retroactive for six months.

Individuals who delayed applying for Medicare and were later covered by Medicare retroactively to the month they turned 65 (or six months, if later) cannot make contributions to the HSA for the period of retroactive coverage. There are no exceptions to this rule.

However, if they contributed to an HSA during the months that were retroactively covered by Medicare and, as a result, had contributions in excess of the annual limitation, they may withdraw the excess contributions (and any net income attributable to the excess contribution) from the HSA.

They can make the withdrawal without penalty if they do so by the due date for the return (with extensions). Further, an individual generally may withdraw amounts from an HSA after reaching Medicare eligibility age without penalty. (However, the individual must include both types of withdrawals in income for federal tax purposes to the extent the amounts were previously excluded from taxable income.)

If an excess contribution is not withdrawn by the due date of the federal tax return for the taxable year, it is subject to an excise tax under the Internal Revenue Code. This tax is intended to recapture the benefits of any tax-free earning on the excess contribution.

By Danielle Capilla

Originally Posted By www.ubabenefits.com