On November 5, 2018, the Internal Revenue Service (IRS) released Notice 2018-85 to announce that the health plan Patient-Centered Outcomes Research Institute (PCORI) fee for plan years ending between October 1, 2018 and September 30, 2019 will be $2.45 per plan participant. This is an increase from the prior year’s fee of $2.39 due to an inflation adjustment.

Background

The Affordable Care Act created the PCORI to study clinical effectiveness and health outcomes. To finance the nonprofit institute’s work, a small annual fee — commonly called the PCORI fee — is charged on group health plans.

The fee is an annual amount multiplied by the number of plan participants. The dollar amount of the fee is based on the ending date of the plan year. For instance:

For plan year ending between October 1, 2017 and September 30, 2018: $2.39.

For plan year ending between October 1, 2018 and September 30, 2019: $2.45.

Insurers are responsible for calculating and paying the fee for insured plans. For self-funded health plans, however, the employer sponsor is responsible for calculating and paying the fee. Payment is due by filing Form 720 by July 31 following the end of the calendar year in which the health plan year ends. For example, if the group health plan year ends December 31, 2018, Form 720 must be filed along with payment no later than July 31, 2019.

Certain types of health plans are exempt from the fee, such as:

Stand-alone dental and/or vision plans;

Employee assistance, disease management, and wellness programs that do not provide significant medical care benefits;

Stop-loss insurance policies; and

Health savings accounts (HSAs).

HRAs and QSEHRAs

A traditional health reimbursement arrangement (HRA) is exempt from the PCORI fee, provided that it is integrated with another self-funded health plan sponsored by the same employer. In that case, the employer pays the PCORI fee with respect to its self-funded plan, but does not pay again just for the HRA component. If, however, the HRA is integrated with a group insurance health plan, the insurer will pay the PCORI fee with respect to the insured coverage and the employer pays the fee for the HRA component.

A qualified small employer health reimbursement arrangement (QSEHRA) works a little differently. A QSEHRA is a special type of tax-preferred arrangement that can only be offered by small employers (generally those with fewer than 50 employees) that do not offer any other health plan to their workers. Since the QSEHRA is not integrated with another plan, the PCORI fee applies to the QSEHRA. Small employers that sponsor a QSEHRA are responsible for reporting and paying the PCORI fee.

PCORI Nears its End

The PCORI program will sunset in 2019. The last payment will apply to plan years that end by September 30, 2019 and that payment will be due in July 2020. There will not be any PCORI fee for plan years that end on October 1, 2019 or later.

Resources

The IRS provides the following guidance to help plan sponsors calculate, report, and pay the PCORI fee:

Friday, April 27, the Internal Revenue Service (IRS) announced that the 2018 annual contribution limit to Health Savings Accounts (HSAs) for persons with family coverage under a qualifying High Deductible Health Plan (HDHP) is restored to $6,900. The single-coverage limit of $3,450 is not affected.

This is the final word on what has been an unusual back-and-forth saga. The 2018 family limit of $6,900 had been announced in May 2017. Following passage of the Tax Cuts and Jobs Act in December 2017, however, the IRS was required to modify the methodology used in determining annual inflation-adjusted benefit limits. On March 5, 2018, the IRS announced the 2018 family limit was reduced by $50, retroactively, from $6,900 to $6,850. Since the 2018 tax year was already in progress, this small change was going to require HSA trustees and recordkeepers to implement not-so-small fixes to their systems. The IRS has listened to appeals from the industry, and now is providing relief by reinstating the original 2018 family limit of $6,900.

Employers that offer HSAs to their workers will receive information from their HSA administrator or trustee regarding any updates needed in their payroll files, systems, and employee communications. Note that some administrators had held off making changes after the IRS announcement in March, with the hopes that the IRS would change its position and restore the original limit. So employers will need to consider their specific case with their administrator to determine what steps are needed now.

HSA Summary

An HSA is a tax-exempt savings account employees can use to pay for qualified health expenses. To be eligible to contribute to an HSA, an employee:

Must be covered by a qualified high deductible health plan (HDHP);

Must not have any disqualifying health coverage (called “impermissible non-HDHP coverage”);

Must not be enrolled in Medicare; and

May not be claimed as a dependent on someone else’s tax return.

HSA 2018 Limits

Limits apply to HSAs based on whether an individual has self-only or family coverage under the qualifying HDHP. 2018 HSA contribution limit:

Single: $3,450

Family: $6,900

Catch-up contributions for those age 55 and older remains at $1,000

2018 HDHP minimum deductible (not applicable to preventive services):

Single: $1,350

Family: $2,700

2018 HDHP maximum out-of-pocket limit:

Single: $6,650

Family: $13,300*

*If the HDHP is a nongrandfathered plan, a per-person limit of $7,350 also will apply due to the ACA’s cost-sharing provision for essential health benefits.

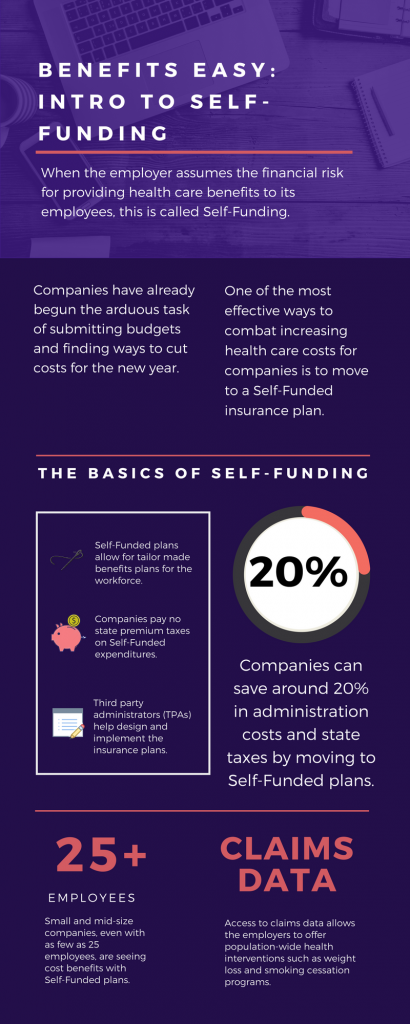

As we head into the second month of 2018, companies have already begun the arduous task of submitting budgets and finding ways to cut costs for the new year. One of the most effective ways to combat increasing health care costs for companies is to move to a Self-Funded insurance plan. By paying for claims out-of-pocket instead of paying a premium to an insurance carrier, companies can save around 20% in administration costs and state taxes. That’s quite a cost savings!

The topic of Self-Funding is huge and so we want to break it down into smaller bites for you to digest. This month we want to tackle a basic introduction to Self-Funding and in the coming months, we will cover the benefits, risks, and the stop-loss associated with this type of plan. THE BASICS

When the employer assumes the financial risk for providing health care benefits to its employees, this is called Self-Funding.

Self-Funded plans allow the employer to tailor the benefits plan design to best suit their employees. Employers can look at the demographics of their workforce and decide which benefits would be most utilized as well as cut benefits that are forecasted to be underutilized.

While previously most used by large companies, small and mid-sized companies, even with as few as 25 employees, are seeing cost benefits to moving to Self-Funded insurance plans.

Companies pay no state premium taxes on self-funded expenditures. This savings is around 1.5% – 3/5% depending on in which state the company operates.

Since employers are paying for claims, they have access to claims data. While keeping within HIPAA privacy guidelines, the employer can identify and reach out to employees with certain at-risk conditions (diabetes, heart disease, stroke) and offer assistance with combating these health concerns. This also allows greater population-wide health intervention like weight loss programs and smoking cessation assistance.

Companies typically hire third-party administrators (TPA) to help design and administer the insurance plans. This allows greater control of the plan benefits and claims payments for the company.

As you can see, Self-Funding has many facets. It’s important to gather as much information as you can and weigh the benefits and risks of moving from a Fully-Funded plan for your company to a Self-Funded one. Doing your research and making the move to a Self-Funded plan could help you gain greater control over your healthcare costs and allow you to design an original plan that best fits your employees.

Two tri-agency (Internal Revenue Service, Employee Benefits Security Administration, and Centers for Medicare and Medicaid Services) Interim Final Rules were released and became effective on October 6, 2017, and were published on October 13, 2017, allowing a greater number of employers to opt out of providing contraception to employees at no cost through their employer-sponsored health plan. The expanded exemption encompasses all non-governmental plan sponsors that object based on sincerely held religious beliefs, and institutions of higher education in their arrangement of student health plans. The exemption also now encompasses employers who object to providing contraception coverage on the basis of sincerely held moral objections and institutions of higher education in their arrangement of student health plans. Furthermore, if an issuer of health coverage (an insurance company) had sincere religious beliefs or moral objections, it would be exempt from having to sell coverage that provides contraception. The exemptions apply to both non-profit and for-profit entities.

The currently-in-place accommodation is also maintained as an optional process for exempt employers, and will provide contraceptive availability for persons covered by the plans of entities that use it (a legitimate program purpose). These rules leave in place the government’s discretion to continue to require contraceptive and sterilization coverage where no such objection exists. These interim final rules also maintain the existence of an accommodation process, but consistent with expansion of the exemption, the process is optional for eligible organizations. Effectively this removes a prior requirement that an employer be a “closely held for-profit” employer to utilize the exemption.

On November 30, 2017, the Centers for Medicare and Medicaid Services (CMS) released guidance on accommodation revocation notices. Plan participants and beneficiaries must receive written notice if an objecting employer had previously used the accommodation and, under the new exemptions, no longer wishes to use the accommodation process. The Interim Final Rules required the issuer to provide written revocation notice to plan participants and beneficiaries. CMS’ recent guidance clarifies that the employer, its group health plan, or its third-party administrator (TPA) may provide written revocation notice instead of the issuer.

CMS’ guidance also clarifies the timing of the revocation notice. Under the Interim Final Rules, revocation is effective on the first day of the first plan year that begins on or after 30 days after the revocation date. Alternatively, if the plan or issuer listed the contraceptive benefit in its Summary of Benefits and Coverage (SBC), then the plan or issuer must give at least 60 days prior notice of the accommodation revocation (SBC notification process). CMS’ guidance indicates that, even if the plan or issuer did not list the contraceptive benefit in its SBC, the employer is permitted to use the 60-day advance notice method to revoke the accommodation as long as the revocation is consistent with any other applicable laws and contract provisions regarding benefits modification.

Further, if the employer chooses not to use the SBC notification process to notify plan participants and beneficiaries of the accommodation revocation and if the employer instructs its issuer or TPA not to use the SBC notification process on the employer’s behalf, then the employer, its plan, issuer, or TPA must send a separate written revocation notice to plan participants and beneficiaries no later than 30 days before the first day of the first plan year in which the revocation will be effective.

Unlike the SBC notification process, which would allow mid-year benefit modification, if an employer uses the 30-day notification process, the modification can only be effective at the beginning of a plan year.

Employers that object to providing contraception on the basis of sincerely held religious beliefs or moral objections, who were previously required to offer contraceptive coverage at no cost, and that wish to remove the benefit from their medical plan are still subject (as applicable) to ERISA, its plan document and SPD requirements, notice requirements, and disclosure requirements relating to a reduction in covered services or benefits. These employers would be obligated to update their plan documents, SBCs, and other reference materials accordingly, and provide notice as required.

Employers are also now permitted to offer group or individual health coverage, separate from the current group health plans, that omits contraception coverage for employees who object to coverage or payment for contraceptive services, if that employee has sincerely held religious beliefs relating to contraception. All other requirements regarding coverage offered to employees would remain in place. Practically speaking, employers should be cautious in issuing individual policies until further guidance is issued, due to other regulations and prohibitions that exist.

By Danielle Capilla

Originally Published By United Benefit Advisors