by admin | Feb 22, 2018 | Hot Topics, Human Resources

Have you ever heard the proverb “Knowledge is power?” It means that knowledge is more powerful than just physical strength and with knowledge people can produce powerful results. This applies to your annual medical physical as well! The #1 goal of your annual exam is to GAIN KNOWLEDGE. Annual exams offer you and your doctor a baseline for your health as well as being key to detecting early signs of diseases and conditions.

According to Malcom Thalor, MD, “A good general exam should include a comprehensive medical history, family history, lifestyle review, problem-focused physical exam, appropriate screening and diagnostic tests and vaccinations, with time for discussion, assessment and education. And a good health care provider will always focus first and foremost on your health goals.”

Early detection of chronic diseases can save both your personal pocketbook as well as your life! By scheduling AND attending your annual physical, you are able to cut down on medical costs of undiagnosed conditions. Catching a disease early means you are able to attack it early. If you wait until you are exhibiting symptoms or have been symptomatic for a long while, then the disease may be to a stage that is costly to treat. Early detection gives you a jump start on treatments and can reduce your out of pocket expenses.

When you are prepared to speak with your Primary Care Physician (PCP), you can set the agenda for your appointment so that you get all your questions answered as well as your PCP’s questions. Here are some tips for a successful annual physical exam:

- Bring a list of medications you are currently taking—You may even take pictures of the bottles so they can see the strength and how many.

- Have a list of any symptoms you are having ready to discuss.

- Bring the results of any relevant surgeries, tests, and medical procedures

- Share a list of the names and numbers of your other doctors that you see on a regular basis.

- If you have an implanted device (insulin pump, spinal cord stimulator, etc) bring the device card with you.

- Bring a list of questions! Doctors want well informed patients leaving their office. Here are some sample questions you may want to ask:

- What vaccines do I need?

- What health screenings do I need?

- What lifestyle changes do I need to make?

- Am I on the right medications?

Becoming a well-informed patient who follows through on going to their annual exam as well as follows the advice given to them from their physician after asking good questions, will not only save your budget, but it can save your life!

by admin | Feb 12, 2018 | Benefit Management, Compliance, Group Benefit Plans, Medicare

Do you offer health coverage to your employees? Does your group health plan cover outpatient prescription drugs? If so, federal law requires you to complete an online disclosure form every year with information about your plan’s drug coverage. You have 60 days from the start of your health plan year to complete the form. For instance, for a calendar-year health plan, this year’s deadline is March 1, 2018.

Background

The Centers for Medicare and Medicaid Services (CMS) is a federal agency that collects data and administers various federal programs. The agency utilizes the CMS online tool to collect information from employers about whether their group health plan’s prescription drug coverage is creditable or noncreditable. Creditable coverage means the group health plan’s prescription drug coverage is actuarially equivalent to Medicare’s Part D drug plans. In other words, the group plan is considered creditable if its drug benefits are as good as or better than Medicare’s benefits.

To confirm whether your plan provides creditable or noncreditable coverage, check with the plan’s carrier or HMO (if insured) or the plan’s actuary (if self-funded). CMS provides guidance to help plan sponsors, carriers, and actuaries determine the plan’s status.

Deadline for Disclosure

All group health plans that include any outpatient prescription drug benefits, regardless of whether the plan is insured, self-funded, grandfathered, or nongrandfathered, must complete the CMS disclosure requirement. There is no exception for small employers.

Complete the CMS online disclosure form every year within 60 days of the start of the plan year. For instance, for calendar-year plans, this year’s deadline is March 1, 2018.

Additionally, if your plan terminates or its status changes between creditable and noncreditable coverage, you must disclose the updated information to CMS within 30 days of the change.

Completing the Disclosure Form

The CMS online tool is the only method allowed for completing the required disclosure. From this link, follow the prompts to respond to a series of questions regarding the plan. The link is the same regardless of whether the employer’s plan provides creditable or noncreditable coverage.

The entire process usually takes only 5 or 10 minutes to complete. To save time, have the following information handy before you start filling in the form:

- Information about the plan sponsor (employer): Name, address, phone number, and federal Employer Identification Number (EIN).

- Number of prescription drug options offered (e.g., if employer offers two plan options with different benefit levels, the number is “2”).

- Creditable/Noncreditable Offer: Indicate whether all options are creditable or noncreditable or whether some are creditable and others are noncreditable.

- Plan year beginning and ending dates.

- Estimated number of plan participants eligible for Medicare (and how many are participants in the employer’s retiree health plan, if any).

- Date that the plan’s Notice of Creditable (or Noncreditable) Coverage was provided to participants.

- Name, title, and email address of the employer’s authorized individual completing the disclosure.

We suggest you print a copy of the completed disclosure to keep for your records.

Note: Employers that receive the Retiree Drug Subsidy (RDS), or sponsor health plans that contract directly with one or more Medicare Part D plans, should seek the advice of legal counsel regarding the applicable disclosure requirements.

Additional Disclosure Requirement

Separate from the CMS online disclosure requirement, employers also must distribute a disclosure notice to Medicare-eligible group health plan participants. The deadline for distributing the participant notice is October 14 of the preceding year. It often is difficult for employers to identify which employees and spouses may be Medicare-eligible, so most employers simply distribute the notice to all participants regardless of age or status. For information about the notice requirement, see our previous post.

Originally Published By ThinkHR.com

by admin | Feb 6, 2018 | Benefit Management, Employee Benefits, Group Benefit Plans

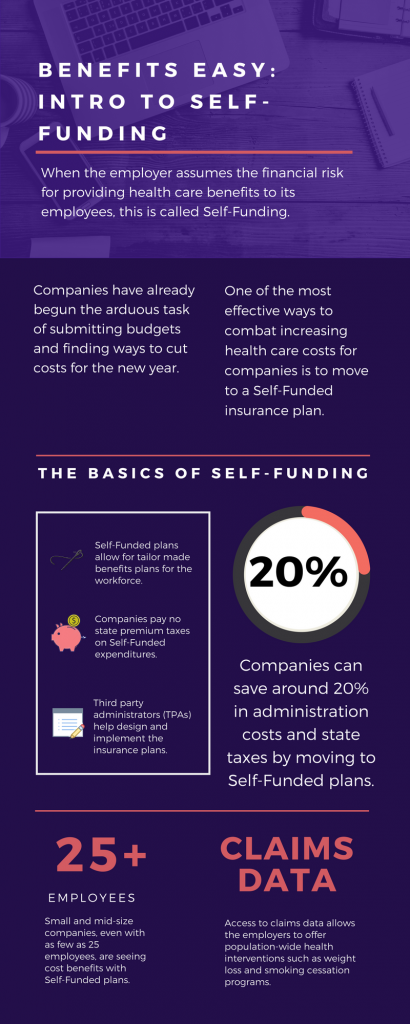

As we head into the second month of 2018, companies have already begun the arduous task of submitting budgets and finding ways to cut costs for the new year. One of the most effective ways to combat increasing health care costs for companies is to move to a Self-Funded insurance plan. By paying for claims out-of-pocket instead of paying a premium to an insurance carrier, companies can save around 20% in administration costs and state taxes. That’s quite a cost savings!

The topic of Self-Funding is huge and so we want to break it down into smaller bites for you to digest. This month we want to tackle a basic introduction to Self-Funding and in the coming months, we will cover the benefits, risks, and the stop-loss associated with this type of plan.

THE BASICS

- When the employer assumes the financial risk for providing health care benefits to its employees, this is called Self-Funding.

- Self-Funded plans allow the employer to tailor the benefits plan design to best suit their employees. Employers can look at the demographics of their workforce and decide which benefits would be most utilized as well as cut benefits that are forecasted to be underutilized.

- While previously most used by large companies, small and mid-sized companies, even with as few as 25 employees, are seeing cost benefits to moving to Self-Funded insurance plans.

- Companies pay no state premium taxes on self-funded expenditures. This savings is around 1.5% – 3/5% depending on in which state the company operates.

- Since employers are paying for claims, they have access to claims data. While keeping within HIPAA privacy guidelines, the employer can identify and reach out to employees with certain at-risk conditions (diabetes, heart disease, stroke) and offer assistance with combating these health concerns. This also allows greater population-wide health intervention like weight loss programs and smoking cessation assistance.

- Companies typically hire third-party administrators (TPA) to help design and administer the insurance plans. This allows greater control of the plan benefits and claims payments for the company.

As you can see, Self-Funding has many facets. It’s important to gather as much information as you can and weigh the benefits and risks of moving from a Fully-Funded plan for your company to a Self-Funded one. Doing your research and making the move to a Self-Funded plan could help you gain greater control over your healthcare costs and allow you to design an original plan that best fits your employees.

by admin | Jan 10, 2018 | Employee Benefits, Human Resources

Have you heard the saying “the eyes are the window to your soul”? Well, did you know that your mouth is the window into what is going on with the rest of your body? Poor dental health contributes to major systemic health problems. Conversely, good dental hygiene can help improve your overall health. As a bonus, maintaining good oral health can even REDUCE your healthcare costs!

Researchers have shown us that there is a close-knit relationship between oral health and overall wellness. With over 500 types of bacteria in your mouth, it’s no surprise that when even one of those types of bacteria enter your bloodstream that a problem can arise in your body. Oral bacteria can contribute to:

- Endocarditis—This infection of the inner lining of the heart can be caused by bacteria that started in your mouth.

- Cardiovascular Disease—Heart disease as well as clogged arteries and even stroke can be traced back to oral bacteria.

- Low birth weight—Poor oral health has been linked to premature birth and low birth weight of newborns.

The healthcare costs for the diseases and conditions, like the ones listed above, can be in the tens of thousands of dollars. Untreated oral diseases can result in the need for costly emergency room visits, hospital stays, and medications, not to mention loss of work time. The pain and discomfort from infected teeth and gums can lead to poor productivity in the workplace, and even loss of income. Children with poor oral health miss school, are more prone to illness, and may require a parent to stay home from work to care for them and take them to costly dental appointments.

So, how do you prevent this nightmare of pain, disease, and increased healthcare costs? It’s simple! By following through with your routine yearly dental check ups and daily preventative care you will give your body a big boost in its general health. Check out these tips for a healthy mouth:

- Maintain a regular brushing/flossing routine—Brush and floss teeth twice daily to remove food and plaque from your teeth, and in between your teeth where bacteria thrive.

- Use the right toothbrush—When your bristles are mashed and bent, you aren’t using the best instrument for cleaning your teeth. Make sure to buy a new toothbrush every three months. If you have braces, get a toothbrush that can easily clean around the brackets on your teeth.

- Visit your dentist—Depending on your healthcare plan, visit your dentist for a check-up at least once a year. He/she will be able to look into that window to your body and keep your mouth clear of bacteria. Your dentist will also be able to alert you to problems they see as a possible warning sign to other health issues, like diabetes, that have a major impact on your overall health and healthcare costs.

- Eat a healthy diet—Staying away from sugary foods and drinks will prevent cavities and tooth decay from the acids produced when bacteria in your mouth comes in contact with sugar. Starches have a similar effect. Eating healthy will reduce your out of pocket costs of fillings, having decayed teeth pulled, and will keep you from the increased health costs of diabetes, obesity-related diseases, and other chronic conditions.

There’s truth in the saying “take care of your teeth and they will take care of you”. By instilling some of the these tips for a healthier mouth, not only will your gums and teeth be thanking you, but you may just be adding years to your life.

by admin | Sep 27, 2017 | Benefit Plan Tips, Tricks and Traps, Employee Benefits, Human Resources

We’ve all been there – once or twice (or more)—when a child, spouse or family member has had to gain access to healthcare quickly. Whether a fall that requires stitches; a sprained or broken bone; or something more serious, it can be difficult to identify which avenue to take when it comes to walk-in care. With the recent boom in stand-alone ERs (Emergency Care Clinics or ECCs), as well as, Urgent Care Clinics (UCCs) it’s easy to see why almost 50% of diagnoses could have been treated for less money and time with the latter.

It’s key to educate yourself and your employees on the difference between the two so as not to get pummeled by high medical costs.

- Most Emergency Care facilities are open 24 hours a day; whereas Urgent Care may be open a maximum of 12 hours, extending into late evening. Both are staffed with a physician, nurse practitioners, and physician assistants, however, stand alone ECCs specialize in life-threatening conditions and injuries that require more advanced technology and highly trained medical personnel to diagnose and treat than a traditional Urgent Care clinic.

- Most individual ERs charge a higher price for the visit – generally 3-5 times higher than a normal Urgent Care visit would cost. The American Board of Emergency Medicine (ABEM) physicians’ bill at a higher rate than typical Family-Medicine trained Urgent Care physicians do (American Board of Family Medicine (ABFM). These bill rates are based on insurance CPT codes. For example, a trip to the neighborhood ER for strep throat may cost you more than a visit to a UC facility. Your co-insurance fee for a sprain or strain at the same location may cost you $150 in lieu of $40 at a traditional Urgent Care facility.

- Stand alone ER facilities may often be covered under your plan, but some of the “ancillary” services (just like visit rates) may be billed higher than Urgent Care facilities. At times, this has caused many “financial sticker shock” when they first see those medical bills. The New England Journal of Medicine indicates 1 of every 5 patients experience this sticker shock. In fact, 22% of the patients who went to an ECC covered by their insurance plan later found certain ancillary services were not covered, or covered for less. These services were out-of-network, therefore charged a higher fee for the same services offered in both facilities.

So, what can you and your employees do to make sure you don’t get duped into additional costs?

- Identify the difference between when you need urgent or emergency care.

- Know your insurance policy. Review the definition of terms and what portion your policy covers with regard to deductibles and co-pays for each of these facilities.

- Pay attention to detail. Understand key terms that define the difference between these two walk-in clinics. Most Emergency Care facilities operate as stand-alone ERs, which can further confuse patients when they need immediate care. If these centers, or their paperwork, has the word “emergency”, “emergency” or anything related to it, they’ll operate and bill like an ER with their services. Watch for clinics that offer both services in one place. Often, it’s very easy to disguise their practices as an Urgent Care facility, but again due to CPT codes and the medical boards they have the right to charge more. Read the fine print.

It’s beneficial as an employer to educate your employees on this difference, as the more they know – the lower the cost will be for the employer and employee come renewal time.