by admin | Oct 11, 2022 | Employee Benefits, Open Enrollment

Choosing the right benefits during open-enrollment season is so important and can help save money. It can also give individuals and families broader support with their health. Benefits like medical coverage are particularly important with high inflation having such a big impact on people’s budgets.

A survey by UnitedHealthcare found that nearly 40% of employees devote less than one hour to the open enrollment process. It is crucial to carefully analyze your benefits during open enrollment as any decisions you make will likely be locked for the year until the next open enrollment period. Don’t rush into open enrollment without carefully considering your options!

Here are some tips to ensure you make the most of your open enrollment:

Be Prepared

Open enrollment typically lasts for a short period (2-4 weeks) so knowing what you need to do ahead of time can be a big stress reliever. A good starting point is to consider how your needs have changed since last year. For example, maybe you got married or received a raise. These changes may require a change in coverage, whether it be for life, health or disability insurance, and it is important to consider how these or any other expected life changes will impact your insurance needs.

Review Any Changes Made by Your Employer

It is common for employers make changes to plans and premiums to keep up with the times. When you receive your open enrollment packet to review plan options, it is important to consider all aspects of coverage and the total cost of coverage. The total cost is impacted by the deductibles, premiums, co-insurance and maximum out-of-pocket expenses.

Take note of whether your employer made any changes in providers. If this happens, your current physician or dentist may be out-of-network which will result in out-of-network costs or denied claims.

Review Your Insurance Options

The largest portion of employer benefits is health insurance so it is important to choose the plan that is best for you and your family. Important questions to ask are: how often do you have medical expenses? Are lower premiums or lower out-of-pocket costs more important to you? Do you take expensive prescription drugs? Can you afford hefty out-of-pocket costs if there is an emergency?

There are 3 main plan types:

- Preferred Provider Organization (PPO)

PPO’s are a popular choice since they allow you to see any doctor or specialist and don’t require a referral from your primary care physician (PCP) to see a specialist. However, PPO premiums are usually much more than other plans. To help reduce costs, remember that using in-network providers and specialists who are part of your PPO network will save you money.

- Health Maintenance Organization (HMO)

HMOs have lower premiums than PPOs but they require you to stay in-network. You will also need a referral from your PCP to see a specialist. The idea is that the PCP coordinates your care.

- High Deductible Health Plan (HDHP)

Another low-cost option is a high-deductible health plan. What sets HDHPs apart from other plans is their low premiums and high deductibles. That means you won’t have to pay as much each month for premiums but you will need to pay more of the healthcare costs when you need services. To help you pay for the bigger deductible, employers usually pair an HDHP with a health savings account (HSA), which allows you to save for medical expenses, including deductibles and copays.

Learn How FSAs, HRAs, and HSAs Differ

Many employers offer accounts that help you save for medical expenses:

- Flexible Spending Account (FSA)

You decide how much pre-tax money to put into the employer owned account through payroll deductions and then you can use that money to pay for out-of-pocket medical expenses. You lose that money if you change jobs or don’t use it by the end of the year.

- Health Savings Account (HSA)

Connected to a HDHP, an HSA lets you set aside money on a pre-tax basis to pay for qualified medical expenses. The account is yours, so you keep it if you change jobs. The money rolls over each year so you don’t have to worry about “using it or losing it.”

- Health Reimbursement Arrangement (HRA)

An HRA is similar to an HSA except that the employer owns the account so you can’t take it with you when you change jobs. You’re able to contribute money for medical expenses just like an HSA or FSA. Money can also be carried over to the next year like an HSA.

Open enrollment is an important time of year and is worth investing some time and energy to decide what is best for you and your family. Health insurance is one of the most important purchases you make. By doing your homework and taking the time to carefully consider your options, you’ll find the plan that is right for you!

by admin | Jun 13, 2022 | Hot Topics

Smart spending can keep your health care from costing an arm and a leg. With costs rising on everything from gas to food, every penny counts. It pays to shop smart – that is why it helps to learn how to take steps to limit your out-of-pocket health care costs.

- Save Money on Prescriptions

- Go generic – Always ask your doctor or pharmacist if you can switch to generic medicines. They have the same active ingredients but cost less than brand name drugs.

- Split pills – ask your doctor or pharmacist if your prescription comes in a higher dose that is safe to split. You may be able to get a 2-month supply of medicine in double the dose that you need for the price of a 1-month supply, cutting your prescription cost in half.

- Use a preferred pharmacy – A preferred pharmacy has pre-negotiated lower prices on prescriptions for a particular insurance plan. You can also sign up for home delivery on prescriptions that you take on a regular basis.

- Tune in to Telehealth

With telemedicine, you don’t have to drive to the doctor’s office or sit in a waiting room when you’re sick. Virtual visits can be easier to fit into your busy schedule and you may not even have to arrange for childcare. Doctors also can use telehealth appointments to lessen exposure to other people’s germs.

- Brush Up on HSA & FSA Eligible Expenses

You can withdraw HSA and FSA money tax-free to pay for deductibles and co-payments or coinsurance, as well as for a variety of other expenses including vision expenses and orthodontia. You can also use it for everything from sunscreen and contact solution to baby monitors and over-the-counter medicine like Ibuprofen or cold medicine.

- Save for Retirement with Your HSA

HSA funds don’t expire which makes an HSA a great way to put away money for medical expenses in retirement. An HSA offers a hat trick of tax advantages:

- Contributions to your account are made pre-tax, lowering your taxable income today

- Investments grow tax-free while they are kept in the account

- Withdrawals are free of income tax, as long as you use the money for qualified medical expenses.

Age 65 is when you can use HSA money to pay for non-medical expenses – including day-to-day costs or for home renovations. Those payouts aren’t tax-free but are taxed at the same rate as distributions from a traditional IRA. You’ll simply owe income taxes on whatever you withdraw.

- Review Bills and Insurance Explanations of Benefits

Billing mistakes can happen. In fact, did you know that up to 80% of medical bills contain at least one error? Billing mistakes happen easily when dealing with large numbers of patients, ever-changing medical codes, and payments crossed in the mail and health insurance companies.

The portion of your budget devoted to medical care is always on the rise so it’s never a bad idea to find monetary shortcuts where you can. Knowledge is POWER and when you spend time finding ways to save money on health care, you are empowering yourself! Exercising due diligence to plan for you and your family’s medical needs will save you money and give you confidence in your decisions for care.

by admin | Apr 14, 2022 | Benefit Plan Tips, Tricks and Traps, Hot Topics

Health insurance is essential to protecting your health but the high cost of coverage may leave you feeling sick. Even after employers pick up a substantial amount of the cost, every year Americans spend thousands of dollars on healthcare while costs are continuing to rise. By taking certain steps, you can stretch your healthcare dollars and still receive the care you need to stay healthy.

- Understand How Your Health Plan Works

Review your plan to learn how to maximize your benefits. You need to know what is covered (and what is not!) and what procedures you need to follow to ensure your claims will get paid. Know what your copayment, coinsurance and deductible costs are before your visit.

Most health insurance plans cover more of your costs if you use their preferred or in-network doctors. If you visit an out-of-network doctor or medical facility, you’ll pay more and may end up being responsible for 100% of the bill. Use your insurer’s online tools to search for in-network providers.

- Choose the Right Places to Get Care

Running to the emergency room when you get sick after hours could drain your wallet. All too often, those suffering from minor illnesses or injuries visit the ER when they don’t need to. The ER should be your last resort – consider using more affordable options like telemedicine or an urgent care center instead. You can still get the care you require in off-hours without having to schedule an appointment.

If you need surgery, you may save money by having it done at an ambulatory surgical center (ASC) which is a modern healthcare facility focused on same-day surgical care, including diagnostic and preventive procedures. Typically, these centers charge less than a hospital.

- Use a Health Savings Account (HSA) or Flexible Spending Account (FSA)

Opening a HSA or an FSA is a handy way to save for medical expenses and reduce your taxable income. They are like personal savings accounts but the money in them is used to pay for health care expenses. HSAs are owned by you, earn interest, and can be transferred to a new employer. FSAs are owned by your employer, do not earn interest, and must be used within the calendar year.

- Ask Your Doctor About Remote Patient Monitoring (RPM)

RPM is the use of digital technologies to monitor and analyze medical and other health data from patients and electronically transmit this information to healthcare providers for assessment and, when necessary, recommendations and instructions. This type of monitoring is often used to manage high-risk patients, such as those with acute or chronic health conditions such as those with diabetes, hypertension and heart conditions.

- Use Your Preventive Care Benefits

Many health plans pay the full cost for important preventive care. These regular screenings, exams, and immunizations help detect or prevent diseases and medical problems early when they are easier to treat. Annual check-ups, mammograms (usually after the age of 40), flu shots and colonoscopies (usually 1 every 10 years after the age of 50) are examples of preventive care. These checks can save you a lot of money because they catch problems early.

Health insurance isn’t mandatory – there’s no law requiring you to buy it – but, health insurance is an important part of staying healthy, financially and physically. Since most people who don’t have insurance made that decision based on money instead of what is best for their health, they usually don’t have doctor appointments for the same reason – it’s too expensive. But skipping routine care can end up being more expensive than your premiums, especially if you have serious health issues that aren’t caught early. Think of it like care maintenance: regularly changing your oil might be a hassle but it is essential to prevent a major breakdown down the road.

by admin | Mar 9, 2022 | Hot Topics

Let’s say that you visited the doctor and you are wondering how much that visit is going to cost. A short while later, you receive something in the mail that looks like a bill – and even says “amount you owe” at the bottom. However, it doesn’t have a return envelope or tear-off portion for the bill. Confused? You’re not the only one!

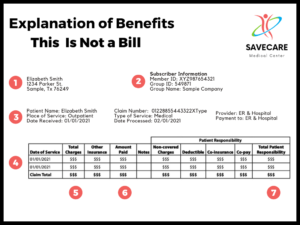

Most likely, you’ve just received an Explanation of Benefits (EOB) from your insurance company. The most important thing for you to remember is that an EOB is NOT a bill. It is essentially “one big receipt” that explains your visit. It shows what was billed, how much you can expect your health plan to pay, and what you – the patient – have to pay. It is always important to review your EOB to make sure it is correct.

An EOB is a tool that shows you the value of your health plan. It will detail the cost of the services you received and how much your insurance will pay.

How do EOB’s work?

The health care provider will bill your insurance company after your doctor visit. Then, your insurance company will send your EOB. Later, you will receive a bill for the amount you owe. However, if the bill does arrive before the EOB, don’t pay it yet. Wait until you have the EOB in hand so you can compare it to your medical bill.

While an EOB will differ from one insurance company to another, they typically all include the following information:

- The Account Summary – lists your account information with details like the patient’s name, date(s), and claim number.

- The Claim Details – lists the services provided and the dates of the services.

- The Amounts Billed – details the cost of the services and what costs your health plan did not cover. It will also include any outstanding amount you are responsible for paying. If there is a portion that is not covered by insurance, the reason why will also be listed.

Remember, insurance companies rarely pay 100% of the bill. You will need to pay any applicable deductible, copay and coinsurance.

Deductible: The amount you pay for health care services before your insurance begins to pay anything.

Copay: A flat fee that you pay on the spot each time you go to your doctor or fill a prescription.

Coinsurance: The portion of the medical cost you pay after your deductible has been met. Coinsurance is a way of saying that you and your insurance carrier each pay a share of eligible costs that add up to 100%.

Why is Your EOB important?

Medical billing companies sometimes make billing errors. Your EOB is a window into your medical billing history. Review it carefully to make sure that you did receive the service being billed and that your procedure and diagnosis are listed and coded correctly.

EOBs can help you understand how the health insurance system works and provide transparency in the complicated finances of health care. While the EOB may be complicated, understanding it can help ensure that you and your family get the most out of your health insurance. Knowing what an EOB is and what is included on the statement ensures that you stay in control of your health care finances.

by admin | Dec 26, 2021 | Employee Benefits

Employee benefits are a major bargaining chip for companies looking to attract talent. The problem is healthcare costs are skyrocketing, and it’s difficult for employers to offer the same level of coverage. Higher costs are either resulting in less coverage or smaller wages for employees.

Find out what’s happening with healthcare and recruitment, and get tips on what companies can do to stay competitive:

The Rising Costs of Healthcare

It’s no secret that healthcare costs have been increasing for years. According to the research, it will continue to increase. One study from the Peterson Center on Healthcare and the Kaiser Family Foundation (KFF) found that $3.8 trillion—or $11,582 per person— was spent on healthcare in 2019. By 2028, individual Americans will be spending around $18,000 on healthcare.

While the issue is complex, experts agree that the major factors in this spike include an aging population, a rise in chronic disease, and higher prices for medical services and drugs. Costs are rising so rapidly that insurers are increasing deductibles, not covering certain services, or applying caps. As a result, healthcare packages are playing a larger role when chosen candidates are deciding whether to accept a new job.

How Important Are Competitive Healthcare Packages?

As healthcare costs continue to rise, a new debate has emerged. Should employers or employees take more responsibility for covering healthcare?

One of two things are happening with workplace healthcare. Either employees are leaving their current position for a job with better healthcare coverage or their annual salary increases are being eaten up by higher healthcare premiums being passed on to employees.

A recent survey found that 42% of employees are thinking about leaving their current position because of inadequate benefits.

“The rising price of health care costs families thousands of dollars a year in foregone wages, out-of-pocket costs, and increased taxes,” said Josh Bivens, research director at the Economic Policy Institute, in an interview with MarketWatch.

He said the effect may not be apparent, but it’s one of the main reasons wages have remained stagnant. If you spot a number of paradoxes here, then you aren’t alone. Lower salaries won’t attract top talent, and passing on the costs of healthcare to current employees won’t retain them. This quandary for employers is compounded by the current labor shortage, which is often referred to as the Great Resignation.

What Can Companies Do?

It’s clear that healthcare is important to job candidates. To attract new talent, companies should revolutionize the way they treat wellness in the workplace.

Promoting health and wellness initiatives not only improves employee morale and decreases absenteeism, but a healthier workforce is less likely to use their insurance. This may eventually equate to lower premiums.

Another easy way to curb costs is by communicating with employees about what plans are available. Health insurance is often a complex topic, and some employees may accidentally choose the wrong plan because they don’t understand the difference.

Proactively highlighting available services can assist employees before a medical issue spins out of control. Mental health services are an example of this. Letting employees know about Employee Assistance Programs or low-cost telehealth options could offer help before a more serious intervention is needed.

There are many options available for companies to make their benefit packages more competitive to attract top talent. Some companies are considering Health Savings Accounts or HSAs that help employees pay medical bills while enrolled in cheaper, high deductible plans.

Direct Primary Care is another technique being used by companies to control costs. DPC allows employees to pay fixed monthly, quarterly, or annual fees to cover primary care, consultations, care coordination, and comprehensive care management. Not only does DPC result in cost-savings, but it fosters a better relationship between patient and doctor.

Leveraging Your Benefits

Even though healthcare costs continue to rise, it’s possible for companies to control costs by promoting wellness initiatives and helping employees select the best benefit package for their needs.

Being proactive with healthcare and making smart financial decisions can keep healthcare prices reasonable, and ensure that companies will be able to attract talent.

By Mckenzie Cassidy

Orginally posted on HR Exchange Network