by admin | Dec 10, 2025 | Compliance, HIPAA

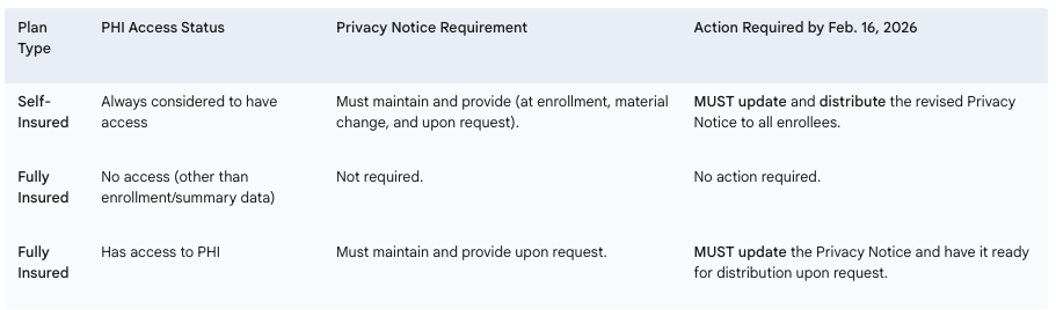

The U.S. Department of Health and Human Services (HHS) has issued a final rule that requires covered entities—including many health plans—to update their Notice of Privacy Practices (Privacy Notice). This change enhances privacy protections for highly sensitive Substance Use Disorder (SUD) treatment records.

Why the Update is Necessary

The HIPAA Privacy Rule already mandates that covered entities provide a Privacy Notice to explain how an individual’s Protected Health Information (PHI) is used.

However, the April 2024 final rule specifically addresses patient records involving SUD treatment from federally assisted programs (often referred to as “Part 2 programs”). Any covered entity that receives or maintains these Part 2 records must now update their Privacy Notice to reflect these additional, heightened protections.

The mandatory deadline for updating and distributing these notices is February 16, 2026.

Required Employer Actions by Plan Type

Employers sponsoring health plans must determine their level of responsibility based on their plan’s funding structure and access to PHI.

Next Steps for Employers: Employers with self-insured health plans, or fully insured plans that manage PHI, must immediately begin the process of updating their Privacy Notices to incorporate the new requirements for SUD treatment records. It is currently uncertain if HHS will release updated model privacy notices before the deadline.

by admin | Dec 9, 2025 | Custom Content, Health & Wellness

The transition into winter and the busy holiday season often brings two things: cold weather and packed calendars. While the shorter days and festive cheer are welcome, they also present unique challenges to our health, including managing stress, fighting off seasonal illnesses, and maintaining an active routine.

Staying healthy this winter isn’t about grand gestures; it’s about small, consistent habits that protect your body and mind. Here is your guide to winter wellness.

- Boost Your Immune System and Sleep

The fight against winter colds and the flu starts with strengthening your natural defenses. This season, prioritize three foundational pillars of immunity:

Mind Your Vitamin D

With less sunlight exposure, many people become deficient in Vitamin D, which is crucial for immune function and mood regulation. If you can’t get 10–15 minutes of midday sun exposure, consider speaking to your doctor about a supplement. This small adjustment can make a big difference in fighting off sickness.

Stay Hydrated (Yes, Even in Winter)

The dry winter air and indoor heating dehydrate us faster than we realize, weakening the protective mucous membranes that fight germs. Keep a water bottle within reach and aim to drink herbal tea or warm water throughout the day. Dehydration contributes to fatigue, which makes you more susceptible to illness.

Make Sleep Non-Negotiable

Sleep is your body’s most effective time for immune repair. With holiday parties and deadlines looming, it’s easy to sacrifice an hour of sleep, but this can significantly compromise your health. Aim for 7-9 hours of quality sleep nightly. Stick to a consistent bedtime, even on weekends, to regulate your body’s natural rhythms.

- Managing Holiday Stress and Mental Load

The holidays bring a mix of joy and unique pressures—financial strain, travel headaches, and social commitments. Protect your mental health by applying these strategies:

Practice Proactive Planning

Instead of letting tasks pile up, dedicate 15 minutes each Sunday evening to look at your calendar and budget your energy. Schedule time blocks not just for work meetings, but also for “recharge time” and “boundary setting.”

Set Realistic Boundaries

It’s okay to say no to extra commitments. Whether it’s an optional holiday event or taking on another project before year-end, know your limits. Communicate clearly and politely: “That sounds lovely, but I can’t commit right now.” Protecting your time is vital for preventing burnout.

Embrace Micro-Mindfulness

Use small moments throughout the workday to check in with yourself. Before answering an email or joining a meeting, take two deep, slow breaths. This simple action can lower your heart rate, reduce the stress hormone cortisol, and reset your focus.

- Keep Moving, Inside and Out

When it’s cold and dark, the couch can be a powerful magnet. Counter this by adapting your fitness routine to the season:

Take a “Walking Meeting”

If you are working from home or have an internal call, suggest a walking meeting outside. Even 15 minutes of brisk outdoor walking can boost your mood and provide light exposure to aid Vitamin D production. Remember to layer up!

Find Your Indoor Outlet

Don’t rely solely on outdoor activities. Explore simple indoor options: use resistance bands while watching TV, follow a 15-minute yoga session online, or simply do some stretching and bodyweight exercises before starting your workday. The goal is consistency, not intensity.

Fuel with Focus

The holidays often mean sugary treats, which can lead to energy crashes and sluggishness. Balance celebratory foods with nutrient-dense options. Focus on protein, fiber, and healthy fats to keep your energy stable, especially during peak work hours.

By taking small steps each day – and listening to your body – you can enjoy the winter season, stay healthy, and start the new year feeling your best.

by admin | Dec 2, 2025 | Compliance, ERISA

Employers with insured health plans may have received a Medical Loss Ratio (MLR) rebate from their health insurance carrier this year. Rebates were required for plans not meeting the 2024 MLR standards and had to be issued by September 30, 2025, either as premium credits or lump-sum payments.

If any part of the rebate qualifies as a plan asset under ERISA, it must benefit plan participants and beneficiaries exclusively. Employers can fulfill this requirement by distributing the plan asset portion using a fair and reasonable allocation method. Alternatively, if direct payments aren’t practical, the rebate can be used for other allowable plan purposes, such as future premium reductions or benefit enhancements.

ERISA generally requires that plan assets be kept in trust, but this is waived if any rebate amount considered a plan asset is used within three months of receipt, so employers must pay careful attention to the timeline. For example, rebates received on September 30, 2025, must be used by December 30, 2025.

Key points:

- Under the Affordable Care Act, health insurers must spend a minimum percentage of premiums on medical care and quality improvements; if not, rebates are required.

- Employers must determine if any rebate portion qualifies as a plan asset under ERISA.

- Plan assets must only benefit plan participants and beneficiaries and generally must be used within three months of receiving the rebate to remain ERISA-compliant.

Employers should review current obligations to ensure any rebate qualifying as a plan asset is properly allocated and used in accordance with federal requirements.

by admin | Nov 24, 2025 | Custom Content, Health & Wellness

The phrase “attitude of gratitude” is more than a simple rhyme—it’s a powerful reminder to intentionally practice thankfulness in our daily lives. Consistently acknowledging what we appreciate not only enhances our own mental and physical health but also positively affects those around us.

What Is Gratitude?

Gratitude means being thankful and ready to show appreciation and return kindness. While saying “thank you” is a common expression of gratitude, it also includes reflecting on positive moments from your day or life and genuinely feeling grateful.

The Profound Health Benefits

The benefits of gratitude extend far beyond simply making someone feel appreciated. Research has consistently demonstrated measurable psychological and physiological advantages for those who practice it regularly.

Mental and Emotional Well-being

Consciously practicing gratitude has been proven to act as a direct counter to stress and anxiety.

- Increased Happiness: Studies show that a single, thoughtful act of gratitude can produce an immediate increase in happiness and a 35% reduction in depressive symptoms.

- Improved Outlook: It fosters greater optimism for the future, improved mental well-being, and greater overall satisfaction with life.

- Reduced Toxic Emotions: Gratitude helps diminish feelings of envy, frustration, resentment, and regret.

- Character Development: It encourages the development of valuable traits like patience, humility, and wisdom.

Physical Health Advantages

The positive effects of gratitude are so deep that they manifest physically:

- Better Health Outcomes: Individuals who focus on gratitude have even reported fewer visits to the doctor.

- Improved Rest: It is linked to better sleep quality and less fatigue.

- Cellular Resilience: Perhaps the most surprising benefit is its effect on the body’s internal state. Regular gratitude is associated with lower levels of cellular inflammation. Since chronic inflammation is a root cause for numerous diseases, this suggests that thankfulness plays a role in long-term disease prevention and better physical health overall.

Simple Ways to Cultivate Gratitude

Building a habit of thankfulness is easy and requires minimal time. Here are practical exercises to strengthen your gratitude muscles every day:

- Daily Acknowledgment: Make it a point to sincerely say “thank you” to people throughout your day.

- Journaling: Keep a dedicated gratitude journal or use a physical gratitude jar to record specific things you are thankful for each day.

- Handwritten Notes: Take the time to write personalized, handwritten thank-you notes.

- Mindful Reflection: Set aside a few minutes daily to think or meditate on positive events.

- Create Rituals: Incorporate thankfulness into a daily routine, such as sharing a high point of the day at the dinner table.

- Visual Reminders: Use sticky notes around your home or workspace to prompt you to pause and appreciate what you have.

The evidence is clear: cultivating an “attitude of gratitude” is not a luxury, but a necessity for optimal health. By committing to mindful reflection and simple daily practices—whether through journaling, enjoying time spent with a loved one, or simply saying thank you—you invest directly in your psychological resilience and physical longevity. Start today to experience the transformative power of thankfulness.

by admin | Nov 17, 2025 | Human Resources

An employee handbook is key for setting workplace expectations and staying compliant. Outdated policies can create legal and operational risk. With evolving compliance requirements in the form of new laws and revised regulations, employers need to keep a watchful eye on their handbook policies to make sure they stay compliant. They should also be sure that the “oldies but goodies” – like harassment prevention and conduct guidelines are up to snuff. If you pulled a template for one of these off the internet in 2007, it’s almost guaranteed to need a refresh.

Using outdated policies can lead to confusion, operational disorder,and potential legal exposure. Here are some key end-of-year activities to make sure you start the new year off right: year:

1. Keep Up with State Leave Laws

State leave laws of all kinds have been trending for years now from paid family leave, to bereavement, to sick and safe leave. If you haven’t had expert help with your handbook policies, there’s a good chance you’re missing key details. For instance:

- California requires accrued paid sick leave with specific accrual caps and revises its law at least some part of that law on an almost yearly basis.

- Many states, including Massachusetts, New York, New Jersey, Washington, and Illinois have paid family and medical leave programs that offer job protection

- Colorado (and a handful of other states) have expanded their paid sick leave to cover public health emergencies

Why it matters: Multi-state employers face a patchwork of rules. Ignoring them can result in fines, penalties, and disputes.

Action for Employers: Audit leave policies against the laws and rules in each state and locality where you have employees. Clearly outline eligibility, accrual, carryover, duration, and payout provisions to avoid disputes.

2. If Your Discrimination, Harassment, and Complaint Policies Feel Outdated, They Probably Are

Your employee handbook should create a safe and inclusive workplace. But many organizations are still relying on policies written years ago that don’t reflect current laws or best practices.

Common gaps include:

- Outdated lists of protected classes that omit new state or federal protections.

- Limited examples of unacceptable behavior.

- Insufficient or unclear complaint procedures.

- Not having specific language or contact information required by state law.

Action for Employers: Refresh anti-harassment, discrimination, and complaint policies to include any and all information required by state law, clear reporting procedures, and protections against retaliation. Pair handbook policies with mandatory training to reinforce expectations.

3. Review Your Workplace Conduct and Social Media Policies

Although employers have a lot of latitude to dictate employee behavior, the National Labor Relations Act does create some limits, several of which you might find surprising. (If you don’t have union activity, you might be surprised to find that this law applies to you at all!) For instance, you can’t prevent employees from complaining about their working conditions or discussing their wages.

Things to check for in your written and unwritten policies:

- Prohibiting Wage Conversations: Even a word-of-mouth rule against wage discussions is problematic. Make sure your managers understand this and that rules again such discussions haven’t found their way into offer letters or handbooks.

- Rules Against Speaking Up or Having a “Bad Attitude”: Rules like this can crop up in many places, including your policy that covers standards of conduct. While you can certainly try to enforce decorum and respectful behavior in the workplace, the devil is in the details, and you need to be careful about over-restricting employee behavior.

- Social Media Limitations: You can certainly restrict social media use during work hours, but generally you can’t stop employees from discussing their employment conditions online (e.g., wages, hours, safety issues, bad management). Unfortunately for employers, there’s a lot of nuance in this area of law.

Action for Employers: Make sure your handbooks policies–and even unwritten practices–don’t run afoul of the National Labor Relations Act.

4. Ensure Handbook Distribution and Acknowledgment

A great handbook is only effective if employees receive it, read it, and acknowledge it. Too often, employers update policies but fail to track distribution or obtain acknowledgments, leaving them unprotected in a dispute.

Best practices include:

- Communicating changes clearly to avoid misunderstandings. If you’ve made big changes to your handbook, point those out when distributing new copies.

- Requiring signed acknowledgment forms or e-signatures from every employee.

- Storing acknowledgments in a secure and easily accessible format.

- If distributing updated handbooks digitally, also have a print version available in an easily accessible location in the workplace.

Action for Employers: Make handbook acknowledgment part of your compliance checklist every year. Ensure everyone receives important updates promptly.

Why Updating Your Employee Handbook Before 2026 Matters

Updating your employee handbook is not just about avoiding penalties. It helps create a compliant, transparent, and inclusive workplace that builds trust and engagement. Employers with up-to-date handbooks will enter 2026 ready to adapt to new laws, strengthen employee relationships, and reduce compliance risk.

By Brian Costello

Originally posted on Mineral