by admin | Oct 29, 2024 | ACA, Compliance

The Department of Health and Human Services (HHS) has issued a final rule that significantly expands the Mental Health Parity and Addiction Act (MHPAEA) requirements under the Affordable Care Act (ACA). This rule aims to ensure that health plans provide equal coverage for mental health and substance use disorder (MH/SUD) benefits as they do for medical benefits.

Key Changes in the Final Rule:

Expanded Parity Definition: The rule expands the definition of mental health conditions to include substance use disorders and conditions associated with autism spectrum disorder.

Expanded Treatment Limitations: The rule prohibits health plans from imposing stricter limitations on mental health benefits than those applied to medical benefits. This includes limitations on the number of visits, days of service, or types of treatments.

Enhanced Enforcement: The rule strengthens enforcement mechanisms to ensure compliance with mental health parity requirements.

Implications for Health Plans and Employers

Compliance Review: Health plans will need to review their benefit plans to ensure they comply with the expanded parity requirements.

Benefit Design Changes: Some plans may need to be modified to eliminate discriminatory treatment of mental health benefits.

Increased Costs: The expanded parity requirements may lead to increased costs for health plans.

Improved Access to Care: The rule is expected to improve access to mental health and substance use disorder treatment for individuals with health insurance coverage.

Next Steps for Employers and Employees

Review Your Plan: Employers should review their health plans to ensure compliance with the expanded parity requirements.

Understand Your Benefits: Employees should become familiar with their mental health benefits and how they are covered under their plan.

Seek Assistance: If you have questions or concerns about your mental health benefits, contact your health plan or your employer’s human resources department.

The final rule represents a significant step forward in ensuring that individuals with mental health and substance use disorders have access to the same level of care as those with medical conditions. By understanding the expanded parity requirements, employers and employees can work together to improve access to mental health treatment and promote overall well-being.

by admin | Oct 7, 2024 | ACA, Compliance

by admin | Sep 9, 2024 | ACA, Compliance

The Affordable Care Act (ACA) introduced the Medical Loss Ratio (MLR) to ensure that health insurance companies spend a significant portion of premiums on medical care and quality improvement activities rather than administrative costs and profits. When insurers fail to meet the MLR threshold, they are required to issue rebates to plan sponsors.

Understanding MLR Rebates

The MLR mandates that health insurers spend at least a certain percentage of premium dollars on medical claims and quality improvement activities. This percentage varies depending on the type of plan. If an insurer’s medical loss ratio falls below the required threshold, they must issue a rebate to the plan sponsor, typically the employer.

Approaching Deadlines: Time to Prepare

It’s essential for employers to be aware of the MLR rebate deadlines. These deadlines vary by year, but typically, insurers have until September 30th of the following year to issue rebates for the previous year’s plan performance. For instance, rebates for 2023 plan performance are due by September 30, 2024.

What to Do with Your MLR Rebate

Employers who receive MLR rebates should carefully consider how to use the funds. While the specific use of the funds depends on the plan’s legal structure and governing documents, some common options include:

- Offsetting future premium costs: Using the rebate to reduce future premium payments.

- Funding wellness programs: Investing in employee wellness initiatives to improve overall health and productivity.

- Contributing to a health savings account (HSA): Offering additional contributions to employee HSAs to help cover healthcare costs.

- Other plan improvements: Using the rebate to enhance other plan benefits or expand coverage options.

Important Considerations:

- ERISA Compliance: If the rebate qualifies as a plan asset under ERISA, it must be used solely for the benefit of plan participants and beneficiaries.

- Documentation: Maintain proper documentation of how the rebate is used to comply with regulatory requirements.

By understanding the MLR rebate process and carefully considering how to use the funds, employers can maximize the benefits of this unexpected windfall and improve the overall health and well-being of their workforce.

by admin | Jul 9, 2024 | ACA, Compliance

The Patient-Centered Outcomes Research Trust Fund fee, often referred to as the PCORI fee, can be a source of confusion for employers offering health insurance plans. This article aims to simplify what the PCORI fee is, why it exists, and how it impacts your business.

What is the PCORI Fee?

The PCORI fee is an annual charge levied on most health insurance plans and self-funded employer health plans. It was established by the Affordable Care Act (ACA) to fund the Patient-Centered Outcomes Research Institute (PCORI).

What Does PCORI Do?

PCORI is an independent, non-profit organization dedicated to conducting research on the effectiveness of different medical treatments and approaches. Their research helps patients, caregivers, and healthcare providers make more informed decisions about treatment options.

The IRS offers useful resources, including a chart that explains how the fees apply to different types of health coverage and arrangements.

How Much is the PCORI Fee?

The PCORI fee is calculated based on the average number of lives covered under a plan during the policy year. The fee amount is adjusted annually based on inflation in National Health Expenditures. Here’s a quick breakdown:

- For plans ending after September 30, 2023 and before October 1, 2024: The applicable dollar amount is $3.22 per covered life.

- For plans ending after September 30, 2022 and before October 1, 2023: The applicable dollar amount is $3.00 per covered life.

Who Pays the PCORI Fee?

The PCORI fee is generally paid by the issuer of a health insurance plan or the plan sponsor of a self-funded health plan. Employers offering group health plans will typically see the PCORI fee reflected in their health insurance premium statements.

When is the PCORI Fee Due?

The PCORI fee is typically due on July 31st of the year following the last day of the plan year.

Are There Any Exemptions?

Certain types of health plans are exempt from the PCORI fee, including:

- Health Reimbursement Arrangements (HRAs)

- Certain government-funded plans (Medicare, Medicaid)

- Some limited-flexibility plans

The Bottom Line:

The PCORI fee is a relatively small annual cost that helps fund valuable research in patient-centered outcomes. Understanding the purpose and calculation of the PCORI fee can help employers better manage their health insurance expenses and contribute to the advancement of healthcare knowledge.

Additional Resources:

by admin | Nov 17, 2021 | ACA

On September 30, 2021, the Department of Health and Human Services, the Department of Labor, and the Department of the Treasury (collectively, the Departments), along with the Office of Personnel Management (OPM), released an interim final rule (IFR) under the No Surprises Act (Act) to help protect health care consumers from surprise billing and excessive cost sharing. The IFR primarily explains the Act’s mandatory independent dispute resolution (IDR) process.

Background

A prior interim final rule established that, for emergency services and certain non-emergency services furnished by out-of-network (OON) providers at in-network facilities, patients will pay a cost-sharing rate similar to the in-network rate, which must be calculated based on a state All-Payer Model Agreement, specific state law, or, if neither apply, the qualifying payment amount (QPA). The QPA is generally the plan or carrier’s median contracted rate for the same or similar service in the specific geographic area.

The Act provides that the balance of the bill to be paid by the plan or carrier following patient cost sharing and any initial payment from the plan or carrier is determined between the provider (including air ambulance provider), facility, and the plan or carrier through an open negotiation period. If the parties cannot agree on a payment amount, the Act mandates a federal IDR process.

The IDR process applies only to:

- Balance billing for emergency services; cost-sharing for emergency services must be determined on an in-network basis.

- Patient copayments, co-insurance, or deductibles for emergency services and certain non-emergency services provided at an in-network facility; cannot be higher than if such services were provided by an in-network provider, and any cost-sharing obligation must be based on in-network provider rates.

- OON charges for items or services provided by an OON provider at an in-network facility; prohibited unless notice and consent given in advance. Providers and facilities must provide patients with a plain-language consumer notice explaining that patient consent is required to receive care on an OON basis before that provider can bill the patient more than in-network cost-sharing rates.

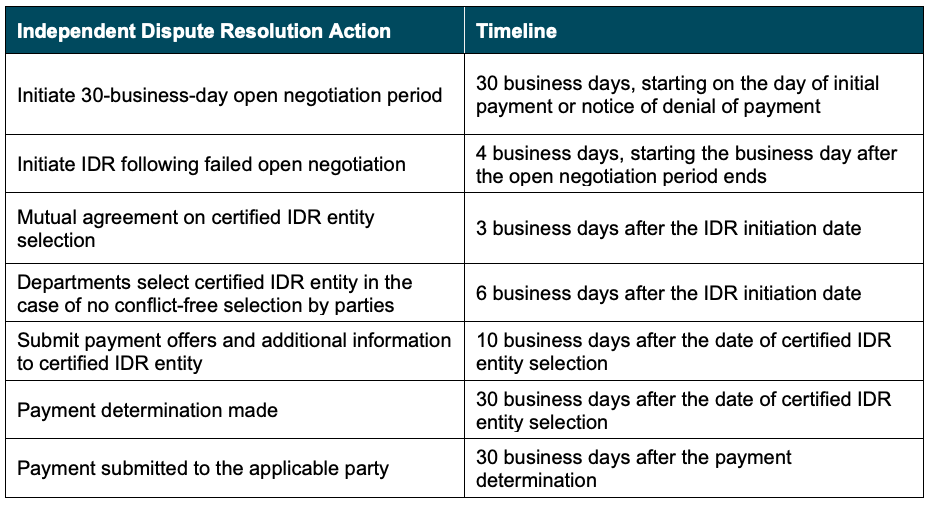

Independent Dispute Resolution

Before initiating the IDR process, disputing parties must initiate a 30-day open negotiation period. If open negotiation fails, either party may start the IDR process. If the parties cannot agree on a jointly selected certified IDR entity, or if the jointly selected certified IDR entity has a conflict of interest, the Departments will select a certified IDR entity. The parties will submit their payment offers along with supporting documentation, and the certified IDR entity will issue a binding determination by selecting one party’s offer.

When making a payment determination, certified IDR entities must assume that the QPA is the appropriate OON amount. The certified IDR entity must consider any credible permissible information submitted by a party. For the IDR entity to deviate from the offer closest to the QPA, however, any information submitted must clearly demonstrate that the value of the item or service is materially different from the QPA.

The IDR process will proceed according to the following guidelines:

Expanded External Review

Additionally, the IFR expands the scope of adverse benefit determinations eligible for external review to include determinations that involve whether a plan or issuer is complying with the surprise billing and cost-sharing protections under the No Surprises Act and its implementing regulations. In addition, under these interim final rules, grandfathered plans that are not otherwise subject to external review requirements will be subject to external review requirements for coverage decisions that involve whether a plan or issuer is complying with the surprise billing and cost-sharing protections under the No Surprises Act.

Conclusion

The regulations in the IFR become applicable to group health plans for plan and policy years beginning on or after January 1, 2022. However, the IFR is subject to a public comment period that will close in December 2021. We will continue to monitor this and other related developments under the No Surprises Act and provide ongoing updates as needed.

©2021 United Benefit Advisors, LLC. All rights reserved.

by admin | Oct 28, 2021 | ACA

The Affordable Care Act’s employer shared responsibility provision — often called the employer mandate or “play or pay” — requires large employers to offer health coverage to their full-time employees or face a potential penalty. (Employers with fewer than 50 full-time and full-time-equivalent employees are exempt.) Large employers can avoid the risk of any play or pay penalties by offering all full-time employees at least one group health plan option that meets two standards: It provides minimum value and it is affordable.

Minimum value means the plan’s share of total allowed costs is at least 60 percent and the plan provides substantial coverage of physician services and inpatient hospital services.

Affordable means the employee’s required contribution (payroll deduction) for self-only coverage, if elected, does not exceed a certain percentage of the employee’s household income. The affordability percentage changes slightly each year based on the law’s indexing rule. For 2021, the percentage is 9.83 percent. For 2022, however, the percentage decreases to 9.61 percent.

Although the change is minor, it means that employers need to consider whether their plan’s employee-only contribution rate will still meet the affordability standard next year.

Determining Affordability

The first step in determining whether a group health plan option is affordable is to define the employee’s “income.” Employers do not know their workers’ total household income, so the play or pay rules offer employers three optional safe harbor methods to define income using information known to the employer. Employers may use any of the safe harbor methods. They also may use different methods for different classes (such as one method for hourly employees and another method for salaried employees), provided that the chosen method is applied uniformly to all employees in the class.

The three IRS safe harbor methods are:

- Federal Poverty Line (FPL)

The FPL method is the easiest of the three methods. Multiply the mainland FPL amount for a single-member household by the affordability percentage, then divide by 12. As long as the self-only contribution rate does not exceed the resulting amount, the plan’s coverage is deemed affordable. For instance:

- 2021: ($12,760 x 9.83%)/12 = $104.52 per month

- 2022 ($12,880 x 9.61%)/12 = $103.15 per month

The FPL chart is updated every year in late January. For 2022 calendar-year health plans, the employer needs to refer to the current FPL amount ($12,880) since the new FPL amount will not be available until after the plan year starts. If the health plan year starts February 1, 2022 or later, however, the employer may refer to the new FPL amount which likely will be a little higher.

2. Rate of Pay

This is the most convenient method to define income when applied to hourly employees. Multiply the employee’s hourly rate of pay times 130 hours per month (regardless of how many hours he or she actually works), then multiply by the affordability percentage. As long as the self-only contribution rate does not exceed the resulting amount, the plan’s coverage is deemed affordable. For instance:

- 2021: ($11* x 130) x 9.83% = $140.57 per month

- 2022: ($11* x 130) x 9.61% = $137.42 per month

* Replace $11 with the hourly employee’s rate of pay.

For salaried employees, the rate of pay method is somewhat complicated so employers generally avoid using this method for non-hourly employees.

3. W-2

The W-2 method requires using current W-2 wages instead of looking back at the prior year. W-2 wages means the amount that will be reported in Box 1 of Form W-2. Pretax contributions, such as § 125 plan contributions and 401(k) or 403(b) plan deferrals, are not included in Box 1, so using the W-2 safe harbor method may understate the employee’s actual income. Coverage will be deemed affordable if, for each month of the plan year, the self-only contribution does not exceed the Box 1 amount multiplied by the affordability percentage.

Summary

Large employers can avoid the risk of potential penalties under the ACA’s play or pay rules by ensuring that they offer full-time employees at least one minimum value plan option that also is affordable. Affordable means the employee’s contribution to elect self-only coverage would not exceed a certain percentage of the employee’s income.

The percentage used to determine affordability changes from year to year is based on the law’s indexing formula. For 2021 plan years, the affordability percentage is 9.83 percent, but it decreases to 9.61 percent for 2022 plan years. Employers and their advisors will want to keep this information in mind as they finalize their group health plan offerings and employee contribution rates for 2022.

By Kathleen A. Berger, CEBS

Originally posted on Mineral