by admin | May 23, 2023 | Compliance

2024 BENEFIT PARAMETERS FOR MEDICARE PART D CREDITABLE COVERAGE DISCLOSURES ANNOUNCED

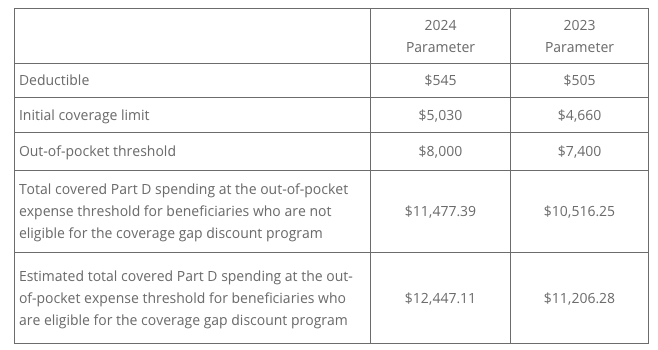

The Centers for Medicare and Medicaid Services (CMS) released a Fact Sheet announcing the 2024 benefit parameters for Medicare Part D. These factors are used to determine the actuarial value of defined standard Medicare Part D coverage under CMS guidelines.

Each year, Medicare Part D requires that employers offering prescription drug coverage to Part D eligible individuals (including active or disabled employees, retirees, COBRA participants, and beneficiaries) disclose to those individuals and CMS whether the prescription plan coverage offered is creditable or non-creditable. Creditable coverage meets or exceeds the value of defined standard Medicare Part D coverage.

Insurance carriers and providers of the prescription benefit will typically notify the plan sponsor if their prescription plan is creditable or non-creditable. The 2024 parameters for Medicare Part D are:

The Online Disclosure to CMS Form must be submitted to CMS annually, and upon any change that affects whether the drug coverage is creditable:

- Within 60 days after the beginning date of the plan year

- Within 30 days after the termination of the prescription drug plan

- Within 30 days after any change in the creditable coverage status of the prescription drug plan

QUESTION OF THE MONTH

Q: Where can I find the updated RxDC reporting instructions?

A: The most recent version of the reporting instructions and templates can be found on the Centers for Medicare and Medicaid website.

To receive an email when the instructions are updated, create a Registration for Technical Assistance Portal (REGTAP) account. Select the checkbox “Please send me updates for the Consolidated Appropriations Act / No Surprises Act” in your account settings.

© UBA. All rights reserved.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. |

by admin | Apr 10, 2023 | Compliance

IRS RELEASES 2024 EMPLOYER SHARED RESPONSIBILITY PROVISION PENALTIES

The dollar amount used to calculate the employer shared responsibility provision penalties (ESRP) has been provided for 2024.

As background, the penalties can be assessed under Code § 4980H(a) if an applicable large employer (ALE) fails to offer minimum essential coverage to the required number of full-time employees (and their dependents) through a qualified group health plan for any month.

Additionally, ALEs may be subject to a Code § 4980H(b) penalty if they offer minimum essential coverage to the required number of full-time employees, but the offered coverage is not affordable or does not provide minimum value.

The adjusted penalty amount per full-time employee for non-compliance occurring in the 2024 calendar year will be $2,970 under Code § 4980H(a) and $4,460 under Code §4980H(b).

GUIDANCE ON GAG CLAUSE PROHIBITION FOR HEALTH PLAN AGREEMENTS

Additional guidance was issued by the Department of Labor (DOL), the Department of Health and Human Services (HHS), and the Internal Revenue Service (IRS) (the “Agencies”) on the gag clause provision of the Consolidated Appropriations Act of 2021 (CAA). The guidance addresses questions from stakeholders to help people understand the law and promote compliance. The FAQs speak to the CAA’s annual attestation, prohibiting group health plans from preventing specific disclosures regarding provider cost or quality-of-care information as well as a gag clause prohibition. This prohibition specifically applies to agreements between group health plans or insurers and providers, third-party administrators (TPAs), or other service providers. Further, the FAQs explained that a gag clause is a “contractual term that directly or indirectly restricts specific data and information that a plan or issuer can make available to another party.”

Health plans, insurers, and other health plan vendors must attest to their compliance with the gag clause prohibition annually, beginning no later than December 31, 2023, with subsequent attestations due each December 31. Visit the Centers for Medicare and Medicaid Services (CMS) website for instructions, a user manual, and reporting template. Plans and issuers should submit an annual attestation of compliance at https://hios.cms.gov/HIOS-GCPCA-UI.

CMS FACT SHEET PROVIDES FACT SHEET FOR CONSUMERS ABOUT END OF COVID-19 PUBLIC HEALTH EMERGENCY

The Centers for Medicare & Medicaid Services (CMS) issued a consumer-facing fact sheet to help individuals know what to expect at the end of the COVID-19 Public Health Emergency (PHE). The Department of Health and Human Services is planning for the federal PHE and the COVID-19 national emergency to expire at the end of the day on May 11, 2023. This will trigger the 60-day countdown to the end of the outbreak period and the end of the tolling period for many plan-related deadlines.

This fact sheet covers COVID-19 vaccines, testing, and treatments; telehealth services; continuing flexibilities for health care professionals; and expanded hospital capacity by providing inpatient care in a patient’s home.

IRS ISSUES FAQS ON NUTRITION, WELLNESS, AND GENERAL HEALTH EXPENSES

The IRS has provided FAQs to explain how health flexible spending arrangement (FSAs), health reimbursement arrangements (HRAs) and health savings accounts (HSAs) can be used to pay for or reimburse eligible medical expenses related to nutrition, wellness, and general health under Internal Revenue Code Section 213.

Medical expenses are defined as the costs of diagnosis, cure, mitigation, treatment, or prevention of disease, and for the purpose of affecting any part or function of the body and must be primarily to alleviate or prevent a physical or mental disability or illness. Not included are expenses that are merely beneficial to general health.

IRS TO REQUIRE ELECTRONIC FILING FOR MOST EMPLOYER RETURNS STARTING IN 2024

A final rule issued by the IRS addresses a change in the way employers file certain forms. Beginning in 2024, employers will be required to aggregate most information returns, including W-2, 1099, ACA reporting Forms 1094-B/1095-B and Forms 1094-C/1095-C, and Form 5330 (Return of Excise Taxes Related to Employee Benefit Plans) among others. Once aggregated, forms totaling ten or more must be submitted electronically.

Previously, an employer was not required to file electronically unless were filing at least 250 of the same form.

Any corresponding corrected returns must also be filed electronically. Waivers may be available for those facing an undue hardship related to the cost of filing electronically. Applicable penalties will apply for non-electronic filing when electronic filing is required. See the IRS website for information on secure filing of electronic tax information.

QUESTION OF THE MONTH

Q: What is a “gag clause?”

A: In general a “gag clause” is a contractual term that directly or indirectly restricts specific data and information that a plan or issuer can make available to another party. Gag clauses in this context might be found in agreements between a plan or issuer and any of the following parties:

- a health care provider

- a network or association of providers

- a TPA

- another service provider offering access to a network of providers

© UBA. All rights reserved.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. |

by admin | Apr 4, 2023 | Benefit Plan Tips, Tricks and Traps, Compliance

When the COVID-19 public health emergency and national emergency were declared in 2020, no one anticipated they would still be in place in 2023.

On January 30, 2023, the President announced the intent to end the emergencies on May 11, 2023. The impact of the emergencies on employer-sponsored benefits affected certain coverages, reimbursements, and timelines. Multiple laws and regulations passed after 2020 created temporary rules tied to the end of the emergencies. As a result, employers will face significant tasks and obligations to unwind the changes from the last three years.

There are two areas of significance for employers: free coverages that will end, and required deadlines that will begin. Here’s what you need to keep in mind for each:

1. Free coverages that will end

The Families First Coronavirus Response Act (FFCRA) required health plans to cover the cost of COVID-19 testing and related services with no cost-sharing. The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) expanded the FFCRA by adding over-the-counter tests and vaccinations by out-of-network providers.

When the emergency ends, this required no-cost coverage of testing and related services will sunset. Employers with fully insured plans should speak with their carrier to discuss whether there will be any option to continue the coverage with no cost-sharing. Each state’s Department of Insurance should provide guidance to carriers on when cost-sharing will resume. Self-funded groups may have more flexibility to continue to offer testing and related services with no-cost sharing. Due to the Affordable Care Act’s preventative services requirement, fully approved COVID-19 vaccines will remain covered, without cost, by in-network providers. A reduction in coverage will require a 60-day advance notice to affected employees.

Another specific impact is stand-alone telehealth benefits. Employees who were ineligible for their employer’s health plan were permitted to enroll in stand-alone telehealth benefits. The relief applies for the plan year that begins on or before the end of the emergency. An employer providing stand-alone telehealth will not be able to continue the coverage past the end of the current plan year and should review their policy to modify the language for stand-alone coverage. A reduction in coverage requires sending a notice to affected employees 60 days prior to the plan year end date.

2. Required deadlines that will begin

Many provisions of the last three years are tied to outbreak period rules issued in May 2020. The outbreak period lasts until 60 days after the end of the national emergency. These rules extended several key deadlines related to COBRA, special enrollment periods, claim submission, and appeal processes.

The Employee Benefits Services Administration issued a notice in 2021 providing guidance and clarity for employers, stating that the maximum period a deadline may extend is the earlier of one year from the date an original deadline would begin, or 60 days after the end of the outbreak period. This one-year period is known as tolling.

The challenge for employers will be tracking each individual’s tolling period as the end of the outbreak period nears. For example, an employee traditionally has 60 days to elect COBRA continuation coverage. The 60-day deadline would not begin until one year and 60 days later or 60 days after the outbreak period.

To illustrate this, imagine this scenario:

- Employee A’s benefits were terminated on December 31, 2022.

- Traditionally, they would have until March 2023 to elect COBRA.

- The relief states the 60-day countdown would not begin until the earlier of one year (December 2023) or July 10, 2023 (60 days after the end of the outbreak period).

- Since the outbreak period end date is planned for May 11, 2023, which is earlier than the one-year tolling, Employee A must make their COBRA election by September 20, 2023.

The tolling period has been a point of confusion for employers and may be more confusing as the outbreak period now has a planned end date of May 11, 2023.

The Department of Health and Human Services (HHS) provided a roadmap on February 9, 2022, outlining what may and may not be affected by the end of the emergencies. HHS also indicated it will continue “to review the flexibilities and policies implemented during the COVID-19 PHE to determine whether others can and should remain in place, even for a temporary duration, to facilitate jurisdictions’ ability to provide care and resources to Americans.”

Employers and plan sponsors should continue monitoring federal and state government resources. Employers may need to revise plan documents and provide new notifications to employees when coverage is changed or eliminated.

By Angela Surra

Originally posted on Mineral

by admin | Jul 18, 2022 | Compliance

By way of background, the Affordable Care Act (ACA) created the Patient-Centered Outcomes Research Institute (PCORI) to study clinical effectiveness and health outcomes. To finance the Institute’s work, a small annual fee—commonly called the PCORI fee—is charged on group health plans. Grandfathered health plans are not exempt.

Most employers do not have to take any action because employer-sponsored health plans are commonly provided through group insurance contracts. For insured plans, the carrier is responsible for calculating and paying the PCORI fee and the employer has no additional duties.

However, employers that sponsor self-funded group health plans are responsible for calculating, reporting, and paying this fee each year.

The PCORI fee applies for each plan year based on the plan year end date. The fee is an annual amount multiplied by the number of plan participants.

$2.66 per year, per participant, for plan years ending between October 1, 2020 and September 30, 2021.

$2.79 per year, per participant, for plan years ending between October 1, 2021 and September 30, 2022.

Payment is due by July 31st in the following calendar year in which the plan year ends. Because the due date in 2022 falls on Sunday, you may file the return on the next business day. This year, payment is due on Monday, August 1, 2022. Use IRS Form 720, Quarterly Federal Excise Tax Return.

Does the PCORI fee apply to all health plans?

The fee applies to all health plans and HRAs, excluding the following:

Plans that primarily provide “excepted benefits” (e.g., stand-alone dental and vision plans, most health flexible spending accounts with little or no employer contributions, and certain supplemental or gap-type plans).

Plans that do not provide significant benefits for medical care or treatment (e.g., employee assistance, disease management, and wellness programs).

Stop-loss insurance policies.

Health savings accounts (HSAs).

The IRS provides a helpful chart indicating the types of health plans that are, or are not, subject to the PCORI fee.

Which quarter do self-funded employers report on by August 1st?

For the purposes of the 2022 PCORI obligations, this would be the 2nd Quarter of 2022. So, when completing Form 720 be sure to fill in the circle for “2nd Quarter.”

Caution! Before taking any action, confirm with your tax department or controller whether your organization files Form 720 for any purposes other than the PCORI fee. For instance, some employers use Form 720 to make quarterly payments for environmental taxes, fuel taxes, or other excise taxes. In that case, do not prepare Form 720 (or the payment voucher), but instead give the PCORI fee information to your organization’s tax preparer to include with its second quarterly filing.

If I have multiple self-insured plans, does the fee apply to each one?

Yes. For instance, if you self-insure one medical plan for active employees and another medical plan for retirees, you will need to calculate, report, and pay the fee for each plan. There is an exception, though, for “multiple self-insured arrangements” that are sponsored by the same employer, cover the same participants, and have the same plan year. For example, if you self-insure a medical plan with a self-insured prescription drug plan, you would pay the PCORI fee only once with respect to the combined plan.

What about hybrid plans such as level-funded or partially self-funded?

The terms “level-funded” or “partially self-funded” are not defined by law, so it can mean different things to different carriers, vendors, and employers. In most cases, the terms are intended to refer to a self-funded group medical plan sponsored by an employer who has assumed all financial risk, other than protection under stop-loss insurance. However, this is not absolute. If your hybrid plan is in fact self-funded plan, then the employer is responsible for the paying the PCORI fee. If unsure, check with the state’s insurance commissioner or legal counsel.

Does the fee apply to HRAs?

Yes. The PCORI fee applies to HRAs, which are self-insured health plans, although the fee is waived in some cases. If you self-insure another plan, such as a major medical or high deductible plan, and the HRA is merely a component of that plan, you do not have to pay the PCORI fee separately for the HRA. In other words, when the HRA is integrated with another self-insured plan, you only pay the fee once for the combined plan.

On the other hand, if the HRA stands alone, or if the HRA is integrated with an insured plan, you are responsible for paying the fee for the HRA.

What about QSEHRAs? Does the fee apply?

Yes. A Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is special type of tax-advantaged arrangement that allows small employers to reimburse certain health costs for their workers. Although a QSEHRA is not the same as an HRA, and the rules applying to each type are very different, a QSEHRA is a self-insured health plan for purposes of the PCORI fee. The IRS provides guidance confirming that small employers that offer QSEHRAs must calculate, report, and pay the PCORI fee.

What about ICHRAs and EBHRAs? Does the fee apply?

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is a new type of tax-advantaged arrangement, first offered in 2020, that allows employers to reimburse certain health costs for their workers. The IRS has not provided specific guidance regarding ICHRAs and the PCORI fee, but it appears the fee applies since an ICHRA is a self-insured health plan.

An Excepted Benefits Health Reimbursement Arrangement (EBHRA) also is a self-insured health plan, but it is limited to “excepted benefits,” such as dental and vision care costs. So, the PCORI fee does not apply to EBHRAs.

Can I use ERISA plan assets or employee contributions to pay the fee?

No. The PCORI fee is an employer expense and not a plan expense, so you cannot use ERISA plan assets or employee contributions to pay the fee. (An exception is allowed for certain multiemployer plans (e.g., union trusts) subject to collective bargaining.) Since the fee is paid by the employer as a business expense, it is tax deductible.

How do I calculate the fee for a self-funded plan?

Multiply $2.66 or $2.79 (depending on the specific date the plan year ended in 2021) times the average number of lives covered during the plan year. “Covered lives” are all participants, including employees, dependents, retirees, and COBRA enrollees.

You may use any one of the following counting methods to determine the average number of lives:

- Average Count Method: Count the number of lives covered on each day of the plan year, then divide by the number of days in the plan year.

- Snapshot Method: Count the number of lives covered on the same day each quarter, then divide by the number of quarters (e.g., four). Or count the lives covered on the first of each month, then divide by the number of months (e.g., 12). This method also allows the option — called the “snapshot factor method” — of counting each primary enrollee (e.g., employee) with single coverage as “1” and counting each primary enrollee with family coverage as “2.35.”

- Form 5500 Method: Add together the “beginning of plan year” and “end of plan year” participant counts reported on the Form 5500 for the plan year. There is no need to count dependents using this method since the IRS assumes the sum of the beginning and ending of year counts is close enough to the total number of covered lives. If the plan is employee-only without dependent coverage, divide the sum by 2. (If Form 5500 for the plan year ending in 2021 is not filed by August 1, 2022, you cannot use this counting method.)

Note: For an HRA, QSEHRA or ICHRA, count only the number of primary participants (employees) and disregard any dependents.

How do I report and pay the fee for a self-funded plan?

Use Form 720, Quarterly Excise Tax Return, to report and pay the annual PCORI fee. Report all information for self-insured plan(s) with plan year ending dates in 2021 on the same Form 720. Do not submit more than one Form 720 for the same period with the same Employer Identification Number (EIN), unless you are filing an amended return.

The IRS provides Instructions for Form 720. Here is a quick summary of the items for PCORI:

- Fill in the employer information at the top of the form.

- In Part II, complete line 133(c) and/or line 133(d), as applicable, depending on the plan year ending date(s). If you are reporting multiple plans on the same line, combine the information.

- In Part II, complete line 2 (total).

- In Part III, complete lines 3 and 10.

- Sign and date Form 720 where indicated.

- If paying by check or money order, also complete the payment voucher (Form 720-V) provided on the last page of Form 720. Refer to the Instructions for mailing information.

Summary

If you self-insure one or more health plans or sponsor an HRA, you may be responsible for calculating, reporting, and paying annual PCORI fees. The fee is based on the average number of lives covered during the health plan year. The IRS offers a choice of different counting methods to calculate the plan’s average covered lives. Once you have determined the count, the process for reporting and paying the fee using Form 720 is fairly simple. For plan years ending in 2021, the deadline to file Form 720 and make your payment is August 1, 2022.

By Erin DeBartelo

Originally posted on Mineral

by admin | May 4, 2022 | Compliance

The Departments of Health and Human Services, Labor, and Treasury (the Departments) released Transparency in Coverage (TiC) rules in late 2020 that will require fully insured and self-funded plan sponsors of non-grandfathered group health plans to make important disclosures about in-network and out-of-network rates beginning July 1, 2022. To be ready to meet that deadline, plan sponsors should be coordinating efforts with carriers and third-party administrators (TPAs), as the case may be, to ensure they have the necessary information in the proper format to comply with the new TiC requirements.

Devil in the Details

The TiC rules originally required certain employers to provide “machine readable” files that disclose in-network rates, out-of-network charges and information relating to prescription drug coverage and costs by January 1, 2022. Last year the Departments delayed enforcement of the prescription drug coverage rules indefinitely until they issue additional guidance. However, plan sponsors should be taking steps now to ensure they can publish the required in-network negotiated rates and out-of-network allowed amounts as laid out in the TiC rules by the new July 1 deadline.

The first required file (In-Network Rate File) must show a plan’s negotiated rates for all covered items and services between the plan or carrier and all in-network providers. The second file (Allowed Amount File) will show both the historical payments to, and billed charges from, out-of-network providers. Plan sponsors must be sure this file includes at least 20 historical entries to safeguard individual privacy. The departments have indicated they will provide more specific guidance as to format and content, but so far have not released more details than what we know from the final rules.

Machine-Readable Files

The machine-readable files must include:

• For each option a group medical plan or carrier offers, the identifier for each such option. The identifier is either the insurer Health Insurance Oversight (HIOS) identifier, or if the plan or insurer does not have a HIOS number, the employer identification number (EIN).

• A billing code, which can include a Current Procedural Terminology (CPT) code, Healthcare Common Procedure Coding System (HCPCS) code, Diagnosis-related Group (DRG) code, or a National Drug Code (NDC) or any other common payer identifier. This content element also requires a plain language description for each billing code of each covered item or service.

In-Network Rate File

The In-Network Rate File must show:

• In-network rates for each item or service provided by in-network providers, including any negotiated rates, fee schedule rates used to determine cost-sharing, or derived amounts, whichever rate is applicable to the plan.

• If a rate is percentage-based, include the calculated dollar amount, or the calculated dollar amount for each National Provider Identifier (NPI) identified provider, if rates differ by providers or tiers. Bundled items and services must be identified by relevant code.

Allowed Amount File

The Allowed Amount File must show:

• Unique out-of-network allowed amounts and billed charges with respect to covered items or services, furnished by out-of-network providers during the 90-day period that begins 180 days prior to the publication date of the file.

• The plan or insurer must omit data for a particular item or service and provider when the plan or insurer would be reporting on payment of out-of-network allowed amounts for fewer than 20 different claims for payment under a single plan or coverage. These amounts must also be expressed as dollar amounts and associated with the NPI, Taxpayer Identification Number, and Place of Service Code for each network provider.

What Should You Do?

Plan sponsors will need to update the information in the required files no less frequently than monthly. This will likely require strong coordination with the carrier in an insured plan and with the TPA in a self-funded plan.

The Departments will require the files to be posted to a public website that consumers can use without providing individually identifiable information. The website should be open access and not require passwords, account setup, login credentials or any other barriers to accessing the required information.

The TiC rules recognize that a plan sponsor might not have its own public website on which it will be able to house the required files. But the rules permit plan sponsors to contract with a carrier, TPA or other third party to produce and house the information on a plan’s behalf. However, plans should be aware that they might ultimately remain responsible for any failures.

A carrier will be responsible for any failure if a plan has required it in writing to ensure a plan’s compliance. Self-funded plans can contract to have another entity provide and update required files, too, but the TiC rules do not provide the same level of protection for any failures by a third party in the self-funded context, so plans should be sure to review relevant indemnification provisions in any third-party vendor service agreement.

Many carriers and TPAs have begun reaching out to employer plan sponsors offering to assist in in providing, preparing, updating, and hosting the required files. Employers should be carefully reviewing their service agreements and related contracts to make certain they include specific provisions dealing with all aspects of the required transparency disclosures.

Conclusion

We will continue to monitor the guidance we expect to be coming soon as to certain administrative requirements regarding formatting and hosting of the required forms and provide updates as needed.

© UBA. All rights reserved.

by Johnson and Dugan | Sep 30, 2021 | Compliance, Group Benefit Plans, Medicare

Are you an employer that offers or provides group health coverage to your workers? Does your health plan cover outpatient prescription drugs — either as a medical claim or through a card system? If so, be sure to distribute your plan’s Medicare Part D notice before October 15.

Purpose

Medicare began offering “Part D” plans — optional prescription drug benefit plans sold by private insurance companies and HMOs — to Medicare beneficiaries many years ago. People may enroll in a Part D plan when they first become eligible for Medicare.

If they wait too long, a late enrollment penalty amount is permanently added to the Part D plan premium cost when they do enroll. There is an exception, though, for individuals who are covered under an employer’s group health plan that provides creditable coverage. (“Creditable” means that the group plan’s drug benefits are actuarially equivalent or better than the benefits required in a Part D plan.) In that case, the individual can delay enrolling for a Part D plan while he or she remains covered under the employer’s creditable plan. Medicare will waive the late enrollment premium penalty for individuals who enroll in a Part D plan after their initial eligibility date if they were covered by an employer’s creditable plan. To avoid the late enrollment penalty, there cannot be a gap longer than 62 days between the creditable group plan and the Part D plan.

To help Medicare-eligible plan participants make informed decisions about whether and when to enroll in a Part D drug plan, they need to know if their employer’s group health plan provides creditable or noncreditable prescription drug coverage. That is the purpose of the federal requirement for employers to provide an annual notice (Employer’s Medicare Part D Notice) to all Medicare-eligible employees and spouses.

Employer Requirements

Federal law requires all employers that offer group health coverage including any outpatient prescription drug benefits to provide an annual notice to plan participants.

The notice requirement applies regardless of the employer’s size or whether the group plan is insured or self-funded:

- Determine whether your group health plan’s prescription drug coverage is creditable or noncreditable for the upcoming year (2022). If your plan is insured, the carrier/HMO will confirm creditable or noncreditable status. Keep a copy of the written confirmation for your records. For self-funded plans, the plan actuary will determine the plan’s status using guidance provided by the Centers for Medicare and Medicaid Services (CMS).

- Distribute a Notice of Creditable Coverage or a Notice of Noncreditable Coverage, as applicable, to all group health plan participants who are or may become eligible for Medicare in the next year. “Participants” include covered employees and retirees (and spouses) and COBRA enrollees. Employers often do not know whether a particular participant may be eligible for Medicare due to age or disability. For convenience, many employers decide to distribute their notice to all participants regardless of Medicare status.

- Notices must be distributed at least annually before October 15. Medicare holds its Part D enrollment period each year from October 15 to December 7, which is why it is important for group health plan participants to receive their employer’s notice before October 15.

- Notices also may be required after October 15 for new enrollees and/or if the plan’s creditable versus noncreditable status changes.

Preparing the Notice(s)

Model notices are available on the CMS website. Start with the model notice and then fill in the blanks and variable items as needed for each group health plan. There are two versions: Notice of Creditable Coverage or Notice of Noncreditable Coverage and each is available in English and Spanish:

Employers who offer multiple group health plan options, such as PPOs, HDHPs, and HMOs, may use one notice if all options are creditable (or all are noncreditable). In this case, it is advisable to list the names of the various plan options so it is clear for the reader. Conversely, employers that offer a creditable plan and a noncreditable plan, such as a creditable HMO and a noncreditable HDHP, will need to prepare separate notices for the different plan participants.

Distributing the Notice(s)

You may distribute the notice by first-class mail to the employee’s home or work address. A separate notice for the employee’s spouse or family members is not required unless the employer has information that they live at different addresses.

The notice is intended to be a stand-alone document. It may be distributed at the same time as other plan materials, but it should be a separate document. If the notice is incorporated with other material (such as stapled items or in a booklet format), the notice must appear in 14-point font, be bolded, offset, or boxed, and placed on the first page. Alternatively, in this case, you can put a reference (in 14-point font, either bolded, offset, or boxed) on the first page telling the reader where to find the notice within the material. Here is suggested text from the CMS for the first page:

“If you (and/or your dependents) have Medicare or will become eligible for Medicare in the next 12 months, a federal law gives you more choices about your prescription drug coverage. Please see page XX for more details.”

Email distribution is allowed but only for employees who have regular access to email as an integral part of their job duties. Employees also must have access to a printer, be notified that a hard copy of the notice is available at no cost upon request, and be informed that they are responsible for sharing the notice with any Medicare-eligible family members who are enrolled in the employer’s group plan.

CMS Disclosure Requirement

Separate from the participant notice requirement, employers also must disclose to the CMS whether their group health plan provides creditable or noncreditable coverage. To submit your plan’s disclosure, use the CMS online tool and follow the prompts. The process usually takes only 5 or 10 minutes to complete. It is due with 60 days after the start of the plan year; for instance, for calendar year plans that will be March 1, 2022. If the plan’s prescription drug coverage ends or its status as creditable or noncreditable changes, submit a new disclosure within 30 days of the change.

By Kathleen A. Berger

Originally posted on Mineral