by admin | May 1, 2018 | Benefit Management, Group Benefit Plans, HSA/HRA, IRS

Friday, April 27, the Internal Revenue Service (IRS) announced that the 2018 annual contribution limit to Health Savings Accounts (HSAs) for persons with family coverage under a qualifying High Deductible Health Plan (HDHP) is restored to $6,900. The single-coverage limit of $3,450 is not affected.

This is the final word on what has been an unusual back-and-forth saga. The 2018 family limit of $6,900 had been announced in May 2017. Following passage of the Tax Cuts and Jobs Act in December 2017, however, the IRS was required to modify the methodology used in determining annual inflation-adjusted benefit limits. On March 5, 2018, the IRS announced the 2018 family limit was reduced by $50, retroactively, from $6,900 to $6,850. Since the 2018 tax year was already in progress, this small change was going to require HSA trustees and recordkeepers to implement not-so-small fixes to their systems. The IRS has listened to appeals from the industry, and now is providing relief by reinstating the original 2018 family limit of $6,900.

Employers that offer HSAs to their workers will receive information from their HSA administrator or trustee regarding any updates needed in their payroll files, systems, and employee communications. Note that some administrators had held off making changes after the IRS announcement in March, with the hopes that the IRS would change its position and restore the original limit. So employers will need to consider their specific case with their administrator to determine what steps are needed now.

HSA Summary

An HSA is a tax-exempt savings account employees can use to pay for qualified health expenses. To be eligible to contribute to an HSA, an employee:

- Must be covered by a qualified high deductible health plan (HDHP);

- Must not have any disqualifying health coverage (called “impermissible non-HDHP coverage”);

- Must not be enrolled in Medicare; and

- May not be claimed as a dependent on someone else’s tax return.

HSA 2018 Limits

Limits apply to HSAs based on whether an individual has self-only or family coverage under the qualifying HDHP.

2018 HSA contribution limit:

- Single: $3,450

- Family: $6,900

- Catch-up contributions for those age 55 and older remains at $1,000

2018 HDHP minimum deductible (not applicable to preventive services):

- Single: $1,350

- Family: $2,700

2018 HDHP maximum out-of-pocket limit:

- Single: $6,650

- Family: $13,300*

*If the HDHP is a nongrandfathered plan, a per-person limit of $7,350 also will apply due to the ACA’s cost-sharing provision for essential health benefits.

Originally posted on thinkHR.com

by admin | Mar 14, 2018 | ACA, HSA/HRA, IRS

Taking control of health care expenses is on the top of most people’s to-do list for 2018. The average premium increase for 2018 is 18% for Affordable Care Act (ACA) plans. So, how do you save money on health care when the costs seems to keep increasing faster than wage increases? One way is through medical savings accounts.

Medical savings accounts are used in conjunction with High Deductible Health Plans (HDHP) and allow savers to use their pre-tax dollars to pay for qualified health care expenses. There are three major types of medical savings accounts as defined by the IRS. The Health Savings Account (HSA) is funded through an employer and is usually part of a salary reduction agreement. The employer establishes this account and contributes toward it through payroll deductions. The employee uses the balance to pay for qualified health care costs. Money in HSA is not forfeited at the end of the year if the employee does not use it. The Health Flexible Savings Account (FSA) can be funded by the employer, employee, or any other contributor. These pre-tax dollars are not part of a salary reduction plan and can be used for approved health care expenses. Money in this account can be rolled over by one of two ways: 1) balance used in first 2.5 months of new year or 2) up to $500 rolled over to new year. The third type of savings account is the Health Reimbursement Arrangement (HRA). This account may only be contributed to by the employer and is not included in the employee’s income. The employee then uses these contributions to pay for qualified medical expenses and the unused funds can be rolled over year to year.

There are many benefits to participating in a medical savings account. One major benefit is the control it gives to employee when paying for health care. As we move to a more consumer driven health plan arrangement, the individual can make informed choices on their medical expenses. They can “shop around” to get better pricing on everything from MRIs to prescription drugs. By placing the control of the funds back in the employee’s hands, the employer also sees a cost savings. Reduction in premiums as well as administrative costs are attractive to employers as they look to set up these accounts for their workforce. The ability to set aside funds pre-tax is advantageous to the savings savvy individual. The interest earned on these accounts is also tax-free.

The federal government made adjustments to contribution limits for medical savings accounts for 2018. For an individual purchasing single medical coverage, the yearly limit increased $50 from 2017 to a new total $3450. Family contribution limits also increased to $6850 for this year. Those over the age of 55 with single medical plans are now allowed to contribute $4450 and for families with the insurance provider over 55 the new limit is $7900.

Health care consumers can find ways to save money even as the cost of medical care increases. Contributing to health savings accounts benefits both the employee as well as the employer with cost savings on premiums and better informed choices on where to spend those medical dollars. The savings gained on these accounts even end up rewarding the consumer for making healthier lifestyle choices with lower out-of-pocket expenses for medical care. That’s a win-win for the healthy consumer!

by admin | Mar 9, 2018 | HSA/HRA, IRS

On March 5, 2018, the Internal Revenue Service (IRS) announced a reduction in the maximum annual contribution allowed for Health Savings Accounts (HSAs) in 2018. The change does not affect people whose HSA contributions are based on self-only health coverage, but it does affect those with family coverage under a qualifying High Deductible Health Plan (HDHP). Previously, the 2018 HSA contribution limit for persons with family HDHP coverage was $6,900. That limit is now reduced retroactively to $6,850.

In Revenue Bulletin 2018-10, the IRS explains that the recently-enacted tax reform law requires recalculating inflation-adjusted amounts under various tax code provisions. One of the affected provisions is § 223 pertaining to HSAs. Using the new required method of applying annual inflation adjustments, the 2018 HSA contribution limit for those with family HDHP coverage is $6,850, which is a $50 reduction from the amount previously announced.

HSA Summary

An HSA is a tax-exempt savings account employees can use to pay for qualified health expenses. To be eligible to contribute to an HSA, an employee:

- Must be covered by a qualified high deductible health plan (HDHP);

- Must not have any disqualifying health coverage (called “impermissible non-HDHP coverage”);

- Must not be enrolled in Medicare; and

- May not be claimed as a dependent on someone else’s tax return.

HSA 2018 Limits

Limits apply to HSAs based on whether an individual has self-only or family coverage under the qualifying HDHP.

2018 HSA contribution limit:

- Single: $3,450

- Family: $6,850

- Catch-up contributions for those age 55 and older remains at $1,000

2018 HDHP minimum deductible (not applicable to preventive services):

- Single: $1,350

- Family: $2,700

2018 HDHP maximum out-of-pocket limit:

- Single: $6,650

- Family: $13,300*

*If the HDHP is a nongrandfathered plan, a per-person limit of $7,350 also will apply due to the ACA’s cost-sharing provision for essential health benefits.

Originally Published By ThinkHR.com

by admin | Aug 4, 2017 | HSA/HRA

Across most industries, HSA contributions are, for the most part, down or unchanged from three years ago, according to UBA’s Health Plan Survey. The average employer contribution to an HSA is $474 for a single employee (down 3.5 percent from 2015 and 17.6 percent from five years ago) and $801 for a family (down 9.2 percent from last year and 13.7 percent from five years ago). Government and education employers are the only industries with average single contributions well above average and on the rise.

Government employees had the most generous contributions for singles at $850, on average, up from $834 in 2015. This industry also has the highest employer contributions for families, on average, at $1,595 (though that is down from 1,636 in 2015). Educational employers are the next most generous, contributing $636, on average, for singles and $1,131 for families.

Singles in the accommodation/food services industries received virtually no support from employers, with average HSA contributions at $166. The same is true for families with HSA plans in the accommodation/food services industries with average family contributions of $174.

Retail employers also remain among the least generous contributors to single and family HSA plans, contributing $305 and $470, respectively. This may be why they have low enrollment in these plans.

The education services industry has seen a 109 percent increase in HSA enrollment since 2013 (aided by employers’ generous contributions), catapulting the industry to the lead in HSA enrollment at 23.8 percent. The professional/scientific/tech and finance/insurance industries follow closely at 23.3 percent and 22.1 percent, respectively.

The mining/oil/gas industry sees the lowest enrollment at 3.8 percent. The retail, hotel, and food industries continue to have some of the lowest enrollment rates despite the prevalence of these plans, indicating that these industries, in particular, may want to increase employee education efforts about these plans and how they work.

For a detailed look at the prevalence and enrollment rates among HSA and HRA plans by group size and region, view UBA’s “Special Report: How Health Savings Accounts Measure Up”.

Benchmarking your health plan with peers of a similar size, industry or geography makes a big difference in determining if your plan is competitive. To compare your exact plan with your peers, request a custom benchmarking report.

For fast facts about HSA and HRA plans, including the best and worst plans, average contributions made by employers, and industry trends, download (no form!) “Fast Facts: HSAs vs. HRAs”.

By Bill Olson

Originally Posted By www.ubabenefits.com

by admin | Jun 16, 2017 | HSA/HRA

The average employer contribution to an HSA is $474 for a single employee (down 3.5 percent from 2015 and 17.6 percent from five years ago) and $801 for a family (down 9.2 percent from last year and 13.7 percent from five years ago). There was a 26 percent increase in the number of individuals enrolled in HSAs, likely due to the increase in CDHP enrollment (which often have HSAs tied to them). Since 2013, there has been a 97.7 percent increase in enrollment, showing significant employer and employee interest in these plans over time.

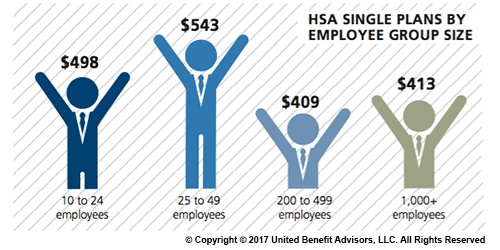

Looking at contributions by group size, singles at companies with 200 to 499 employees receive the lowest HSA contributions ($409). Singles at some of the smallest companies (25 to 49 employees) receive the most generous contributions ($543), on average.

Like their single counterparts, families get more generous contributions from small employers. The average family HSA contribution in groups with 25 to 49 employees was $908 (though, in general, small employer contributions have been declining over time).

Last year, some of the smallest companies (10 to 24 employees) had the highest HSA enrollment (16.3 percent). However, rapid enrollment increases among large employers in recent years now places the largest companies (1,000+ employees) as HSA enrollment leaders with 19.1 percent enrolled.

For a detailed look at the prevalence and enrollment rates among HSA and HRA plans by industry and region, view UBA’s “Special Report: How Health Savings Accounts Measure Up”, to understand which aspects of these accounts are most successful, and least successful.

Benchmarking your health plan with peers of a similar size, industry and/or geography makes a big difference in determining if your plan is competitive. To compare your exact plan with your peers, request a custom benchmarking report.

For fast facts about HSA and HRA plans, including the best and worst plans, average contributions made by employers, and industry trends, download (no form!) “Fast Facts: HSAs vs. HRAs”.

By Bill Olson

Originally Posted By www.ubabenefits.com

by admin | Jun 9, 2017 | HSA/HRA, IRS

IRS Releases 2018 Amounts for HSAs

The IRS released Revenue Procedure 2017-37 that sets the dollar limits for health savings accounts (HSAs) and high-deductible health plans (HDHPs) for 2018.

For calendar year 2018, the annual contribution limit for an individual with self-only coverage under an HDHP is $3,450, and the annual contribution limit for an individual with family coverage under an HDHP is $6,900. How much should an employer contribute to an HSA? Read our latest news release for information on modest contribution strategies that are still driving enrollment in HSA and HRA plans.

For calendar year 2018, a “high deductible health plan” is defined as a health plan with an annual deductible that is not less than $1,350 for self-only coverage or $2,700 for family coverage, and the annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) do not exceed $6,650 for self-only coverage or $13,300 for family coverage.

Retroactive Medicare Coverage Effect on HSA Contributions

The Internal Revenue Service (IRS) recently released a letter regarding retroactive Medicare coverage and health savings account (HSA) contributions.

As background, Medicare Part A coverage begins the month an individual turns age 65, provided the individual files an application for Medicare Part A (or for Social Security or Railroad Retirement Board benefits) within six months of the month in which the individual turns age 65. If the individual files an application more than six months after turning age 65, Medicare Part A coverage will be retroactive for six months.

Individuals who delayed applying for Medicare and were later covered by Medicare retroactively to the month they turned 65 (or six months, if later) cannot make contributions to the HSA for the period of retroactive coverage. There are no exceptions to this rule.

However, if they contributed to an HSA during the months that were retroactively covered by Medicare and, as a result, had contributions in excess of the annual limitation, they may withdraw the excess contributions (and any net income attributable to the excess contribution) from the HSA.

They can make the withdrawal without penalty if they do so by the due date for the return (with extensions). Further, an individual generally may withdraw amounts from an HSA after reaching Medicare eligibility age without penalty. (However, the individual must include both types of withdrawals in income for federal tax purposes to the extent the amounts were previously excluded from taxable income.)

If an excess contribution is not withdrawn by the due date of the federal tax return for the taxable year, it is subject to an excise tax under the Internal Revenue Code. This tax is intended to recapture the benefits of any tax-free earning on the excess contribution.

By Danielle Capilla

Originally Posted By www.ubabenefits.com