by admin | Feb 6, 2018 | Benefit Management, Employee Benefits, Group Benefit Plans

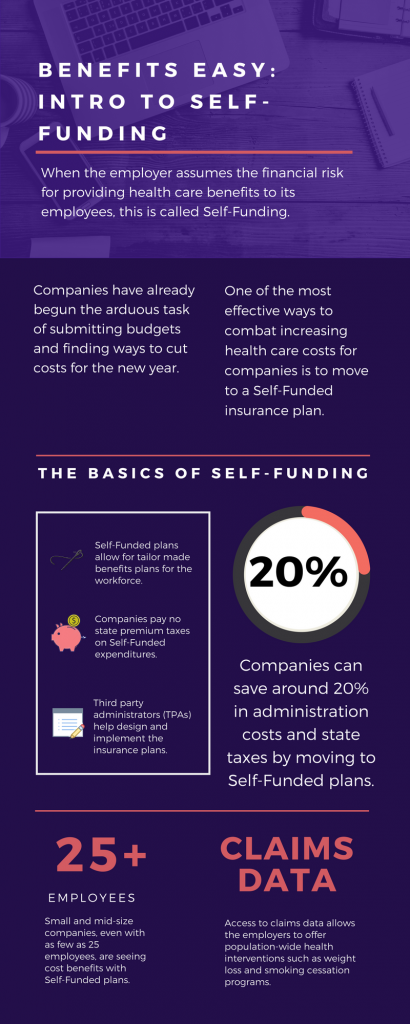

As we head into the second month of 2018, companies have already begun the arduous task of submitting budgets and finding ways to cut costs for the new year. One of the most effective ways to combat increasing health care costs for companies is to move to a Self-Funded insurance plan. By paying for claims out-of-pocket instead of paying a premium to an insurance carrier, companies can save around 20% in administration costs and state taxes. That’s quite a cost savings!

The topic of Self-Funding is huge and so we want to break it down into smaller bites for you to digest. This month we want to tackle a basic introduction to Self-Funding and in the coming months, we will cover the benefits, risks, and the stop-loss associated with this type of plan.

THE BASICS

- When the employer assumes the financial risk for providing health care benefits to its employees, this is called Self-Funding.

- Self-Funded plans allow the employer to tailor the benefits plan design to best suit their employees. Employers can look at the demographics of their workforce and decide which benefits would be most utilized as well as cut benefits that are forecasted to be underutilized.

- While previously most used by large companies, small and mid-sized companies, even with as few as 25 employees, are seeing cost benefits to moving to Self-Funded insurance plans.

- Companies pay no state premium taxes on self-funded expenditures. This savings is around 1.5% – 3/5% depending on in which state the company operates.

- Since employers are paying for claims, they have access to claims data. While keeping within HIPAA privacy guidelines, the employer can identify and reach out to employees with certain at-risk conditions (diabetes, heart disease, stroke) and offer assistance with combating these health concerns. This also allows greater population-wide health intervention like weight loss programs and smoking cessation assistance.

- Companies typically hire third-party administrators (TPA) to help design and administer the insurance plans. This allows greater control of the plan benefits and claims payments for the company.

As you can see, Self-Funding has many facets. It’s important to gather as much information as you can and weigh the benefits and risks of moving from a Fully-Funded plan for your company to a Self-Funded one. Doing your research and making the move to a Self-Funded plan could help you gain greater control over your healthcare costs and allow you to design an original plan that best fits your employees.

by admin | Jan 26, 2018 | Compliance, Human Resources

This is a reminder that from February 1 through April 30, 2018, impacted employers are required to post a copy of their 2017 Form 300A (Summary of Work-Related Illnesses and Injuries) in a common area where employee notices are usually available.

This annual requirement may not apply to certain employers that are partially exempt from routinely keeping Occupational Safety and Health Administration (OSHA) injury and illness reports. Partially exempt employers are those:

Partially exempt employers may have to maintain illness and injury reports at the request of OSHA, the Bureau of Labor Statistics (BLS), or a state agency operating under the authority of OSHA or the BLS. Additionally, pursuant to 29 CFR § 1904.39, all employers, even those that are partially exempt, must report to OSHA any workplace incident that results in a fatality, in-patient hospitalization, amputation, or loss of an eye.

Originally Published By ThinkHR.com

by admin | Jan 19, 2018 | Compliance, Human Resources, IRS

On January 2, 2018, the U.S. Department of Labor (DOL) published updated, inflation-adjusted penalties for violations of various laws regulated by the DOL and its internal components or divisions, including the Occupational Health and Safety Administration (OSHA). The DOL is required to adjust the level of civil monetary penalties for inflation by January 15 each year pursuant to the Federal Civil Penalties Inflation Adjustment Act of 1990, as amended by the Federal Civil Penalties Inflation Adjustment Act Improvements Act of 2015 (Inflation Adjustment Act).

Because of the Inflation Adjustment Act, rates for OSHA penalties have increased three times in the last 17 months (August 1, 2016, January 13, 2017, and January 2, 2018). Therefore, for violations occurring after November 2, 2015, the penalty amounts incurred by employers will depend on when the penalty is assessed, as follows:

- If the penalty was assessed after August 1, 2016 but on or before January 13, 2017, then the August 1, 2016 penalty level applies.

- If the penalty was assessed after January 13, 2017 but on or before January 2, 2018, then the January 13, 2017 penalty level applies.

- If the penalty was assessed after January 2, 2018, then the current penalty level applies.

The applicable January 2, 2018 penalty levels for violations of the Occupational Safety and Health Act of 1970 (OSH Act) are as follows:

- Willful violations: $9,239 – 129,936 (up from $9,054 – $126,749 after January 13, 2017 and $8,908 – $124,709 after August 1, 2016)

- Repeated violations: $129,936 (up from $126,749 after January 13, 2017 and $124,709 after August 1, 2016)

- Serious violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

- Other-than-serious violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

- Failure to correct violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

- Posting requirement violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

These increases apply to states with federal OSHA programs and states with OSHA-approved state plans. Violations occurring on or before November 2, 2015 are assessed at pre-August 1, 2016 levels.

Employers are encouraged to familiarize themselves with these increased penalties and consult counsel if they have questions about the penalty level applicable to a potential violation.

Originally Published By ThinkHR.com

by admin | Jan 17, 2018 | Human Resources, IRS

On January 11, 2018, the Internal Revenue Service released its income tax withholding tables for 2018 reflecting changes made by the December 2017 tax reform legislation. The updated withholding information provides the new rates for employers to use during 2018. Employers are encouraged to use these tables as soon as possible but must use them by no later than February 15, 2018. Employers should continue to use the 2017 withholding tables until they implement the 2018 withholding tables.

According to the U.S. Treasury, an estimated 90 percent of paycheck recipients are likely to see an increase in their take-home pay by February. However, when employees see these changes in their paychecks depends on how quickly the new tables are implemented by their employers and how often they are paid (usually weekly, biweekly, or semimonthly).

To help individuals identify the correct amount of withholding, the IRS is releasing a revised withholding calculator by the end of February, which will be posted on IRS.gov. The IRS encourages taxpayers to use the calculator to adjust their withholding once it is released.

Changes for 2018 and Looking Forward

The new law makes many changes for 2018 that affect individual taxpayers, including an increase in the standard deduction, repeal of personal exemptions, and changes in tax rates and brackets. In relation to Form W-4, these new withholding tables are designed to work with employees’ current W-4, as filed with their employer; so, there are no steps employees must currently take regarding the new tables and law.

The IRS is also working on revising the Form W-4 to reflect the newly available itemized deductions, increases in the child tax credit, the new dependent credit, and repeal of dependent exemptions. However, there is no set release date for the revised form.

Once released, employees may use the new Form W-4 to update their withholding in response to the new law or changes in their personal circumstances in 2018, and by workers starting a new job. Until a new Form W-4 is issued, employees and employers should continue to use the 2017 Form W-4.

For Now

At this time, employers should be reviewing these new tables and implementing necessary changes. For 2019, the IRS has said that it anticipates making even more changes involving withholding. But don’t despair; the agency provides FAQs, which employers and employee may find useful, and pledges to work with the business and payroll community to encourage workers to file new Forms W-4 next year while sharing information on changes in the new tax law that impact withholding.

Stay tuned though, because 2018 has only just begun.

Originally Published By ThinkHR.com

by admin | Jan 5, 2018 | ACA, Compliance, IRS

The ACA requires employers to report the cost of coverage under an employer-sponsored group health plan. Reporting the cost of health care coverage on Form W-2 does not mean that the coverage is taxable.

Employers that provide “applicable employer-sponsored coverage” under a group health plan are subject to the reporting requirement. This includes businesses, tax-exempt organizations, and federal, state and local government entities (except with respect to plans maintained primarily for members of the military and their families). Federally recognized Indian tribal governments are not subject to this requirement.

Employers that are subject to this requirement should report the value of the health care coverage in Box 12 of Form W-2, with Code DD to identify the amount. There is no reporting on Form W-3 of the total of these amounts for all the employer’s employees.

In general, the amount reported should include both the portion paid by the employer and the portion paid by the employee. See the chart below from the IRS’ webpage and its questions and answers for more information.

The chart below illustrates the types of coverage that employers must report on Form W-2. Certain items are listed as “optional” based on transition relief provided by Notice 2012-9 (restating and clarifying Notice 2011-28). Future guidance may revise reporting requirements but will not be applicable until the tax year beginning at least six months after the date of issuance of such guidance.

|

Form W-2, Box 12, Code DD |

| Coverage Type |

Report |

Do Not

Report |

Optional |

| Major medical |

X |

|

|

| Dental or vision plan not integrated into another medical or health plan |

|

|

X |

| Dental or vision plan which gives the choice of declining or electing and paying an additional premium |

|

|

X |

| Health flexible spending arrangement (FSA) funded solely by salary-reduction amounts |

|

X |

|

| Health FSA value for the plan year in excess of employee’s cafeteria plan salary reductions for all qualified benefits |

X |

|

|

| Health reimbursement arrangement (HRA) contributions |

|

|

X |

| Health savings account (HSA) contributions (employer or employee) |

|

X |

|

| Archer Medical Savings Account (Archer MSA) contributions (employer or employee) |

|

X |

|

| Hospital indemnity or specified illness (insured or self-funded), paid on after-tax basis |

|

X |

|

| Hospital indemnity or specified illness (insured or self-funded), paid through salary reduction (pre-tax) or by employer |

X |

|

|

| Employee assistance plan (EAP) providing applicable employer-sponsored healthcare coverage |

Required if employer charges a COBRA premium |

|

Optional if employer does not charge a COBRA premium |

| On-site medical clinics providing applicable employer-sponsored healthcare coverage |

Required if employer charges a COBRA premium |

|

Optional if employer does not charge a COBRA premium |

| Wellness programs providing applicable employer-sponsored healthcare coverage |

Required if employer charges a COBRA premium |

|

Optional if employer does not charge a COBRA premium |

| Multi-employer plans |

|

|

X |

| Domestic partner coverage included in gross income |

X |

|

|

| Governmental plans providing coverage primarily for members of the military and their families |

|

X |

|

| Federally recognized Indian tribal government plans and plans of tribally charted corporations wholly owned by a federally recognized Indian tribal government |

|

X |

|

| Self-funded plans not subject to federal COBRA |

|

|

X |

| Accident or disability income |

|

X |

|

| Long-term care |

|

X |

|

| Liability insurance |

|

X |

|

| Supplemental liability insurance |

|

X |

|

| Workers’ compensation |

|

X |

|

| Automobile medical payment insurance |

|

X |

|

| Credit-only insurance |

|

X |

|

| Excess reimbursement to highly compensated individual, included in gross income |

|

X |

|

| Payment/reimbursement of health insurance premiums for 2% shareholder-employee, included in gross income |

|

X |

|

| Other situations |

Report |

Do Not

Report |

Optional |

| Employers required to file fewer than 250 Forms W-2 for the preceding calendar year (determined without application of any entity aggregation rules for related employers) |

|

|

X |

| Forms W-2 furnished to employees who terminate before the end of a calendar year and request, in writing, a Form W-2 before the end of the year |

|

|

X |

| Forms W-2 provided by third-party sick-pay provider to employees of other employers |

|

|

X |

By Danielle Capilla

Originally Published By United Benefit Advisors