by admin | Mar 24, 2026 | Human Resources

As we move through 2026, the workforce is sending a clear message: Stability is the new priority.

New research from the Adecco Group

shows that employees are putting a premium on job security, fair pay, and long-term stability—much more than chasing the next opportunity.

Many have embraced “job hugging”,

choosing to stay where they are rather than jump for a slightly bigger paycheck.

The Great Stability: Why Employees Are Staying Put

Specifically, employees say they stay in their jobs because:

- They’re happy with their work-life balance.

- They like the company culture.

- They’re satisfied with their salary.

- They appreciate the flexibility in their current role.

- They value the upskilling and training they receive.

As the report notes, flexibility, fulfillment, and culture still matter—but they’re no longer enough on their own.

What Employees Value Most Now

Priorities have shifted in the last few years. With the pandemic largely behind us but the economy and society

still unsettled,

employees are sending a clear message.

With the results from the Addeco Group survey, they found that employees value:

-

Prioritize security over personal fulfillment.

Stable income and job security now outrank “purpose” as the top reasons people stay.

In an uncertain world, they need

stability at work.

-

Still want flexibility—but tailored to them.

Leaders often care more about where they work, while junior employees focus on when they work.

One-size-fits-all policies miss the mark.

-

Expect fair and transparent pay.

Blue-collar employees are more likely than white-collar workers to feel they’re paid fairly—but both groups want clarity and openness around compensation.

-

Want to grow where they are.

Many employees want internal mobility, but more than 60% of organizations struggle to move people into new roles.

There’s an opportunity to

build internal mobility

through better

skills gap analysis.

How Companies Can Lead in the Great Stability

Stability alone won’t keep people forever. Employees still need growth, purpose, and a healthy environment as their lives and careers evolve.

Here are four ways organizations can respond:

-

Invest in upskilling and internal mobility.

Many companies have people who could step into new roles, but lack the tools and visibility to make that happen.

At the same time, employees are increasingly taking development into their own hands, learning AI and building new skills on their own.

Companies that provide clear learning paths, targeted training, and internal job opportunities will hold onto their best talent rather than constantly hiring from outside.

-

Create an environment where employees thrive.

Most workers prefer employers committed to inclusion, well-being, sustainability, and purpose—but Adecco found satisfaction with those efforts is still low.

Organizations can stand out by offering real mental health support, visible DEI progress, and meaningful social responsibility,

then communicating those efforts clearly and consistently.

-

Personalize flexibility—think “when and how,” not just “where.”

Instead of generic hybrid or remote policies, give teams tools to shape their own work rhythms:

schedule flexibility, core hours, compressed weeks, or smart shift-swapping for frontline roles.

Let employees help design team norms—like meeting-free blocks and response-time expectations—and tie flexibility to clear performance outcomes.

-

Build a genuine “voice-to-action” loop.

Use short, frequent check-ins and listening sessions focused on what makes people want to stay—workload, manager support, recognition, flexibility, growth.

Then close the loop quickly with “you said, we did” updates so employees see tangible changes within weeks, not months.

The Great Stability isn’t about employees settling; it’s about employers rising to meet a new standard.

Organizations that pair security with fair pay, growth, and real listening will be the ones people choose to “hug” for the long haul.

by admin | Mar 17, 2026 | Uncategorized

If your company provides an employee benefit plan governed by the Employee Retirement Income Security Act (ERISA), you are likely obligated to file Form 5500. This annual report discloses key details about your organization’s benefit offerings, such as welfare benefit plans (including medical, dental, life, and disability coverage), retirement plans, fully insured plans, and self-funded plans. In this article, we break down the fundamentals of Form 5500—who must file, important deadlines, and the consequences of failing to comply.

Who Is Required to File Form 5500?

As a general rule, you must file Form 5500 if your plan had 100 or more participants at the beginning of the plan year. Additionally, any plan that holds its funds in a trust must file, even if it has fewer than 100 participants. However, there are exceptions: welfare plans with fewer than 100 participants that are either unfunded or insured (meaning they don’t hold assets in a trust) are usually exempt. This exemption also covers government entities and church plans. When determining the number of participants for Form 5500, you should count all eligible employees (whether they’ve joined or not), as well as retirees, former employees, and beneficiaries receiving benefits.

Filing Requirement: For non-exempt calendar year plans in 2026, electronic filing of Form 5500 (and attachments) via the DOL’s EFAST2 system is mandatory by July 31, 2026. Need more time? File Form 5558 for a possible extension until October 15, 2026. For more information on filing requirements, penalties and voluntary correction programs, employers can refer to the DOL’s guidance on Form 5500.

Important Note: Small welfare benefit plans (under 100 participants, unfunded or fully insured) might not need to file.

Late Filing? Consider DFVCP: If you’ve missed the deadline for Form 5500, the DOL’s Delinquent Filer Voluntary Compliance Program (DFVCP) could help you avoid bigger penalties by filing voluntarily. To qualify, filings must be completed before the Department of Labor (DOL) sends a written notice of noncompliance.

Penalties for 2026

- The DOL may issue penalties for missing or incomplete filings.

- Under ERISA, penalties can exceed $2,670 per day for each day a complete Form 5500 is not filed.

- Using the DFVCP can help reduce potential penalty amounts.

- Penalties may be waived if there is a reasonable cause for noncompliance.

Form 5500 isn’t just a formality – it’s a vital part of staying compliant and transparent. Understanding your filing responsibilities and planning ahead for audits can save you stress and money.

Quick Links

by admin | Mar 10, 2026 | ACA, Compliance

On January 29, 2026, the U.S. Department of Health and Human Services (HHS) officially released the maximum cost-sharing limits for the 2027 plan year. These figures represent a significant 13.2% increase over the 2026 limits, marking a substantial shift in potential out-of-pocket expenses for plan participants.

2027 Maximum Out-of-Pocket Limits

For 2027, the maximum annual limitation on cost-sharing is:

- Self-Only Coverage: $12,000 (Up from $10,600 in 2026)

- Family Coverage: $24,000 (Up from $21,200 in 2026)

Employers must review their current plan designs to ensure they remain compliant with these updated Affordable Care Act (ACA) mandates.

Understanding the Out-of-Pocket Maximum (OOPM)

The ACA requires most health plans to set an annual cap on total enrollee cost-sharing for Essential Health Benefits (EHBs). This limit is commonly known as the Out-of-Pocket Maximum (OOPM).

Scope of Coverage:

- Applicability: These limits apply to all non-grandfathered health plans, including self-insured, level-funded, and fully insured plans of all sizes.

- Included Costs: Deductibles, copayments, and coinsurance all count toward the limit. Premiums and spending for non-covered services are excluded.

- Essential Health Benefits: Limits apply to the 10 EHB categories, such as emergency services, hospitalization, prescription drugs, and maternity care. Plans are not required to apply the OOPM to non-EHB services.

- Network Status: Plans generally do not have to count out-of-network expenses toward the ACA’s cost-sharing limit.

The “Embedded” Individual Limit

Even within a family plan, the ACA’s self-only cost-sharing limit applies to each individual. This means that if a family plan has a total OOPM higher than the self-only limit ($12,000 for 2027), the plan must include an “embedded” individual OOPM.

Once any single individual in a family reaches the $12,000 threshold, the plan must cover 100% of their qualified expenses for the rest of the year, even if the total family limit has not yet been met.

HSA-Compatible High Deductible Health Plans (HDHPs)

It is important to note that HDHPs compatible with Health Savings Accounts (HSAs) are subject to lower out-of-pocket limits set by the IRS.

While the 2027 HDHP limits have not yet been released, for comparison, the 2026 HDHP limits are capped at $8,500 for self-only and $17,000 for family coverage. Employers with HSA-qualified plans should watch for separate IRS guidance later this year.

Next Steps for Employers:

- Audit 2027 plan designs for compliance with the $12,000/$24,000 thresholds.

- Ensure payroll and benefits systems are updated to handle the embedded individual maximums.

- Consult with your benefits advisor to prepare for the upcoming open enrollment cycle.

by admin | Mar 2, 2026 | Custom Content, Employee Benefits, Health Insurance

Choosing a health insurance plan can feel a lot like solving a puzzle—there are many moving pieces, and the best fit depends on how they come together for your unique situation. With so many options and acronyms—HMO, PPO, POS, EPO, HDHP—it’s easy to feel unsure about where to start. This guide breaks down the most common types of health plans to help you understand how they work, what they cost, and which one might align best with your health care needs and budget.

What Sets Health Plans Apart

When comparing plans, pay attention to these key differences:

- Whether you must choose a Primary Care Provider (PCP)

- If you need referrals to see specialists or get certain services

- Whether the plan requires preauthorization for certain procedures

- If out-of-network care is covered

- How much cost sharing you’re responsible for (deductible, copay, coinsurance)

- Whether you’ll need to file claims or handle additional paperwork

No single plan works for everyone. The right choice depends on your personal health needs, your family’s situation, and your financial comfort level.

Health Maintenance Organization (HMO)

An HMO plan typically offers lower premiums, smaller deductibles, and predictable copays. In exchange, you’ll need to stay within the plan’s provider network and work through a designated PCP, who must refer you to specialists.

HMOs can be a cost-effective option for individuals with fewer health care needs who are comfortable with a structured system.

Preferred Provider Organization (PPO)

PPO plans allow more flexibility when choosing health care providers—you can see specialists and even out-of-network doctors without referrals. These plans usually have higher premiums, and out-of-network care costs more.

A PPO may be a good fit if you want freedom to choose your providers and anticipate needing multiple types of care.

Point-of-Service (POS)

POS plans blend features of both HMOs and PPOs. You’ll select a PCP but can also choose out-of-network care at a higher cost. For slightly higher premiums than an HMO, POS plans provide flexibility while encouraging coordinated care through your PCP.

A POS plan can work well if you want both structure and the occasional freedom to go out-of-network.

Exclusive Provider Organization (EPO)

An EPO plan offers moderate flexibility. Like an HMO, you must use in-network providers, but unlike an HMO, you usually don’t need a referral to see a specialist. Premiums fall between HMO and PPO rates.

An EPO might be right for you if you’re comfortable with a limited provider network and want easier access to specialists.

High Deductible Health Plan (HDHP)

An HDHP can be structured as an HMO, PPO, POS, or EPO. These plans feature lower premiums but higher deductibles—meaning you’ll pay more upfront before coverage kicks in. HDHPs are often paired with a Health Savings Account (HSA), which lets you set aside pre‑tax dollars for medical expenses and roll over unused funds year to year.

HDHPs can work well for those who don’t anticipate frequent medical needs, such as younger or healthier individuals, but they may not be ideal for those with ongoing health concerns.

Final Thoughts

Because health plans and rules can vary by state (and employer), take time to review the details carefully before enrolling. Understanding the coverage, costs, and flexibility of each option will help you make an informed, confident decision that fits your unique health and financial needs.

by admin | Feb 25, 2026 | ACA

Employers must prepare for Affordable Care Act (ACA) reporting covering the 2025 calendar year. Staying ahead of these deadlines is critical for Applicable Large Employers (ALEs) and providers of self-insured health plans.

Who is Required to Report?

Reporting obligations under Internal Revenue Code Sections 6055 and 6056 fall into two main categories:

Self-Insured Health Plan Providers (Section 6055): Any entity providing minimum essential coverage (MEC), including non-ALEs with self-insured plans.

Applicable Large Employers (ALEs) (Section 6056): Organizations with 50 or more full-time employees (including equivalents).

Note for Self-Insured ALEs: If you are an ALE with a self-funded plan, you must comply with both requirements. However, you can simplify the process by using a single combined filing (Forms 1094-C and 1095-C).

Important Filing Deadlines for 2026

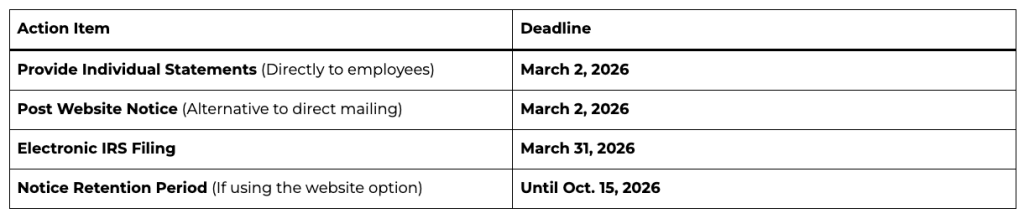

How to Furnish Statements to Individuals

Employers have two options for providing Forms 1095-B or 1095-C to covered individuals:

Direct Delivery: Automatically mail or electronically deliver the forms by March 2, 2026.

Website Notice Alternative: Instead of mailing every form, you may post a “clear, conspicuous, and easily accessible” notice on your website by March 2, 2026.

The notice must state that individuals can request a copy of their form.

It must include an email address, physical address, and phone number for requests.

Requests must be fulfilled within 30 days.

Mandatory Electronic Filing

The IRS now requires electronic filing for almost all employers.

The 10-Return Threshold: If you file 10 or more information returns in total (including W-2s, 1099s, and ACA forms combined), you must file your ACA returns electronically.

The System: Electronic filings must be submitted through the ACA Information Returns (AIR) Program using specific XML formatting.

Extensions and Hardships

Automatic Extension: You can secure an additional 30 days to file with the IRS by submitting Form 8809 by the original March 31 deadline.

Hardship Waivers: While the IRS encourages electronic filing for everyone, waivers may be available for those facing significant technological or financial hardships.