by admin | Feb 16, 2018 | Compliance, Human Resources, IRS

IRS Releases Publication 15 and W-4 Withholding Guidance for 2018

On January 31, 2018, the federal Internal Revenue Service (IRS) released Publication 15 — Introductory Material, which includes the following:

- 2018 federal income tax withholding tables.

- Exempt Form W-4.

- New information on:

- Withholding allowance.

- Withholding on supplemental wages.

- Backup withholding.

- Moving expense reimbursement.

- Social Security and Medicare tax for 2018.

- Disaster tax relief.

Read Publication 15 and further details here.

EEOC Penalty Increases for Failure to Post Required Notices

On January 18, 2018, the U.S. Equal Employment Opportunity Commission (EEOC) released a final rule increasing the penalty amount from $534 to $545 for violations of Title VII of the Civil Rights Act (Title VII), the Americans with Disabilities Act (ADA), and the Genetic Information Nondiscrimination Act (GINA) notice posting requirements.

The final rule is effective February 20, 2018.

Originally Published By ThinkHR.com

by admin | Feb 12, 2018 | Benefit Management, Compliance, Group Benefit Plans, Medicare

Do you offer health coverage to your employees? Does your group health plan cover outpatient prescription drugs? If so, federal law requires you to complete an online disclosure form every year with information about your plan’s drug coverage. You have 60 days from the start of your health plan year to complete the form. For instance, for a calendar-year health plan, this year’s deadline is March 1, 2018.

Background

The Centers for Medicare and Medicaid Services (CMS) is a federal agency that collects data and administers various federal programs. The agency utilizes the CMS online tool to collect information from employers about whether their group health plan’s prescription drug coverage is creditable or noncreditable. Creditable coverage means the group health plan’s prescription drug coverage is actuarially equivalent to Medicare’s Part D drug plans. In other words, the group plan is considered creditable if its drug benefits are as good as or better than Medicare’s benefits.

To confirm whether your plan provides creditable or noncreditable coverage, check with the plan’s carrier or HMO (if insured) or the plan’s actuary (if self-funded). CMS provides guidance to help plan sponsors, carriers, and actuaries determine the plan’s status.

Deadline for Disclosure

All group health plans that include any outpatient prescription drug benefits, regardless of whether the plan is insured, self-funded, grandfathered, or nongrandfathered, must complete the CMS disclosure requirement. There is no exception for small employers.

Complete the CMS online disclosure form every year within 60 days of the start of the plan year. For instance, for calendar-year plans, this year’s deadline is March 1, 2018.

Additionally, if your plan terminates or its status changes between creditable and noncreditable coverage, you must disclose the updated information to CMS within 30 days of the change.

Completing the Disclosure Form

The CMS online tool is the only method allowed for completing the required disclosure. From this link, follow the prompts to respond to a series of questions regarding the plan. The link is the same regardless of whether the employer’s plan provides creditable or noncreditable coverage.

The entire process usually takes only 5 or 10 minutes to complete. To save time, have the following information handy before you start filling in the form:

- Information about the plan sponsor (employer): Name, address, phone number, and federal Employer Identification Number (EIN).

- Number of prescription drug options offered (e.g., if employer offers two plan options with different benefit levels, the number is “2”).

- Creditable/Noncreditable Offer: Indicate whether all options are creditable or noncreditable or whether some are creditable and others are noncreditable.

- Plan year beginning and ending dates.

- Estimated number of plan participants eligible for Medicare (and how many are participants in the employer’s retiree health plan, if any).

- Date that the plan’s Notice of Creditable (or Noncreditable) Coverage was provided to participants.

- Name, title, and email address of the employer’s authorized individual completing the disclosure.

We suggest you print a copy of the completed disclosure to keep for your records.

Note: Employers that receive the Retiree Drug Subsidy (RDS), or sponsor health plans that contract directly with one or more Medicare Part D plans, should seek the advice of legal counsel regarding the applicable disclosure requirements.

Additional Disclosure Requirement

Separate from the CMS online disclosure requirement, employers also must distribute a disclosure notice to Medicare-eligible group health plan participants. The deadline for distributing the participant notice is October 14 of the preceding year. It often is difficult for employers to identify which employees and spouses may be Medicare-eligible, so most employers simply distribute the notice to all participants regardless of age or status. For information about the notice requirement, see our previous post.

Originally Published By ThinkHR.com

by admin | Feb 6, 2018 | Benefit Management, Employee Benefits, Group Benefit Plans

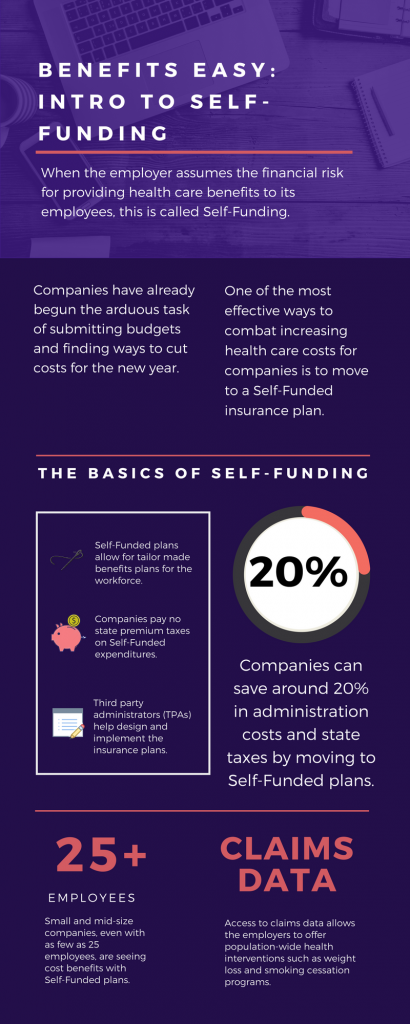

As we head into the second month of 2018, companies have already begun the arduous task of submitting budgets and finding ways to cut costs for the new year. One of the most effective ways to combat increasing health care costs for companies is to move to a Self-Funded insurance plan. By paying for claims out-of-pocket instead of paying a premium to an insurance carrier, companies can save around 20% in administration costs and state taxes. That’s quite a cost savings!

The topic of Self-Funding is huge and so we want to break it down into smaller bites for you to digest. This month we want to tackle a basic introduction to Self-Funding and in the coming months, we will cover the benefits, risks, and the stop-loss associated with this type of plan.

THE BASICS

- When the employer assumes the financial risk for providing health care benefits to its employees, this is called Self-Funding.

- Self-Funded plans allow the employer to tailor the benefits plan design to best suit their employees. Employers can look at the demographics of their workforce and decide which benefits would be most utilized as well as cut benefits that are forecasted to be underutilized.

- While previously most used by large companies, small and mid-sized companies, even with as few as 25 employees, are seeing cost benefits to moving to Self-Funded insurance plans.

- Companies pay no state premium taxes on self-funded expenditures. This savings is around 1.5% – 3/5% depending on in which state the company operates.

- Since employers are paying for claims, they have access to claims data. While keeping within HIPAA privacy guidelines, the employer can identify and reach out to employees with certain at-risk conditions (diabetes, heart disease, stroke) and offer assistance with combating these health concerns. This also allows greater population-wide health intervention like weight loss programs and smoking cessation assistance.

- Companies typically hire third-party administrators (TPA) to help design and administer the insurance plans. This allows greater control of the plan benefits and claims payments for the company.

As you can see, Self-Funding has many facets. It’s important to gather as much information as you can and weigh the benefits and risks of moving from a Fully-Funded plan for your company to a Self-Funded one. Doing your research and making the move to a Self-Funded plan could help you gain greater control over your healthcare costs and allow you to design an original plan that best fits your employees.

by admin | Jan 26, 2018 | Compliance, Human Resources

This is a reminder that from February 1 through April 30, 2018, impacted employers are required to post a copy of their 2017 Form 300A (Summary of Work-Related Illnesses and Injuries) in a common area where employee notices are usually available.

This annual requirement may not apply to certain employers that are partially exempt from routinely keeping Occupational Safety and Health Administration (OSHA) injury and illness reports. Partially exempt employers are those:

Partially exempt employers may have to maintain illness and injury reports at the request of OSHA, the Bureau of Labor Statistics (BLS), or a state agency operating under the authority of OSHA or the BLS. Additionally, pursuant to 29 CFR § 1904.39, all employers, even those that are partially exempt, must report to OSHA any workplace incident that results in a fatality, in-patient hospitalization, amputation, or loss of an eye.

Originally Published By ThinkHR.com

by admin | Jan 19, 2018 | Compliance, Human Resources, IRS

On January 2, 2018, the U.S. Department of Labor (DOL) published updated, inflation-adjusted penalties for violations of various laws regulated by the DOL and its internal components or divisions, including the Occupational Health and Safety Administration (OSHA). The DOL is required to adjust the level of civil monetary penalties for inflation by January 15 each year pursuant to the Federal Civil Penalties Inflation Adjustment Act of 1990, as amended by the Federal Civil Penalties Inflation Adjustment Act Improvements Act of 2015 (Inflation Adjustment Act).

Because of the Inflation Adjustment Act, rates for OSHA penalties have increased three times in the last 17 months (August 1, 2016, January 13, 2017, and January 2, 2018). Therefore, for violations occurring after November 2, 2015, the penalty amounts incurred by employers will depend on when the penalty is assessed, as follows:

- If the penalty was assessed after August 1, 2016 but on or before January 13, 2017, then the August 1, 2016 penalty level applies.

- If the penalty was assessed after January 13, 2017 but on or before January 2, 2018, then the January 13, 2017 penalty level applies.

- If the penalty was assessed after January 2, 2018, then the current penalty level applies.

The applicable January 2, 2018 penalty levels for violations of the Occupational Safety and Health Act of 1970 (OSH Act) are as follows:

- Willful violations: $9,239 – 129,936 (up from $9,054 – $126,749 after January 13, 2017 and $8,908 – $124,709 after August 1, 2016)

- Repeated violations: $129,936 (up from $126,749 after January 13, 2017 and $124,709 after August 1, 2016)

- Serious violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

- Other-than-serious violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

- Failure to correct violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

- Posting requirement violations: $12,934 (up from $12,675 after January 13, 2017 and $12,471 after August 1, 2016)

These increases apply to states with federal OSHA programs and states with OSHA-approved state plans. Violations occurring on or before November 2, 2015 are assessed at pre-August 1, 2016 levels.

Employers are encouraged to familiarize themselves with these increased penalties and consult counsel if they have questions about the penalty level applicable to a potential violation.

Originally Published By ThinkHR.com