by admin | Feb 12, 2018 | Benefit Management, Compliance, Group Benefit Plans, Medicare

Do you offer health coverage to your employees? Does your group health plan cover outpatient prescription drugs? If so, federal law requires you to complete an online disclosure form every year with information about your plan’s drug coverage. You have 60 days from the start of your health plan year to complete the form. For instance, for a calendar-year health plan, this year’s deadline is March 1, 2018.

Background

The Centers for Medicare and Medicaid Services (CMS) is a federal agency that collects data and administers various federal programs. The agency utilizes the CMS online tool to collect information from employers about whether their group health plan’s prescription drug coverage is creditable or noncreditable. Creditable coverage means the group health plan’s prescription drug coverage is actuarially equivalent to Medicare’s Part D drug plans. In other words, the group plan is considered creditable if its drug benefits are as good as or better than Medicare’s benefits.

To confirm whether your plan provides creditable or noncreditable coverage, check with the plan’s carrier or HMO (if insured) or the plan’s actuary (if self-funded). CMS provides guidance to help plan sponsors, carriers, and actuaries determine the plan’s status.

Deadline for Disclosure

All group health plans that include any outpatient prescription drug benefits, regardless of whether the plan is insured, self-funded, grandfathered, or nongrandfathered, must complete the CMS disclosure requirement. There is no exception for small employers.

Complete the CMS online disclosure form every year within 60 days of the start of the plan year. For instance, for calendar-year plans, this year’s deadline is March 1, 2018.

Additionally, if your plan terminates or its status changes between creditable and noncreditable coverage, you must disclose the updated information to CMS within 30 days of the change.

Completing the Disclosure Form

The CMS online tool is the only method allowed for completing the required disclosure. From this link, follow the prompts to respond to a series of questions regarding the plan. The link is the same regardless of whether the employer’s plan provides creditable or noncreditable coverage.

The entire process usually takes only 5 or 10 minutes to complete. To save time, have the following information handy before you start filling in the form:

- Information about the plan sponsor (employer): Name, address, phone number, and federal Employer Identification Number (EIN).

- Number of prescription drug options offered (e.g., if employer offers two plan options with different benefit levels, the number is “2”).

- Creditable/Noncreditable Offer: Indicate whether all options are creditable or noncreditable or whether some are creditable and others are noncreditable.

- Plan year beginning and ending dates.

- Estimated number of plan participants eligible for Medicare (and how many are participants in the employer’s retiree health plan, if any).

- Date that the plan’s Notice of Creditable (or Noncreditable) Coverage was provided to participants.

- Name, title, and email address of the employer’s authorized individual completing the disclosure.

We suggest you print a copy of the completed disclosure to keep for your records.

Note: Employers that receive the Retiree Drug Subsidy (RDS), or sponsor health plans that contract directly with one or more Medicare Part D plans, should seek the advice of legal counsel regarding the applicable disclosure requirements.

Additional Disclosure Requirement

Separate from the CMS online disclosure requirement, employers also must distribute a disclosure notice to Medicare-eligible group health plan participants. The deadline for distributing the participant notice is October 14 of the preceding year. It often is difficult for employers to identify which employees and spouses may be Medicare-eligible, so most employers simply distribute the notice to all participants regardless of age or status. For information about the notice requirement, see our previous post.

Originally Published By ThinkHR.com

by admin | Feb 6, 2018 | Benefit Management, Employee Benefits, Group Benefit Plans

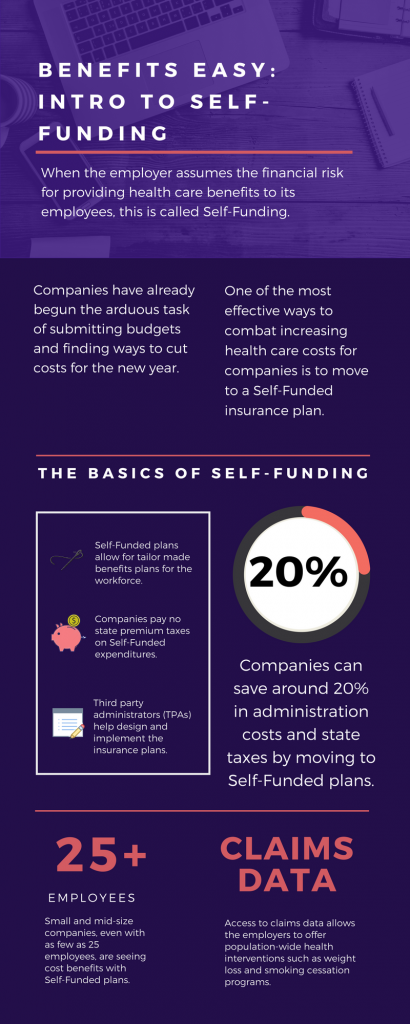

As we head into the second month of 2018, companies have already begun the arduous task of submitting budgets and finding ways to cut costs for the new year. One of the most effective ways to combat increasing health care costs for companies is to move to a Self-Funded insurance plan. By paying for claims out-of-pocket instead of paying a premium to an insurance carrier, companies can save around 20% in administration costs and state taxes. That’s quite a cost savings!

The topic of Self-Funding is huge and so we want to break it down into smaller bites for you to digest. This month we want to tackle a basic introduction to Self-Funding and in the coming months, we will cover the benefits, risks, and the stop-loss associated with this type of plan.

THE BASICS

- When the employer assumes the financial risk for providing health care benefits to its employees, this is called Self-Funding.

- Self-Funded plans allow the employer to tailor the benefits plan design to best suit their employees. Employers can look at the demographics of their workforce and decide which benefits would be most utilized as well as cut benefits that are forecasted to be underutilized.

- While previously most used by large companies, small and mid-sized companies, even with as few as 25 employees, are seeing cost benefits to moving to Self-Funded insurance plans.

- Companies pay no state premium taxes on self-funded expenditures. This savings is around 1.5% – 3/5% depending on in which state the company operates.

- Since employers are paying for claims, they have access to claims data. While keeping within HIPAA privacy guidelines, the employer can identify and reach out to employees with certain at-risk conditions (diabetes, heart disease, stroke) and offer assistance with combating these health concerns. This also allows greater population-wide health intervention like weight loss programs and smoking cessation assistance.

- Companies typically hire third-party administrators (TPA) to help design and administer the insurance plans. This allows greater control of the plan benefits and claims payments for the company.

As you can see, Self-Funding has many facets. It’s important to gather as much information as you can and weigh the benefits and risks of moving from a Fully-Funded plan for your company to a Self-Funded one. Doing your research and making the move to a Self-Funded plan could help you gain greater control over your healthcare costs and allow you to design an original plan that best fits your employees.

by admin | Dec 12, 2017 | ACA, Benefit Management, Compliance, Group Benefit Plans, IRS

Beginning in 2015, to comply with the Patient Protection and Affordable Care Act (ACA), “large” employers must offer their full-time employees health coverage, or pay one of two employer shared responsibility / play-or-pay penalties. The Internal Revenue Service (IRS) determines the penalty each calendar year after employees have filed their federal tax returns.

In November 2017, the IRS indicated on its “Questions and Answers on Employer Shared Responsibility Provisions Under the Affordable Care Act” webpage that, in late 2017, it plans to issue Letter 226J to inform large employers of their potential liability for an employer shared responsibility payment for the 2015 calendar year.

The IRS’ determination of an employer’s liability and potential payment is based on information reported to the IRS on Forms 1094-C and 1095-C and information about the employer’s full-time employees that were received the premium tax credit.

The IRS will issue Letter 226J if it determines that, for at least one month in the year, one or more of a large employer’s full-time employees was enrolled in a qualified health plan for which a premium tax credit was allowed (and the employer did not qualify for an affordability safe harbor or other relief for the employee).

Letter 226J will include:

- A brief explanation of Section 4980H, the employer shared responsibility regulations

- An employer shared responsibility payment summary table that includes a monthly itemization of the proposed payment and whether the liability falls under Section 4980H(a) (the “A” or “No Offer” Penalty) or Section 4980H(b) (the “B” or “Inadequate Coverage” Penalty) or neither section

- A payment summary table explanation

- An employer shared responsibility response form (Form 14764 “ESRP Response”)

- An employee premium tax credit list (Form 14765 “Employee Premium Tax Credit (PTC) List”) which lists, by month, the employer’s assessable full-time employees and the indicator codes, if any, the employer reported on lines 14 and 16 of each assessable full-time employee’s Form 1095-C

- Actions the employer should take if it agrees or disagrees with Letter 226J’s proposed employer shared responsibility payment

- Actions the IRS will take if the employer does not timely respond to Letter 226J

- The date by which the employer should respond to Letter 226J, which will generally be 30 days from the date of the letter

- The name and contact information of the IRS employee to contact with questions about the letter

If an employer responds to Letter 226J, then the IRS will acknowledge the response with Letter 227 to describe further actions that the employer can take.

After receiving Letter 227, if the employer disagrees with the proposed or revised shared employer responsibility payment, the employer may request a pre-assessment conference with the IRS Office of Appeals. The employer must request the conference by the response date listed within Letter 227, which will be generally 30 days from the date of the letter.

If the employer does not respond to either Letter 226J or Letter 227, then the IRS will assess the proposed employer shared responsibility payment amount and issue a notice and demand for payment on Notice CP 220J.

Notice CP 220J will include a summary of the employer shared responsibility payment, payments made, credits applied, and the balance due, if any. If a balance is due, Notice CP 220J will instruct an employer how to make payment. For payment options, such as an installment agreement, employers should refer to Publication 594 “The IRS Collection Process.”

Employers are not required to make payment before receiving a notice and demand for payment.

The ACA prohibits employers from making an adverse employment action against an employee because the employee received a tax credit or subsidy. To avoid allegations of retaliation, as a best practice, employers who receive a Letter 226J should separate their employer shared responsibility penalty assessment correspondence from their human resources department and employees who have authority to make employment actions.

By Danielle Capilla

Originally Published By United Benefit Advisors

by admin | Nov 17, 2017 | Benefit Management, Health Plan Benchmarking, Johnson & Dugan News

We recently unveiled the latest findings from our 2017 Health Plan Survey. With data on 20,099 health plans sponsored by 11,221 employers, the UBA survey is nearly three times larger than the next two of the nation’s largest health plan benchmarking surveys combined. Here are the top trends at a glance.

Cost-shifting, plan changes, and other protections influenced rates

- Sustained prevalence of and enrollment in lower-cost consumer-driven health plans (CDHPs) and health maintenance organization (HMO) plans kept rates lower.

- For yet another year, “grandmothered” employers continue to have the options they need to select cheaper plans (ACA-compliant community-rated plans versus pre-ACA composite/health-rated plans) depending on the health status of their groups.

- Increased out-of-network deductibles and out-of-pocket maximums, with greater increases for single coverage rather than family coverage, as well as prescription drug cost shifting, are among the plan design changes influencing premiums.

- UBA Partners leveraged their bargaining power.

Overall costs continue to vary significantly by industry and geography

- Retail, construction, and hospitality employees cost the least to cover; government employees (the historical cost leader) continue to cost among the most.

- As in 2016, plans in the Northeast cost the most and plans in the Central U.S. cost the least.

- Retail and construction employees contribute above average to their plans, so those employers bear even less of the already low costs in these industries, while government employers pass on the least cost to employees despite having the richest plans.

Plan design changes strained employees financially

- Employee contributions are up, while employer contributions toward total costs remained nearly the same.

- Although copays are holding steady, out-of-network deductibles and out-of-pocket maximums are rising.

- Pharmacy benefits have even more tiers and coinsurance, shifting more prescription drug costs to employees.

PPOs, CDHPs have the biggest impact

- Preferred provider organization (PPO) plans cost more than average, but still dominate the market.

- Consumer-driven health plans (CDHPs) cost less than average and enrollment is increasing.

Wellness programs are on the rise despite increased regulations and scrutiny

Metal levels drive plan decisions

- Most plans are at the gold or platinum metal level reflecting employers’ desire to keep coverage high. In the future, we expect this to change since it will be more difficult to meet the ACA metal level requirements and still keep rates in check.

Key trends to watch

- Slow, but steady: increase in self-funding, particularly for small groups.

- Cautious trend: increased CDHP prevalence/enrollment.

- Rapidly emerging: increase of five-tier and six-tier prescription drug plans.

By Bill Olson

Originally posted by www.UBABenefits.com

by admin | Nov 7, 2017 | Benefit Management, Health Plan Benchmarking

The findings of our 2017 Health Plan Survey show a continuation of steady trends and some surprises. It’s no surprise, however, that costs continue to rise. The average annual health plan cost per employee for all plan types is $9,934, an increase from 2016, when the average cost was $9,727. There are significant cost differences when you look at the data by plan type.

Cost Detail by Plan Type

PPOs continue to cost more than the average plan, but despite this, PPOs still dominate the market in terms of plan distribution and employee enrollment. PPOs have seen an increase in total premiums for single coverage of 4.5% and for family coverage of 2.2% in 2017 alone.

HMOs have the lowest total annual cost at $8,877, as compared to the total cost of a PPO of $10,311. Conversely, CDHP plan costs have risen 2.2% from last year. However, CDHP prevalence and enrollment continues to grow in most regions, indicating interest among both employers and employees.

Across all plan types, employees’ share of total costs rose 5% while employers’ share stayed nearly the same. Employers are also further mitigating their costs by reducing prescription drug coverage, and raising out-of-network deductibles and out-of-pocket maximums.

More than half (54.8%) of all employers offer one health plan to employees, while 28.2% offer two plan options, and 17.1% offer three or more options. The percentage of employers now offering three or more plans decreased slightly in 2017, but still maintains an overall increase in the last five years as employers are working to offer expanded choices to employees either through private exchange solutions or by simply adding high, medium-, and low-cost options; a trend UBA Partners believe will continue. Not only do employees get more options, but employers also can introduce lower-cost plans that may attract enrollment, lower their costs, and meet ACA affordability requirements.

By Bill Olson

Originally Published By United Benefit Advisors

by admin | Oct 26, 2017 | Benefit Management, Benefit Plan Tips, Tricks and Traps, Human Resources

Fall. With it comes cooler temperatures’, falling leaves, warm seasonal scents like turkey and pumpkin pie, and Open Enrollment. It goes without saying; employees who understand the effectiveness of their benefits are much more pleased with those packages, happier with their employers, and more engaged in their work. So, as your company gears up for a new year of navigating Open Enrollment, here are a few points to keep in mind to make the process smoother for both employees and your benefits department. Bonus: it will lighten the load for both parties alike during an already stress-induced season.

Communicate Open Enrollment Using a Variety of Mediums

Advertise 2018 benefit changes to employees by using a variety of mediums. The more reminders and explanation of benefits staff members have using more than one mode of media, the more likely employees will go into Open Enrollment with more knowledge of your company’s benefit options and when they need to have these options completed for the new year.

- Consider explainer videos to simplify the amount of emails and paperwork individuals need to review come Open Enrollment time. These videos can increase the bottom line as well, eliminating the high cost of print material.

- Opt for placards placed throughout your high-traffic areas. Communicate benefit options and remind employees of Open Enrollment dates for the new year by posting in such areas as the lobby, break room and bathroom stalls.

- Choose SMS texting. Today, over 97% of individuals use text. Ninety-eight percent of those that use text open messages within the first three minutes of receiving them; 6-8 times higher than the engagement rate for email. Delivering a concise message to employees’ mobile devices creates more touch points along the Open Enrollment journey. The key, however, is making it quick so as to entice your employees to take action.

- Promote apps and in-app tools. Push notifications and apps like Remind 101 can help drive employee engagement during Open Enrollment season simply by providing short messages reminding them to enroll. Notifications like these can also be tailored to unique employee groups based on location, job level, eligibility status and more.

Utilize Mobile Apps and Web Portals for Open Enrollment

Now that your company has communication down pat for Open Enrollment, simplify the arduous task employees have of enrolling for the coming year by going paperless. Utilize web portals through benefit brokers and companies like ADP to eliminate the hassle of employees having to fill out paperwork both at renewal, and at the time of hire. With nearly three quarters of individuals in the United States checking their phone once an hour and 90% percent of this time is spent using one app or another as a main source of communication, mobile apps can make benefits engagement much easier due to the anywhere/anytime accessibility they offer.

The personal perks for employees are great too! Staff members with a major lifestyle event can make benefit adjustments quickly with the ease of mobile apps. Employees recognize this valuable and time-saving trend and enjoy having this information at their fingertips.

Open Enrollment season can be a stressful time but hopefully these tips will help for a smoother transition into the next year for your business. Simple things like using explainer videos, placing reminders in high traffic areas and utilizing mobile apps and text messaging can save time and stress in the long run for your employees and benefit department.