by admin | Jun 30, 2017 | ACA, Group Benefit Plans

Earlier this month, the Department of Labor (DOL) provided an informational FAQ relating to the Mental Health Parity and Addiction Equity Act (MHPAEA) and the 21st Century Cures Act (Cures Act). This is the DOL’s 38th FAQ on implementing the Patient Protection and Affordable Care Act (ACA) provisions and related regulations. The DOL is requesting comments on a draft model form for participants to use to request information regarding nonquantitative treatment limitations, and confirms that benefits for eating disorders must comply with the MHPAEA. Comments are due by September 13, 2017.

The MHPAEA amended various laws and regulations to provide increased parity between mental health and substance use disorder benefits and medical/surgical benefits. Generally, financial requirements such as coinsurance and copays and treatment limitations for mental health and substance use disorder benefits cannot be more restrictive than requirements for medical and surgical benefits. Regulations also provide that a plan or issuer may not impose a nonquantitative treatment limitation (NQTL) unless it is comparable and no more stringent than limitations on medical and surgical benefits in the same classification.

On December 13, 2016, President Obama signed the 21st Century Cures Act into law. The Cures Act has numerous components including directing the Secretary of Health and Human Services, Secretary of Labor, and Secretary of the Treasury (collectively, the Agencies) to issue compliance program guidance, share findings with each other, and issue guidance to group health plans and health insurance issuers to help them comply with the mental health parity rules.

The Agencies must issue guidance to group health plans and health insurance issuers; the guidance must provide information and methods that plans and issuers can use when they are required to disclose information to participants, beneficiaries, contracting providers, or authorized representatives to ensure the plans’ and issuers’ compliance with the mental health parity rules.

The Agencies must issue the compliance program guidance and guidance to group health plans and health plan issuers within 12 months after the date that the Helping Families in Mental Health Crisis Reform Act of 2016 was enacted, or by December 13, 2017.

In the June 2017 FAQ, the DOL reiterated its request for comments on the following questions, originally asked in the fall of 2016:

- Whether issuance of model forms that could be used by participants and their representatives to request information with respect to various NQTLs would be helpful and, if so, what content the model forms should include. For example, is there a specific list of documents, relating to specific NQTLs, that a participant or his or her representative should request?

- Do different types of NQTLs require different model forms? For example, should there be separate model forms for specific information about medical necessity criteria, fail-first policies, formulary design, or the plan’s method for determining usual, customary, or reasonable charges? Should there be a separate model form for plan participants and other individuals to request the plan’s analysis of its MHPAEA compliance?

- Whether issuance of model forms that could be used by States as part of their review would be helpful and, if so, what content the model form should include. For example, what specific content should the form include to assist the States in determining compliance with the NQTL standards? Should the form focus on specific classifications or categories of services? Should the form request information on particular NQTLs?

- What other steps can the Departments take to improve the scope and quality of disclosures or simplify or otherwise improve processes for requesting disclosures under existing law in connection with mental health/substance misuse disorder MH/SUD benefits?

- Are there specific steps that could be taken to improve State market conduct examinations and/or Federal oversight of compliance by plans and issuers?

The DOL is also asking for input on a draft model form that participants, enrollees, or representatives could use to request information from their health plan or issuer regarding NQTLs that may affect their MH/SUD benefits.

The Cures Act also requires that benefits for eating disorders be consistent with the requirements of MHPAEA. The DOL clarified that the MHPAEA applies to any benefits a plan or issuer may offer for treatment of an eating disorder.

By Danielle Capilla

Originally Posted By www.ubabenefits.com

by admin | Jun 27, 2017 | ACA

On June 22, 2017, the United States Senate released a “Discussion Draft” of the “Better Care Reconciliation Act of 2017” (BCRA), which would substitute the House’s House Resolution 1628, a reconciliation bill aimed at “repealing and replacing” the Patient Protection and Affordable Care Act (ACA). The House bill was titled the “American Health Care Act of 2017” (AHCA). Employers with group health plans should continue to monitor the progress in Washington, D.C., and should not stop adhering to any provisions of the ACA in the interim, or begin planning to comply with provisions in either the BCRA or the AHCA.

Next Steps

- The Congressional Budget Office (CBO) is expected to score the bill by Monday, June 26, 2017.

- The Senate will likely begin the voting process on the bill on June 28 and a final vote is anticipated sometime on June 29.

- The Senate and House versions will have to be reconciled. This can be done with a conference committee, or by sending amendments back and forth between the chambers. With a conference committee, a conference report requires agreement by a majority of conferees from the House, and a majority of conferees by the Senate (not both together). Alternatively, the House could simply agree to the Senate version, or start over again with new legislation.

The BCRA

Like the AHCA, the BCRA makes numerous changes to current law, much of which impact the individual market, Medicare, and Medicaid with effects on employer sponsored group health plans. Also like the AHCA, the BCRA removes both the individual and the employer shared responsibility penalties. The BCRA also pushes implementation of the Cadillac tax to 2025 and permits states to waive essential health benefit (EHB) requirements.

The BCRA would change the excise tax paid by health savings account (HSA) owners who use their HSA funds on expenses that are not medical expenses under the Internal Revenue Code from the current 20 percent to 10 percent. It would also change the maximum contribution limits to HSAs to the amount of the accompanying high deductible health plan’s deductible and out-of-pocket limitation and provide for both spouses to make catch-up contributions to HSAs. The AHCA contains those provisions as well.

Like the AHCA, the BCRA would remove the $2,600 contribution limit to flexible health spending accounts (FSAs) for taxable years beginning after December 31, 2017.

The BCRA would allow individuals to remain on their parents’ plan until age 26 (the same as the ACA’s regulations, and the AHCA) and would not allow insurers to increase premium costs or deny coverage based on pre-existing conditions. Conversely, the AHCA provides for a “continuous health insurance coverage incentive,” which will allow health insurers to charge policyholders an amount equal to 30 percent of the monthly premium in the individual and small group market, if the individual failed to have creditable coverage for 63 or more days during an applicable 12-month look-back period.

The BCRA would also return permissible age band rating (for purposes of calculating health plan premiums) to the pre-ACA ratio of 5:1, rather than the ACA’s 3:1. This allows older individuals to be charged up to five times more than what younger individuals pay for the same policy, rather than up to the ACA limit of three times more. This is also proposed in the AHCA.

The ACA’s cost sharing subsidies for insurers would be eliminated in 2020, with the ability of the President to eliminate them earlier. The ACA’s current premium tax credits for individuals to use when purchasing Marketplace coverage would be based on age, income, and geography, and would lower the top threshold of income eligible to receive them from 400 percent of the federal poverty level (FPL) to 350 percent of the FPL. The ACA allowed any “alien lawfully present in the US” to utilize the premium tax credit; however, the BCRA would change that to “a qualified alien” under the definition provided in the Personal Responsibility and Work Opportunity Reconciliation Act of 1996. The BCRA would also benchmark against the applicable median cost benchmark plan, rather than the second lowest cost silver plan.

By Danielle Capilla

Originally Posted By www.ubabenefits.com

by admin | Jun 23, 2017 | Human Resources, Workplace

One of the latest things trending right now in business is the importance of office culture. When everyone in the office is working well together, productivity rises and efficiency increases. Naturally, the opposite is true when employees do not work well together and the corporate culture suffers. So, what are these barriers and what can you do to avoid them?

According to an article titled, “8 ways to ruin an office culture,” in Employee Benefit News, the ways to kill corporate culture may seem intuitive, but that doesn’t mean they still don’t happen. Here’s what organizations SHOULD do to improve their corporate culture.

Provide positive employee feedback. While it’s easy to criticize, and pointing out employees’ mistakes can often help them learn to not repeat them, it’s just as important to recognize success and praise an employee for a job well done. An “attaboy/attagirl” can really boost someone’s spirits and let them know their work is appreciated.

Give credit where credit is due. If an assistant had the bright idea, if a subordinate did all the work, or if a consultant discovered the solution to a problem, then he or she should be publicly acknowledged for it. It doesn’t matter who supervised these people, to the victor go the spoils. If someone had the guts to speak up, then he or she should get the glory. Theft is wrong, and it’s just as wrong when you take someone’s idea, or hard work, and claim it as your own.

Similarly, listen to all ideas from all levels within the company. Every employee, regardless of their position on the corporate ladder, likes to feel that their contributions matter. From the C-suite, all the way down to the interns, a genuinely good idea is always worth investigating regardless of whether the person who submitted the idea has an Ivy League degree or not. Furthermore, sometimes it takes a different perspective – like one from an employee on a different management/subordinate level – to see the best way to resolve an issue.

Foster teamwork because many hands make light work. Or, as I like to say, competition breeds contempt. You compete to get your job, you compete externally against other companies, and you may even compete against your peers for an award. You shouldn’t have to compete with your own co-workers. The winner of that competition may not necessarily be the best person and it will often have negative consequences in terms of trust.

Get rid of unproductive employees. One way to stifle innovation and hurt morale is by having an employee who doesn’t do any work while everyone else is either picking up the slack, or covering for that person’s duties. Sometimes it’s necessary to prune the branches.

Let employees have their privacy – especially on social media. As long as an employee isn’t conducting personal business on company time, there shouldn’t be anything wrong with an employee updating their social media accounts when they’re “off the clock.” In addition, as long as employees aren’t divulging company secrets, or providing other corporate commentary that runs afoul of local, state, or federal laws, then there’s no reason to monitor what they post.

Promote a healthy work-life balance. Yes, employees have families, they get sick, or they just need time away from the workplace to de-stress. And while there will always be times when extra hours are needed to finish a project, it shouldn’t be standard operating procedure at a company to insist that employees sacrifice their time.

By Geoff Mukhtar

Originally Posted By www.ubabenefits.com

by admin | Jun 21, 2017 | Benefit Management, COBRA

The Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) requires employers to offer covered employees who lose their health benefits due to a qualifying event to continue group health benefits for a limited time at the employee’s own cost. Per regulation, qualifying events are specific events that cause or trigger an individual to lose health coverage. The type of qualifying event determines who the qualified beneficiaries are and the maximum length of time a plan must offer continuation coverage. A group health plan may provide longer periods of continuation coverage beyond the maximum 18 or 36 months required by law.

There are seven triggering events that are qualifying events for COBRA coverage if they result in loss of coverage for the qualified beneficiaries, which may include the covered employee, the employee’s spouse, and dependent children.

The following quick reference chart indicates the qualifying event, the individual who is entitled to elect COBRA, and the maximum length of COBRA continuation coverage.

By Danielle Capilla

Originally Posted By www.ubabenefits.com

by admin | Jun 16, 2017 | HSA/HRA

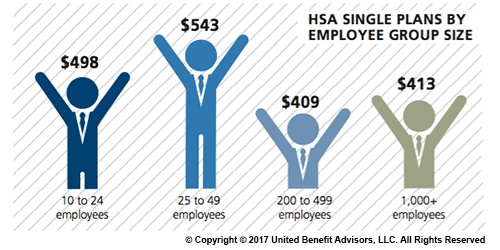

The average employer contribution to an HSA is $474 for a single employee (down 3.5 percent from 2015 and 17.6 percent from five years ago) and $801 for a family (down 9.2 percent from last year and 13.7 percent from five years ago). There was a 26 percent increase in the number of individuals enrolled in HSAs, likely due to the increase in CDHP enrollment (which often have HSAs tied to them). Since 2013, there has been a 97.7 percent increase in enrollment, showing significant employer and employee interest in these plans over time.

Looking at contributions by group size, singles at companies with 200 to 499 employees receive the lowest HSA contributions ($409). Singles at some of the smallest companies (25 to 49 employees) receive the most generous contributions ($543), on average.

Like their single counterparts, families get more generous contributions from small employers. The average family HSA contribution in groups with 25 to 49 employees was $908 (though, in general, small employer contributions have been declining over time).

Last year, some of the smallest companies (10 to 24 employees) had the highest HSA enrollment (16.3 percent). However, rapid enrollment increases among large employers in recent years now places the largest companies (1,000+ employees) as HSA enrollment leaders with 19.1 percent enrolled.

For a detailed look at the prevalence and enrollment rates among HSA and HRA plans by industry and region, view UBA’s “Special Report: How Health Savings Accounts Measure Up”, to understand which aspects of these accounts are most successful, and least successful.

Benchmarking your health plan with peers of a similar size, industry and/or geography makes a big difference in determining if your plan is competitive. To compare your exact plan with your peers, request a custom benchmarking report.

For fast facts about HSA and HRA plans, including the best and worst plans, average contributions made by employers, and industry trends, download (no form!) “Fast Facts: HSAs vs. HRAs”.

By Bill Olson

Originally Posted By www.ubabenefits.com