by admin | Oct 15, 2024 | Employee Benefits, Flexible Spending Accounts

When it comes to health insurance, there is a lot of jargon and plenty of acronyms. Many people have heard of FSAs, but may not actually know — what is a flexible spending account, exactly?

If you have an employer-sponsored health plan, a flexible spending account (FSA) is often available as part of the benefits package. There are two types of FSAs: one for health and medical expenses and another for dependent care/childcare costs. Both are designed to help you set aside money during the year for out-of-pocket expenses while enjoying tax benefits.

When you contribute to an FSA, the money is taken from your paycheck before taxes are removed and is never taxed. The Federal FSA Program estimates that those with an FSA save 30 percent on healthcare expenses on average.

How Does an FSA Work?

- Contributions: You contribute a portion of your pre-tax salary to your FSA. You set a contribution amount to be deducted from each paycheck, up to the federal limit, which for 2024 is $3,200.

- Rollovers, etc.: Employers have the option of allowing employees to roll over up to $640 in 2024 or they can provide a 2 ½ month grace period during which employees can spend their remaining contributions, but they can’t offer both.

- Reimbursement: Use your FSA funds to pay for qualified medical expenses. You typically submit receipts for reimbursement.

- Tax Benefits: Contributions are made with pre-tax dollars, reducing your taxable income.

What Can You Spend Your FSA Money On?

- Medical expenses: Doctor’s visits, prescriptions, dental care, vision care, and mental health services

- Over-the-counter medications: Many OTC medications, like pain relievers and allergy medications

- Medical equipment: Items such as crutches, wheelchairs, and diabetic supplies

- Dependent care expenses: Childcare or elder care costs, which can include before and after school care, preschool, and adult day care. In 2024, employees may contribute up to $5,000 if filing jointly or $2,500 if filing taxes separately.

Key Points to Remember:

- Use-It-or-Lose-It: Generally, any unused FSA funds at the end of the year are forfeited. However, some plans offer a grace period or carryover options.

- Contribution Limits: There are annual contribution limits for FSAs, set by the IRS.

- Dependent Care Expenses: If you have dependent care expenses, you can use your FSA to pay for them up to a certain limit.

Is an FSA Right for You?

Opening an FSA is a great way to save money on taxes and prepare for healthcare costs. As with other types of savings accounts, it allows you to contribute and stash away money, but in this case, that money is taken out of your paychecks in a set amount and is nontaxable. Check to see if your employer matches contributions as well.

Understanding the rules, benefits, and limitations of these accounts will allow you to maximize their value and ensure you’re making the most of this valuable employee benefit.

by admin | Aug 2, 2024 | Employee Benefits

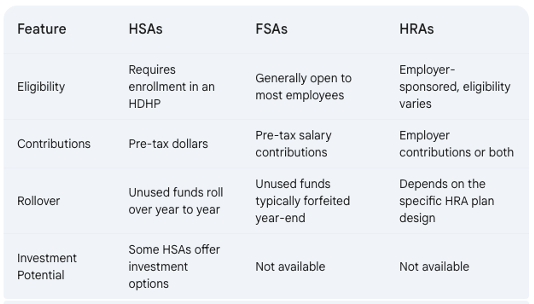

Managing healthcare costs can feel like deciphering a complex code. Three acronyms frequently pop up: HSAs, HRAs, and FSAs. But what exactly do they mean, and which one is right for you? Let’s break down these accounts and explore how they can help you save on qualified medical expenses.

Understanding the Accounts:

-

Health Savings Accounts (HSAs): You contribute pre-tax dollars to your HSA, which acts like a savings account dedicated to qualified medical expenses, including most over-the-counter (OTC) medications. However, to be eligible for an HSA, you must be enrolled in an High Deductible Health Plan (HDHP), which has a higher deductible than traditional health insurance plans. This means you’ll pay more out-of-pocket before your insurance kicks in. HSAs essentially act as a safety net to offset these higher deductible costs.

-

Flexible Spending Accounts (FSAs): These accounts allow you to set aside pre-tax salary contributions to cover qualified medical and dependent care expenses throughout the year. Think of it like a prepaid debit card for approved healthcare costs. Most OTC medications are eligible for reimbursement through an FSA debit card or claim submission process. Unlike HSAs, FSAs are not tied to a specific health insurance plan type, so you might have the option to contribute to an FSA even with a traditional plan (though some employers may have restrictions based on your plan selection). o FSAs have a “use it or lose it” provision: Generally, you must use the money in a FSA within the plan year (but occasionally your employer can offer a grace period of a few months).

-

Health Reimbursement Arrangements (HRAs): These employer-sponsored accounts let companies contribute funds to cover qualified employee medical expenses. The specific eligible expenses, including OTC items, vary depending on the HRA plan design set by your employer. Unlike HSAs and FSAs, you don’t directly contribute to an HRA. Instead, your employer contributes on your behalf, or in some cases, a combination of employer and employee contributions may be allowed.

Who Can Use Them?

-

HSAs: Eligibility hinges on having an HDHP.

-

FSAs: Generally available to most employees, regardless of health plan type (though some employers may restrict enrollment based on plan selection).

-

HRAs: Offered at the discretion of your employer, who determines eligibility and contribution levels.

Tax Benefits:

All three accounts offer tax advantages:

-

Contributions: Reduce your taxable income by contributing pre-tax dollars.

-

Growth: Interest earned on the funds in HSAs and some FSAs (depending on the plan) grows tax-free, allowing your savings to accumulate faster.

-

Withdrawals: When used for qualified medical expenses, withdrawals are tax-free for all three accounts.

Key Differences:

Choosing the Right Account for You:

The best account for you depends on your individual circumstances. Here are some factors to consider:

- Health Status: If you’re generally healthy and have predictable medical expenses, an FSA might be a good choice, allowing you to use the funds throughout the year.

- Financial Risk Tolerance: HSAs offer long-term savings potential with rollovers and investment options (in some plans). However, they require enrollment in an HDHP, which means you’ll shoulder higher upfront costs before insurance kicks in. Consider your comfort level with potentially higher out-of-pocket expenses.

- Employer Benefits: HRAs depend on your employer’s plan design. If your employer offers a generous HRA with significant contributions, it might be a good option for you.

Additional Considerations:

- Use-It-or-Lose-It vs. Rollover: FSAs typically operate on a “use-it-or-lose-it” basis, so plan your contributions carefully to avoid losing funds.

Making an Informed Decision:

By thoroughly understanding HSAs, FSAs, and HRAs, you can choose the account that best aligns with your health needs, financial goals, and employer benefits, ultimately saving you money on healthcare expenses.

by admin | Nov 29, 2023 | Employee Benefits, Health Insurance

If you have a health plan through a job, you can use a Flexible Spending Account (FSA) to pay for health care costs, like deductibles, copayments, coinsurance, and some drugs. They can lower your taxes.

How Flexible Spending Accounts work

A Flexible Spending Account (FSA, also called a “flexible spending arrangement”) is a special account you put money into that you use to pay for certain out-of-pocket health care costs.

You don’t pay taxes on this money. This means you’ll save an amount equal to the taxes you would have paid on the money you set aside.

Employers may make contributions to your FSA, but they aren’t required to.

With an FSA, you submit a claim to the FSA (through your employer) with proof of the medical expense and a statement that it hasn’t been covered by your plan. Then, you’ll get reimbursed for your costs. Ask your employer about how to use your specific FSA.

To learn more about FSAs:

Facts about Flexible Spending Accounts (FSA)

- They are limited to $3,050 per year per employer. If you’re married, your spouse can put up to $3,050 in an FSA with their employer too.

- You can use funds in your FSA to pay for certain medical and dental expenses for you, your spouse if you’re married, and your dependents.

- You can spend FSA funds to pay deductibles and copayments, but not for insurance premiums.

- You can spend FSA funds on prescription medications, as well as over-the-counter medicines with a doctor’s prescription. Reimbursements for insulin are allowed without a prescription.

- FSAs may also be used to cover costs of medical equipment like crutches, supplies like bandages, and diagnostic devices like blood sugar test kits.

- Get a list of generally permitted medical and dental expenses from the IRS.

- You can’t use a Flexible Spending Account with a Marketplace plan.

FSA limits, grace periods, and carry-overs

You generally must use the money in an FSA within the plan year. But your employer may offer one of 2 options:

- It can provide a “grace period” of up to 2 ½ extra months to use the money in your FSA.

- It can allow you to carry over up to $610 per year to use in the following year.

Your employer doesn’t have to offer these options. If it does, it can be either one of these options, but not both.

Plan ahead At the end of the year or grace period, you lose any money left over in your FSA. Don’t put more money in your FSA than you think you’ll spend within a year on things like copayments, coinsurance, drugs, and other allowed health care costs.

Originally posted on Healthcare.gov

by admin | Nov 30, 2021 | Flexible Spending Accounts

The end of the year is drawing near which may mean you have some extra money to spend.

No, you didn’t read that wrong. Many Americans have money in their Flexible Savings Accounts (FSAs) that they need to use up before the end of the year. FSAs provide the benefit of putting pre-tax money aside which optimizes your money. Your FSA is set up through your employer and everyone’s rules are a little different. However, most plans run January 1 – December 31. Some companies allow their employees to roll over a set amount into the new year. Checking with your HR department will help you maximize your hard-earned money.

Typically, FSA money has to be used by the end of the year but the COVID-19 relief bill gets you one more year to spend. That means you have until December 31, 2021 to spend FSA money earmarked for last year. The extension also applies for your 2021 FSA money – the credit will be available until the end of 2022.

All funds remaining in the account at the end of the grace period are forfeited according to the “use-it-or-lose-it” rule, which requires all remaining funds in an FSA to be forfeited at the end of the plan year.

If you have FSA money to spend, we’ve compiled a list of some ways to use up your hard-earned FSA dollars that you may not have thought possible:

Fill Your Medicine Cabinet

You can once again purchase over the counter medication with FSA money thanks to the CARES Act. You can stock up on first aid kits or other items that don’t require a prescription such as:

- Bandages

- Heating pads

- Contraceptives

- Fertility and Pregnancy Tests

- Sleep aids such as Melatonin or a sleep mask

- Motion sickness medication

- Headache medicine

- Antacids or heartburn medication

- Menstrual products

- Contact Solution

- Allergy medication

- Acne creams and cleansers

Alternative Therapies

Under IRS law, certain alternative therapies are eligible for reimbursement. Acupuncture and chiropractic care, alternative medicinal treatments, and herbal supplements are a great way to use up your funds for the year and get a little cash back when you most need it.

Dental

Dental benefits often work differently than medical coverage. According to the American Dental Association, this benefit is often capped annually – generally between $1,000 and $2,000. If you have unused funds remaining in your FSA, now may be the time to schedule a last-minute appointment with your dentist, especially if you might need serious work down the road. This way, you can use up the funds remaining in your account by year-end and reduce your out-of-pocket expense next year.

Prescription Refills

Refilling your prescription medications at year end are a great way to use up your funds in your medical FSA. Take inventory of your prescription drugs, toss out expired ones, and make that call for a refill to your doctor or pharmacy.

Medical Equipment and Supplies

Medical equipment and supplies are eligible for reimbursement under a medical FSA. Walking aids like canes, walkers and crutches, blood pressure monitors, thermometers, and joint braces are just a few. Please note that some will require a note or prescription from your doctor.

Mileage and Other Healthcare-Related Extras

Traveling to and from any medical facility for appointments or treatment for yourself or a dependent are eligible for reimbursement under your FSA. This not only includes traveling by your own vehicle, but also by bus, train, plane, ambulance service and includes parking fees and tolls. However, transportation expenses are not eligible with a Dependent Care Flexible Spending Account (DCFSA).

Family Planning

You can put your FSA dollars to work if you are a new or soon-to-be mom on products such as pregnancy tests, fertility monitors, prenatal vitamins and breastfeeding supplies. On the flip side, condoms and other contraceptives are also FSA eligible.

Nicotine Cessation Products

If you are trying to quit smoking, you can use your FSA funds toward nicotine gum, patches, lozenges, inhalers and nasal sprays.

Dependent Care

If you have opted to contribute to a DCFSA, you can get reimbursed for day care, preschool, summer camps and non-employer sponsored before and after school programs. In addition, funds contributed to this type of FSA can be used for elderly daycare if you’re covering more than 50% your parent’s maintenance costs.

Ancestry Kits with Health Reports

Interested in learning about your heritage and how your DNA can affect your health? You are in luck! Ancestry kits like 23andMe that include health reports are typically considered FSA eligible to be reimbursed approximately 50%.

People often don’t use their FSA out of fear that they need to save it for later. However, every year $400-500 million in FSA funds is forfeited. Lost cash is never a good thing. If you still have leftover funds, consider going to the FSA Store where you can find hundreds of eligible items and pay for them with your account dollars without ever leaving your house.

This list is not an exhaustive list of ways to spend your FSA money. Check with your HR department and insurance agent if you have questions about qualified expenses.

by Johnson and Dugan | Dec 13, 2019 | Benefit Management, Compliance, Flexible Spending Accounts

California law AB1554, signed into law by Governor Newsom on August 30, 2019, describes a new requirement for employers to advise participants in a Flexible Spending Account (FSA) of claim deadlines before the end of the plan year. Per the law: “This bill would require an employer to notify, in a prescribed manner, an employee who participates in a flexible spending account of any deadline to withdraw funds before the end of the plan year.”

Two different forms must be used, one of which can be electronic. Examples of notification options are “(1) Electronic mail communication. (2) Telephone communications. (3) Text message notification. (4) Postal mail notification. (5) In-person notification.”

Incorporating the claim filing deadline in your annual FSA open enrollment communications would satisfy this requirement as long as it is provided in two forms of the suggested methods. Terminated employees must also be notified of the claim filing deadline. This could be done in exit paperwork, verbally in an exit interview or sent electronically.

A poster could also be posted in an area that is accessible to all employees and should include the annual claim filing deadline as well as the deadline to file after the last day of employment, if mid-year. Click Here for a sample poster.

Your Johnson & Dugan team can work with you to incorporate this notice in your communications and meet this new requirement.