by admin | Mar 10, 2026 | ACA, Compliance

On January 29, 2026, the U.S. Department of Health and Human Services (HHS) officially released the maximum cost-sharing limits for the 2027 plan year. These figures represent a significant 13.2% increase over the 2026 limits, marking a substantial shift in potential out-of-pocket expenses for plan participants.

2027 Maximum Out-of-Pocket Limits

For 2027, the maximum annual limitation on cost-sharing is:

- Self-Only Coverage: $12,000 (Up from $10,600 in 2026)

- Family Coverage: $24,000 (Up from $21,200 in 2026)

Employers must review their current plan designs to ensure they remain compliant with these updated Affordable Care Act (ACA) mandates.

Understanding the Out-of-Pocket Maximum (OOPM)

The ACA requires most health plans to set an annual cap on total enrollee cost-sharing for Essential Health Benefits (EHBs). This limit is commonly known as the Out-of-Pocket Maximum (OOPM).

Scope of Coverage:

- Applicability: These limits apply to all non-grandfathered health plans, including self-insured, level-funded, and fully insured plans of all sizes.

- Included Costs: Deductibles, copayments, and coinsurance all count toward the limit. Premiums and spending for non-covered services are excluded.

- Essential Health Benefits: Limits apply to the 10 EHB categories, such as emergency services, hospitalization, prescription drugs, and maternity care. Plans are not required to apply the OOPM to non-EHB services.

- Network Status: Plans generally do not have to count out-of-network expenses toward the ACA’s cost-sharing limit.

The “Embedded” Individual Limit

Even within a family plan, the ACA’s self-only cost-sharing limit applies to each individual. This means that if a family plan has a total OOPM higher than the self-only limit ($12,000 for 2027), the plan must include an “embedded” individual OOPM.

Once any single individual in a family reaches the $12,000 threshold, the plan must cover 100% of their qualified expenses for the rest of the year, even if the total family limit has not yet been met.

HSA-Compatible High Deductible Health Plans (HDHPs)

It is important to note that HDHPs compatible with Health Savings Accounts (HSAs) are subject to lower out-of-pocket limits set by the IRS.

While the 2027 HDHP limits have not yet been released, for comparison, the 2026 HDHP limits are capped at $8,500 for self-only and $17,000 for family coverage. Employers with HSA-qualified plans should watch for separate IRS guidance later this year.

Next Steps for Employers:

- Audit 2027 plan designs for compliance with the $12,000/$24,000 thresholds.

- Ensure payroll and benefits systems are updated to handle the embedded individual maximums.

- Consult with your benefits advisor to prepare for the upcoming open enrollment cycle.

by admin | Feb 25, 2026 | ACA

Employers must prepare for Affordable Care Act (ACA) reporting covering the 2025 calendar year. Staying ahead of these deadlines is critical for Applicable Large Employers (ALEs) and providers of self-insured health plans.

Who is Required to Report?

Reporting obligations under Internal Revenue Code Sections 6055 and 6056 fall into two main categories:

Self-Insured Health Plan Providers (Section 6055): Any entity providing minimum essential coverage (MEC), including non-ALEs with self-insured plans.

Applicable Large Employers (ALEs) (Section 6056): Organizations with 50 or more full-time employees (including equivalents).

Note for Self-Insured ALEs: If you are an ALE with a self-funded plan, you must comply with both requirements. However, you can simplify the process by using a single combined filing (Forms 1094-C and 1095-C).

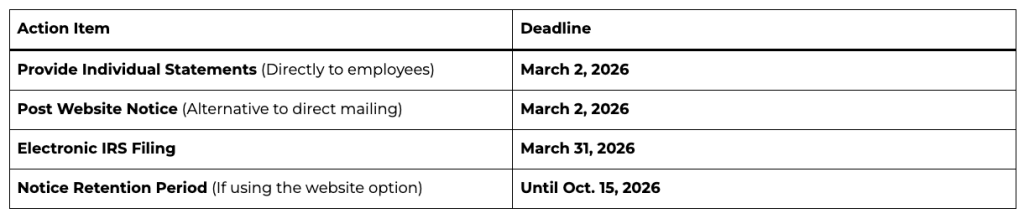

Important Filing Deadlines for 2026

How to Furnish Statements to Individuals

Employers have two options for providing Forms 1095-B or 1095-C to covered individuals:

Direct Delivery: Automatically mail or electronically deliver the forms by March 2, 2026.

Website Notice Alternative: Instead of mailing every form, you may post a “clear, conspicuous, and easily accessible” notice on your website by March 2, 2026.

The notice must state that individuals can request a copy of their form.

It must include an email address, physical address, and phone number for requests.

Requests must be fulfilled within 30 days.

Mandatory Electronic Filing

The IRS now requires electronic filing for almost all employers.

The 10-Return Threshold: If you file 10 or more information returns in total (including W-2s, 1099s, and ACA forms combined), you must file your ACA returns electronically.

The System: Electronic filings must be submitted through the ACA Information Returns (AIR) Program using specific XML formatting.

Extensions and Hardships

Automatic Extension: You can secure an additional 30 days to file with the IRS by submitting Form 8809 by the original March 31 deadline.

Hardship Waivers: While the IRS encourages electronic filing for everyone, waivers may be available for those facing significant technological or financial hardships.

by admin | Sep 2, 2025 | ACA, Compliance, Employee Benefits

How to position yourself as a trusted ACA compliance advisor

For brokers and benefits advisors, Q4 planning doesn’t start in October. It starts now.

September marks a critical moment in the annual ACA compliance cycle, when employers begin thinking about year-end strategies, benefits renewals, and how to avoid last-minute reporting panic. That makes now the perfect time to deepen your role as a strategic advisor and help clients get ahead of the curve.

Here’s how you can stand out by guiding clients through ACA compliance before it becomes a scramble, and why it will pay dividends well into 2026.

📌 Step 1: Help Clients Take Stock of Their Workforce Now

The foundation of ACA compliance is accurate employee classification. Yet many employers still struggle to determine:

Brokers can add immediate value by helping clients audit their headcounts and hours before Q4 begins. That insight informs both ACA reporting and benefits planning decisions, and helps prevent costly missteps when deadlines hit.

🧠 Step 2: Educate on What’s Changed and What’s Coming

ACA rules don’t change often, but confusion persists. Many clients are unaware of:

- State-specific ACA mandates (California, New Jersey, Rhode Island, Vermont, Massachusetts, and Washington DC)

- Updated penalty thresholds and IRS enforcement priorities

- New reporting formats or system changes that could impact submissions

Providing timely updates and checklists positions you not just as a broker but as a compliance partner. You can even use these touchpoints to introduce solutions like ACA reporting automation or integrated compliance tools.

📊 Step 3: Map Out a Reporting Game Plan Before the Crunch

ACA compliance starts with good planning, and now is the time to get ahead. By August, many employers are wrapping up plan design decisions for the next year, making it an ideal time for brokers to:

- Review last year’s filing process (what worked and what didn’t)

- Flag missing or incomplete employee data

- Identify vendors or tools that can simplify electronic filing

- Offer ACA services or connect clients to trusted platforms

The earlier your clients begin organizing data and confirming eligibility, the fewer errors and penalties they’ll face later. And the more indispensable you become in their eyes.

🎯 Position Yourself as the Solution, Not Just the Messenger

ACA compliance is often seen as a burden. But for brokers, it’s a huge opportunity to differentiate. Instead of only alerting clients to upcoming requirements, step in as the solution:

✅ Offer ACA strategy sessions during annual benefits reviews

✅ Share tools and resources that support self-filing or full-service options

✅ Leverage partnerships with platforms like Mitratech Mineral to deliver expert-backed compliance

When you help clients manage risk and reduce workload, you go from being a benefits provider to a business advisor and partner.

🗓 Ready to Dive Deeper?

Join us for a special webinar:

Beyond the Basics: Mastering ACA Compliance for Multi-State Employers

📅 Thursday, September 18, 2025 | 1:00 PM ET

🎙️ Featuring Angela Surra, Principal Benefits Expert at Mitratech Mineral

👉 Register Now

Final Thought

The best brokers know that compliance isn’t a once-a-year conversation, it’s an ongoing strategy. By helping your clients get ACA-ready now, you’re not just solving a problem. You’re showing up as the expert they trust to protect their business, simplify their operations, and keep them ahead of what’s next.

Looking for the right tool to help your clients stay compliant and stress-free? The ACA Reporting Hub from Mitratech Mineral is purpose-built to support brokers and the employers they serve. Whether you’re offering ACA as a service or guiding clients through self-filing, our platform combines automation with compliance expertise to simplify the entire process.

By Brian Costello

Originally posted on Mineral.com

by admin | Jul 28, 2025 | ACA

Big changes are coming to women’s preventive care coverage! Starting with plan years on or after December 31, 2025, group health plans and health insurance issuers must expand their no-cost coverage for women’s preventive care. This expansion includes additional breast cancer imaging or testing needed to complete an initial mammogram, as well as patient navigation services for breast and cervical cancer screenings.

These updates fall under the Affordable Care Act’s (ACA) preventive care mandate, which requires most health plans to cover a range of preventive services without deductibles, copayments, or coinsurance when using in-network providers. The ACA’s guidelines are regularly updated.

The latest HRSA-supported guidelines, updated on December 30, 2024, specifically expand breast cancer screening to include necessary follow-up imaging (such as MRIs or ultrasounds) or pathology evaluations beyond the initial mammogram. Additionally, starting in 2026, patient navigation services for breast and cervical cancer screening and follow-up will be covered. These services offer personalized support, help with healthcare access, referrals to essential services (like language translation or transportation), and patient education.

by admin | Feb 26, 2025 | ACA, Custom Content

At the close of 2024, Congress passed two new pieces of legislation: the Paperwork Burden Reduction Act and the Employer Reporting Improvement Act. These laws simplify the Affordable Care Act (ACA) reporting requirements for employers and introduce new limits on the IRS’s authority to enforce “pay-or-play” penalties, among other changes.

Under the ACA, applicable large employers (ALEs) and non-ALEs with self-insured health plans must report to the IRS regarding the health plan coverage they offer (or don’t offer) to their employees. Additionally, they must provide individual statements about their health plan coverage.

Previously, ALEs were required to send a health coverage statement (Form 1095-C) to each full-time employee within 30 days of January 31 each year. The IRS allowed non-ALEs with self-insured plans to provide health coverage statements (Forms 1095-B) to covered individuals only upon request. Starting in 2025, ALEs will have the same flexibility as non-ALEs to provide Forms 1095-C upon request.

As a result, employers are no longer obligated to send Forms 1095-C or 1095-B to individuals unless specifically requested. Employers must inform individuals about this option in compliance with any IRS guidelines. Requests for forms must be fulfilled by January 31 of the year following the calendar year to which the return pertains, or within 30 days of the request, whichever is later. These forms may be sent electronically to individuals who have previously consented.

Although the new laws offer reporting flexibility, ALEs and non-ALEs with self-insured plans are still required to submit ACA returns to the IRS. The deadline for electronic filing is March 31, 2025.

Additionally, ALEs may face IRS penalties if they fail to offer affordable minimum essential coverage under the ACA’s employer shared responsibility (pay-or-play) rules. The new legislation extends the time ALEs have to respond to IRS penalty assessment warning letters from 30 days to 90 days. It also establishes a six-year limit on the IRS’s ability to collect penalty assessments.

by admin | Feb 6, 2025 | ACA, Compliance

For employers subject to the Affordable Care Act (ACA), staying compliant with reporting requirements is non-negotiable. With 2025 due dates just around the corner, now is the time to prepare for distributing Forms 1095-C to employees and filing with the IRS. These forms provide essential information about health coverage offered to employees and are critical for demonstrating compliance with the ACA’s employer mandate. Missing these deadlines can lead to potential costly penalties and compliance headaches.

Key ACA Reporting Deadlines for 2025

Here are the critical dates you need to mark on your calendar for reporting on the 2024 tax year:

- March 3, 2025:

Deadline for furnishing Form 1095-C to employees.

Employers must provide their employees with a copy of Form 1095-C, which details the health coverage offered, by this date.

- February 28, 2025:

Deadline for paper filing with the IRS.

Employers filing fewer than 10 forms (aggregated with other forms, such as W-2, 1099) may submit paper forms to the IRS. Note: Paper filing is only an option for small employers below the e-filing threshold.

- March 31, 2025:

Deadline for electronic filing with the IRS.

Employers submitting 10 or more forms are required to file electronically. The extra time provided for electronic filing gives employers a little breathing room, but it’s essential to plan ahead and avoid last-minute delays.

Penalties for Missing ACA Reporting Deadlines

Failing to meet ACA reporting deadlines can result in hefty penalties:

- Late Furnishing to Employees:

Employers can be fined up to $310 per form for not providing Form 1095-C to employees by March 3, 2025.

- Late Filing with the IRS:

Penalties start at $60 per form for filing within 30 days of the deadline but can escalate to $310 per form for longer delays.

- Incorrect or Incomplete Information:

Filing forms with incorrect data, such as employee names or Social Security Numbers, can lead to additional penalties.

- Intentional Disregard:

If the IRS determines that an employer intentionally ignored filing requirements, penalties can skyrocket to $630 per form with no annual cap.

Checklist to Stay on Track for ACA Reporting in 2025

Use this checklist to ensure timely and accurate submissions:

- Verify Employee Data:

Review employee names, SSNs, and coverage details for accuracy.

- Select Your Filing Method:

Determine whether you’ll file on paper (if eligible) or electronically. Ensure you have the necessary software for electronic submissions.

- Monitor Deadlines:

Set reminders for March 3(employee furnishing), February 28 (paper filing), and March 31 (electronic filing).

- Test Your Process:

If filing on your own, conduct a test submission through the IRS AIR system to identify potential errors before the official filing.

- Leverage Technology:

Use an ACA compliance software solution to automate form generation, validation, and submission.

- Train Your Team:

Ensure HR, payroll, and benefits teams understand the reporting requirements and deadlines.

- Work with Experts:

Consider outsourcing ACA compliance to a trusted vendor if your internal resources are limited.

Conclusion

ACA reporting doesn’t have to be overwhelming—preparation is key. By understanding the deadlines, filing methods, and potential pitfalls, employers can stay compliant and avoid penalties. With the reporting season fast approaching, now is the time to finalize your plans, gather your data, and ensure you’re ready to meet the 2025 deadlines.

Originally posted on Mineral