Beginning in 2024, most employers obligated to report under the Affordable Care Act (ACA) must file returns electronically by March 31, 2024. Employers filing fewer than 10 returns a year are allowed to use paper filing. Since March 31 falls on a weekend, the deadline this year is April 1, 2024.

Applicable large employers (ALEs) and smaller employers with self-insured health plans are required to e-file Forms 1095-C or 1095-B, as well as the accompanying Forms 1094-C or 1094-B, using the IRS’ Affordable Care Act Information Returns (AIR) system. Employers can apply for a 30-day extension for filing these forms by submitting Form 8809 by the original due date.

2023 HEALTH SAVINGS ACCOUNT CONTRIBUTIONS AND CORRECTIONS

For employers offering a health savings account (HSA), contributions toward the 2023 HSA limits and corrections for the 2023 calendar year must be made by April 15, 2024. Employers and employees can contribute to HSAs and make adjustments until the tax filing deadline, which is typically the individual’s tax filing due date.

Contributions that exceed the annual allowed limit are subject to a 6% tax on the excess contribution. That tax is assessed each year that the excess funds and their earnings remain in the account. Additionally, excess contributions are taxed as income.

Remember that using HSA funds for non-qualified expenses can result in significant penalties. Individuals under age 65 who use HSA money for non-qualified expenses will face a 20% penalty and pay income taxes on the withdrawal. After age 65, HSA funds may be used for non-qualified expenses without incurring the 20% penalty, however the funds will be considered taxable income.

EMPLOYER CONSIDERATIONS

Employers should ensure that employees are aware of the annual contribution limits and the deadline for contribution adjustments, as well as potential tax penalties.

PREPARING FOR JUNE PRESCRIPTION DRUG DATA (RXDC) REPORTING

The third season of Prescription Drug Data Collection (RxDC) reporting is underway, with the annual deadline set for June 1 each year, reporting on the previous calendar year. The Consolidated Appropriations Act requires all group medical plans to file a report with the Centers for Medicare & Medicaid (CMS) detailing the cost and other medical data for the group health plans’ prescription drug and other benefits, excluding excepted benefits. RxDC reporting is mandatory regardless of the group’s insurance status, size, or whether it is a grandfathered plan.

The filing must be completed electronically through the CMS Enterprise Portal. While employers are ultimately responsible for RxDC filing, most third-party administrators (TPAs) pharmacy benefit managers (PBMs) contracted to provide services to the group health plan will assist or submit filings on behalf of the group health plan.

Changes for 2024 RxDC Reporting

The average monthly premium calculation has been simplified. Instead of calculating per member per month, this is stated as the total annual premium divided by 12.

CMS has introduced restrictions on data aggregation. Data in files D1 and D3 through D8 must match the level of detail in the D2 file. This means that if the D2 data is specific to an employer’s plan, the data in files D3 through D8 must be equally specific.

EMPLOYER CONSIDERATIONS

Insurance carriers will handle RxDC reporting on behalf of employers with fully insured plans. However, employers should confirm with carriers that the reporting has been completed and provide any necessary information.

Employers with self-insured plans have final responsibility for RxDC filing. If they rely on TPAs or PBMs to assist with filing, it’s crucial to ensure that it is completed on time.

NEW YORK CITY WORKERS ALLOWED TO SUE FOR SICK LEAVE VIOLATIONS

On March 20, the New York City Council enacted a provision allowing an individual to initiate a private legal action against employers for non-compliance with the Earned Safe and Sick Time Act (ESSTA).

Individuals may now file lawsuits for alleged violations of the Act directly in court, bypassing the need to file an administrative complaint with the Department of Consumer and Worker Protection. Legal action can be initiated within two years from the date the individual became aware or should have been aware of the alleged violation and may seek penalties, injunctive and declaratory relief, legal fees, costs, and other pertinent damages against the violating entity or individual.

Under the Act, the amount of safe and sick leave provided is contingent on the size of the employer.

Employers with 100 or more employees are required to provide up to 56 hours of paid leave annually.

Employers with 5 to 99 employees must offer up to 40 hours of paid leave annually.

Small employers with four or fewer employees and an annual net income exceeding $1 million are obligated to provide up to 40 hours of paid leave. In contrast, if the employer’s net income is less than $1 million, they are only required to offer up to 40 hours of unpaid leave annually.

Employers with one or more domestic workers must provide up to 40 hours of paid leave annually, with an increase to 56 hours for employers with 100 or more domestic workers.

Eligible employees are entitled to use accrued safe and sick leave immediately, including newly hired personnel. In cases of unforeseen leave, employers cannot mandate advance notice but can request documentation for absences exceeding three consecutive workdays. Employers must provide employees with written policy details regarding safe and sick leave, including information about accrued, utilized, and total leave balances, either on paystubs or via an accessible electronic system.

Significant amendments to the were implemented on October 15, 2023, to clarify the Act:

The assessment of an employer’s size is based on the total number of employees nationwide, determined by the peak number of concurrently employed staff within a calendar year.

Full time, part-time, joint employees, and employees on leave of absence are included in the employee count for determining employer size.

Employees telecommuting from outside New York City are not considered employed within the city.

Employees based outside of New York City that are “expected to regularly perform work in New York City during a calendar year” will be counted, but only for hours worked by the employee within New York City.

EMPLOYER CONSIDERATIONS

In light of these developments, it is imperative for New York City employers to thoroughly review their safe and sick leave policies to ensure full compliance and mitigate the risk of potential litigation.

QUESTION OF THE MONTH

Q: If an employee carries her full family on a qualified high deductible health plan (QHDHP) but her children are mandated to also be enrolled in Medicaid, can she contribute the full family amount to her health savings account (HSA)?

A: If the owner of the HSA (employee) is only eligible for the HDHP and the employee has enrolled in family coverage, the employee can contribute the full family limit to the HSA even if the employee’s dependents are not otherwise eligible due to Medicaid.

Answers to the Question of the Week are provided by Kutak Rock LLP. Kutak Rock provides general compliance guidance through the UBA Compliance Help Desk, which does not constitute legal advice or create an attorney-client relationship. Please consult your legal advisor for specific legal advice.

This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors.

In early February, a federal class action lawsuit was filed against Johnson & Johnson (JNJ) and its plan fiduciaries, alleging overpayment for prescription drugs within its prescription drug plan. The complaint alleges that under the Employee Retirement Income Security Act of 1974 (ERISA), JNJ’s plan fiduciaries are obligated to diligently compare service providers, seek cost-effective options, and monitor expenses. It is claimed that the plan fiduciaries failed to act prudently by agreeing to terms with a pharmacy benefit manager (PBM) that resulted in excessive costs for numerous drugs compared to other market options.

The lawsuit highlights the importance of transparency in facilitating comparisons between prescription drug prices across different plans or pharmacies and underscored significant risks faced by health and welfare plan fiduciaries. Publicly available information on drug prices enables individuals – including class action plaintiff attorneys – to scrutinize plan expenses, further emphasizing the need for prudent fiduciary actions.

EMPLOYER CONSIDERATIONS

Given the evolving landscape and heightened litigation risks, health plan fiduciaries should take proactive steps to mitigate litigation exposure and safeguard the interests of plan participants:

Establish a fiduciary committee dedicated to health and welfare benefits and delegate responsibilities accordingly.

Engage qualified consultants to assess PBMs and prescription drug arrangements, ensuring impartiality.

Review and negotiate terms of PBM agreements, fee structures, and formularies to ensure reasonability.

Collect and analyze benchmark information from various sources to evaluate vendor agreements.

Scrutinize compensation arrangements for reasonability and conflicts of interest.

Periodically solicit proposals from PBMs and vendors to reassess market competitiveness.

Document all policies, procedures, and decisions regarding vendor selection and performance monitoring to demonstrate procedural prudence.

UNITEDHEALTHCARE CYBERATTACK IMPACTS MILLIONS

Change Healthcare, a division of UnitedHealthcare’s Optum, was the target of a cyberattack resulting in significant disruptions to prescription orders at thousands of pharmacies nationwide. The impact in the U.S. has been profound, as parent company Optum provides services to more than 60,000 pharmacies and care for more than 100 million consumers.

While it works to recover, the company has isolated services related to billing, claims management, payment, and data exchanges, forcing some healthcare organizations and systems to revert to manual procedures. Full restoration of services remains pending. The American Hospital Association recommended that companies using Optum services temporarily disconnect from them.

Change Healthcare processes approximately 15 billion transactions annually, impacting a significant portion of U.S. patient records, including prescriptions, dental, clinical, and other medical needs. The disruption has led to difficulties in verifying patients’ insurance coverage for prescriptions, forcing some individuals to pay in cash. While larger pharmacy chains like Walgreens have reported limited effects, smaller pharmacies heavily reliant on Change Healthcare for insurance verification and billing services are facing significant challenges.

The attack highlights the vulnerability of healthcare data, especially patients’ private medical records, in the face of cyber threats. Federal officials are closely monitoring the situation, emphasizing the need to strengthen cybersecurity resilience across the healthcare ecosystem.

EMPLOYER CONSIDERATIONS

Given the ongoing disruptions and potential risks to data security, affected employers should:

Remain vigilant and communicate any updates or developments to enrollees.

Encourage employees to exercise caution regarding any unusual communications or activities related to prescription orders or insurance verification.

Stay informed about further updates from Change Healthcare and UnitedHealth Group regarding the restoration of services and any measures to enhance cybersecurity.

UPDATED INSTRUCTIONS RELEASED FOR JUNE 1 RXDC REPORTING

The No Surprises Act, as part of the Consolidated Appropriations Act, 2021 (CAA), requires employer-sponsored health plans to comply with annual prescription drug data collection (RxDC) reporting to provide transparency in prescription drug and health care spending. Data is reported to the U.S. Department of Labor (DOL), the Department of the Treasury (Treasury), and the Department of Health and Human Services (HHS) to monitor spending trends and facilitate regulatory control measures.

The reporting deadline for the 2023 reference year data is June 1, 2024. The Centers for Medicare & Medicaid Services (CMS) has issued revised instructions and templates for RxDC reporting. The instructions are mostly consistent with prior years; however, one significant change is the new enforcement of the “aggregation restriction” beginning with the 2023 reference year. The restrictions will limit the ability of plan sponsors to have their vendors report certain data on their behalf.

Additional changes in the instructions for the 2023 reference year reporting include prescription exclusions and simplified calculations.

Failure to comply with RxDC reporting requirements may result in penalties under Internal Revenue Code Section 4980D of $100 per day.

EMPLOYER CONSIDERATIONS

Ensure timely completion of the RxDC reporting for calendar year 2023 by June 1, 2024.

Confirm filing status with insurance carriers for fully insured plans or follow up with third party administrators (TPAs), pharmacy benefit managers (PBMs), or administrative services only providers (ASOs) for self-insured plans.

Provide necessary information requested by relevant parties for reporting.

Determine whether data should be reported on a plan level or aggregated basis.

Consider requesting pharmacy data reporting on a plan level basis to access detailed pharmacy benefit spend information.

2025 EMPLOYER SHARED RESPONSIBILITY PENALTIES

The IRS has released the 2025 employer shared responsibility payments under the Affordable Care Act (ACA). Applicable large employers (ALEs) may face penalties for failing to provide minimum essential coverage to 95% of full-time employees, or for offering coverage that is not affordable or does not meet minimum value. The adjusted penalty amounts for 2025 will be $2,900 per full-time employee for Penalty “A” (a $70 decrease from 2024) and $4,350 per full-time employee for Penalty “B” (a $110 decrease from 2024).

EMPLOYER CONSIDERATIONS

To avoid penalties, ALEs should consistently ensure full-time employees receive minimum essential coverage that meets affordability and minimum value standards. The IRS uses Letter 226-J to notify ALEs of potential penalties, with a response form included for ALEs to address proposed penalties. Employers and advisors should remain vigilant for this letter to promptly review and respond accordingly.

QUESTION OF THE MONTH

Q: What are the time and dollar limits for flexible spending arrangements (FSA) and FSA carryovers?

A: For 2024, the most that can be deferred to an FSA is $3,200 (a $150 increase from 2023). The amount of a 2024 FSA balance that can be carried over into 2025 is $640 (up from $610 in 2023). A carryover is only available if the FSA does not offer a grace period. The carryover amount can be used all year.

A grace period, on the other hand, is the amount of time in a new year that an employee can incur and be reimbursed for claims from the prior year’s balance. A grace period can be as long as 2 ½ months after the close of the plan year (usually the calendar year). So, if an employee has $1,000 left in the 2023 FSA, that employee could incur $1,000 of reimbursable expense prior to March 15, 2024, and spend that $1,000 if the FSA uses a grace period. An FSA cannot have both a grace period and a carryover.

And finally, most FSAs offer a run-out period. This is a period after the close of the plan year when employees can submit claims incurred in the prior year. There is no maximum run-out period set by the IRS, but most employers (or FSA administrators) will set a limit of 60 to 90 days. The run-out period only allows people to submit claims incurred in the prior year, unlike the grace period, which allows new claims incurred prior to March 15 to be reimbursed.

This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors.

The Affordable Care Act (ACA) Implementation FAQ Part 63, issued by the U.S. Departments of Labor, Health and Human Services, and the Treasury focuses on the Public Health Service Act, which mandates that non-grandfathered group health plans and health insurance issuers provide culturally and linguistically appropriate summaries of benefits and coverage (SBC) and claims and appeals notices.

The regulations stipulate accommodations for notices in counties where more than 10 percent of the population is literate only in a specific non-English language, as determined by American Community Survey (ACS) data. Plans and issuers must offer oral language services, provide notices in the relevant non-English language upon request, and include a statement in English notices indicating how to access language services (referred to as taglines).

Non-grandfathered group health plans and issuers must adhere to the guidance for plan or policy years beginning on or after January 1, 2025. This guidance ensures that the provision of SBC and claims and appeals notices aligns with cultural and linguistic competence standards.

Employer Considerations

Employers should be prepared to point out to applicable employees the tagline to access language services found in English language SBCs and notices.

REDUCED INSULIN PRICES FOR SOME

UnitedHealth’s pharmacy benefit manager unit, Optum Rx, announced the inclusion of eight insulin products in its reimbursement list, limiting out-of-pocket expenses to $35 or less for enrollees. These products, including short- and rapid-acting insulin from Eli Lilly, Novo Nordisk, and Sanofi will be moved to tier one, the preferred status with the lowest prices, effective January 1, 2024. The move is part of an effort by these major insulin manufacturers, who collectively control 90 percent of the U.S. insulin market, to reduce list prices by 70 to 78 percent this year or in 2024. The Biden administration and lawmakers have been urging insulin makers and pharmacy benefit managers to address the high prices of this crucial medication.

Employer Considerations

Employers should check their insurers’ Rx formulary as more carriers may follow suit to lower insulin prices. Self-funded plans may consider making this change to remain competitive with fully funded plans.

BLUECROSS BLUESHIELD MOVES INTO DIRECT CARE DELIVERY

In 2023, various BlueCross BlueShield (BCBS) plans underwent reorganization, engaging in corporate restructuring, mergers and acquisitions, or establishing subsidiaries focused on healthcare delivery to enhance competitiveness with larger insurers.

BCBS plans have been expanding their presence in healthcare delivery by opening medical clinics exclusively serving their members. In Washington, Premera Blue Cross collaborated with Kinwell Medical Group in 2022 to establish primary care clinics for its members. BCBS Arizona took a similar approach in 2023, launching Prosano Health Solutions, a new primary care subsidiary, with plans to address specific geographic areas in Arizona to improve access to care.

BCBS North Carolina recently announced its intention to acquire 55 North Carolina locations of FastMed, a national chain offering preventive, telehealth, occupational health, primary care, and urgent care services. This move is aimed at enhancing healthcare services, particularly in rural areas with limited access to resources.

Employer ConsiderationsEmployers covered by BCBS should ask their insurance broker whether the carrier provides a direct care option near them.

CALIFORNIA TAKES A STEP TOWARD SINGLE-PAYER SYSTEM

Governor Gavin Newsom signed Senate Bill 770, a significant step toward universal healthcare in California. The legislation directs the state’s Health and Human Services Agency to collaborate with the federal government to create a unified health financing system for all Californians. This move could pave the way for a single-payer system, covering every resident and funded by state and federal resources, including Medicaid and Medicare funds.

Senate Bill 770 aims to establish a uniform standard of healthcare accessible to all individuals, irrespective of factors such as age, income status, employment status, immigration status, and other variables. As California undergoes modifications in its Medi-Cal system, Michael Lighty, president of Healthy California Now, emphasizes that certain persisting issues can only be effectively addressed through comprehensive reforms across the entire healthcare system.

The law requires California’s health secretary to provide recommendations on crafting a federal waiver by June 1, 2024, potentially allowing the state to access federal financing for a universal healthcare system.

While the legislation faced opposition, including criticism from both the left and the right, it suggests an incremental approach to healthcare reform in California. The move aligns with Governor Newsom’s 2018 campaign promise of supporting a single-payer system. Despite the diverse opinions, the signing of SB 770 underscores California’s commitment to exploring avenues for achieving universal healthcare.

On November 9, 2023, Chicago replaced its existing paid sick leave ordinance with the Chicago Paid Leave and Paid Sick and Safe Leave ordinance, effective December 31, 2023. The new ordinance modifies the accrual system, allowing employees to earn one hour of paid sick leave plus one hour of paid leave for every 35 hours worked, with a yearly maximum of 40 hours of each. Employees can carry over 16 hours of accrued paid leave and 80 hours of accrued sick leave to the next benefit year. Alternatively, employers can front-load 40 hours of each at the start of each benefit year.

Unlike the prior ordinance, the new law mandates that accrued, unused leave be paid to employees upon termination or when no longer covered by the ordinance, subject to a phased approach based on employer size. Any excess leave beyond annual carryover limits is forfeited. New employees become eligible for paid sick leave after 30 days and paid leave after 90 days of employment. Paid leave can be used for any purpose, and employers cannot compel employees to disclose the reason.

Employer Considerations

Employers must comply with various notice and posting requirements, including providing written notice of the paid-time-off policy at the start of employment and before any changes. A 14-day notice of policy changes affecting final compensation must be given, and information about leave accrual and usage must be provided with each wage payment. Employers with Chicago-based employees should carefully review and adjust their sick leave and paid leave policies to align with the new ordinance, considering its differences from the previous paid sick leave ordinance and the upcoming statewide Paid Leave for All Workers Act.

QUESTION OF THE MONTH

Q: Can former employees who are on COBRA and paying monthly premiums to a TPA for COBRA deduct those premium amounts on their taxes? For example, if a person is on COBRA for three months in 2023, can they deduct COBRA premium payments from taxable income on their 2023 federal tax return?

A: Yes, COBRA premiums can be deducted on an individual’s federal income taxes provided they itemize their taxes and the person’s medical expenses (including COBRA premiums) exceed 7.5% of their adjusted gross income.

Answers to the Question of the Week are provided by Kutak Rock LLP. Kutak Rock provides general compliance guidance through the UBA Compliance Help Desk, which does not constitute legal advice or create an attorney-client relationship. Please consult your legal advisor for specific legal advice.

This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors.

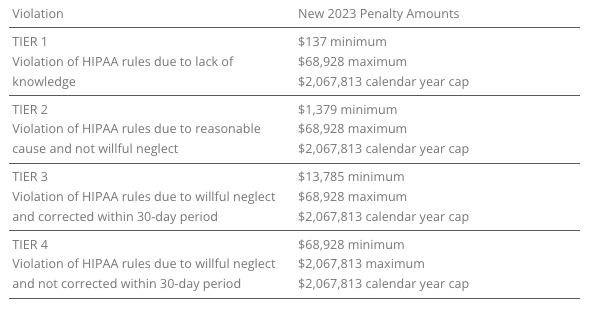

The U.S. Department of Health and Human Services (HHS) has recently announced adjustments to civil penalties related to violations of the Health Insurance Portability and Accountability Act (HIPAA), the Affordable Care Act (ACA), and the Medicare Secondary Payer (MSP) rules. These penalty adjustments take into account inflation and are applicable to violations that occurred on or after November 2, 2015, and for which penalties are assessed on or after October 6, 2023.

HIPAA, which focuses on privacy and security rules, categorizes penalties based on the level of intention behind the violation.

The maximum penalty for failing to provide an SBC to eligible individuals before enrollment (or re-enrollment) in a group health plan has increased from $1,264 to $1,362.

The Medicare Secondary Payer (MSP) rules prevent employers from providing incentives to Medicare beneficiaries to waive or terminate primary group health plan coverage. The maximum penalty for not complying with MSP rules has increased to $11,162 from $10,360. Furthermore, the maximum penalty for failing to inform HHS when a group health plan is or was primary to Medicare has risen to $1,428 from $1,325.

EMPLOYER CONSIDERATIONS

To avoid these penalties, employers should carefully review their plan documents and operations to ensure compliance with the HHS-related requirements.

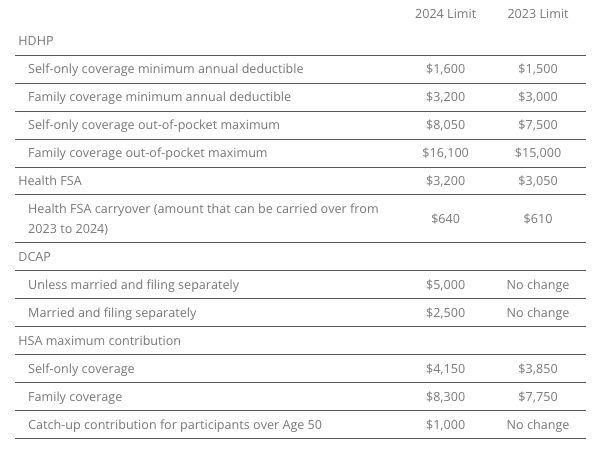

2023 LIMITS ANNOUNCED FOR HDHPS, HSAS, FSAS

The Internal Revenue Service (IRS) announced the new limits for high-deductible health plans (HDHPs), health savings accounts (HSAs), and Dependent Care Assistance Plans (DCAPs), and health flexible spending arrangements (FSAs). The new limits take effect beginning January 1, 2024.

MINNESOTA PAID SICK AND SAFE LEAVE LAW

Minnesota has recently passed a statewide paid sick and safe time leave law set to take effect on January 1, 2024. This law mirrors similar laws already in place in four Minnesota cities—Minneapolis, St. Paul, Duluth, and Bloomington. The key feature of the state law is the “front loading method,” which allows employers to provide employees with 48 hours of earned sick and safe time (ESST) in the first year of employment. Employers can pay out the value of unused hours at the end of the year and avoid carrying over unused hours into the next year.

EMPLOYER CONSIDERATIONS

This option provides flexibility for employers in managing employee leaves of absence. Local ordinances are not preempted by the state law, and employers must follow the most protective provisions of the state or local ordinances. The determination of which is more protective depends on whether more leave or monetary benefits are considered more beneficial for employees. See the FAQs for more information.

CALIFORNIA EXPANDS PAID SICK LEAVE

On October 4, 2023, Governor Gavin Newsom signed Senate Bill No. 616 into law, amending California’s paid sick leave regulations. The key changes introduced by SB 616 are:

Starting January 1, 2024, California employers must provide employees with five days or 40 hours of paid sick leave, an increase from the previous requirement of three days or 24 hours.

Employers can continue to provide paid sick leave at a rate of one hour for every 30 hours worked. If they use a different accrual rate, employees must accrue a minimum of 40 hours by their 200th day of employment and at least 24 hours by the 120th day of employment. Employers can also front load the entire paid sick leave amount.

Employers may still limit the annual use of paid sick leave, but SB 616 increases the annual usage cap from 24 hours to 40 hours. The bill allows employers to cap paid sick leave accrual at 80 hours or 10 days, up from the previous limit of 48 hours or six days.

While SB 616 continues to exempt certain collective bargaining agreement employees from the accrual requirement, it extends some provisions of California’s paid sick leave law to non-construction industry collective bargaining agreement employees. These employees may use paid sick leave for specific reasons, such as health-related issues or domestic violence, without facing retaliation. Employers cannot require these employees to find replacement workers when using sick days.

EMPLOYER CONSIDERATIONS

To comply with SB 616, employers are advised to review and update their paid sick leave policies to align with the new requirements and usage caps. Human resources and managers should also ensure proper implementation and adherence to the law.

QUESTION OF THE MONTH

Q: My wife and I work in the same small company. Is having her on my plan as spouse allowed? Can we both contribute separately from our own paychecks into our own Health Savings Account (HSA)? Or does it need to be my deduction only since I am the policy holder?

A: Yes, each spouse can have an HSA. The family limit, however, is divided between the two spouses, meaning the contributions to both HSAs combined cannot exceed the family HSA contribution limit.

Answers to the Question of the Week are provided by Kutak Rock LLP. Kutak Rock provides general compliance guidance through the UBA Compliance Help Desk, which does not constitute legal advice or create an attorney-client relationship. Please consult your legal advisor for specific legal advice.

This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors.

The IRS has announced a reduction in the Affordable Care Act (ACA) affordability percentage for plan years starting in 2024, lowering it from 9.12% in 2023 to 8.39%. This affordability percentage determines the maximum portion of an employee’s household income that can be spent on self-only coverage while still complying with the ACA’s affordability requirement. For applicable large employers (ALEs) with 50 or more full-time or full-time equivalent employees, this change means they must offer at least one health plan that does not exceed 8.39% of an employee’s household income for self-only coverage starting in 2024. This could necessitate adjustments to both employer and employee contributions to meet the new affordability standard. Employers have three safe harbors to determine if their health coverage is affordable under the ACA: Federal Poverty Level, Rate of Pay, or W-2 Wages. These safe harbors provide different methods for assessing affordability based on employees’ income, and employers can choose the one that best suits their situation. Non-compliance with ACA affordability requirements may lead to penalties for ALEs. Penalty A applies if an employer fails to offer minimum essential coverage to at least 95% of its full-time employees, while Penalty B applies when affordable, minimum value coverage is not offered to all full-time employees, and at least one employee receives a subsidy when enrolling in Marketplace coverage. The penalties for 2024 have been set, with Penalty A at $247.50 per month and Penalty B at $371.67 per month.

EMPLOYER CONSIDERATIONS

Employers should proactively work with their health plan broker or consultant to adapt to these changes in the 2024 ACA affordability percentage and avoid potential penalties while ensuring their employees have access to affordable health coverage.

UPDATED CHIP MODEL NOTICE RELEASED

The Department of Labor (DOL) has recently issued an updated model Employer CHIP Notice, through its Employee Benefits Security Administration (EBSA). This notice serves as a reminder of the annual notice requirement set forth by the Children’s Health Insurance Program Reauthorization Act of 2009 (CHIPRA). Employers who maintain group health plans in states offering premium assistance subsidies under Medicaid or Children’s Health Insurance Plans (CHIP) are obligated to provide this notice. Employers have the flexibility to deliver this notice independently or in conjunction with other materials, such as those related to health plan eligibility, open enrollment processes, or the summary plan description (SPD). The annual notice requirement applies to employers whose group health plans cover participants residing in states with premium assistance subsidies, regardless of the employer’s location. The DOL’s model notice, which employers can use for compliance, is periodically updated to align with changes in states offering premium assistance subsidies.

EMPLOYER CONSIDERATIONS

While employers have the option to create their own notices or customize the model notice, it is crucial to ensure that any notice provided includes at least the minimum state-specific contact information relevant to employees residing in states with premium assistance programs. Compliance with this requirement is essential for employers to inform their employees about the availability of these subsidies under CHIPRA.

PREPARING FOR MEDICAL LOSS RATIO REBATES

Employers with fully insured group health plans may receive a check from their insurance provider, known as a medical loss ratio (MLR) rebate. These rebates are aimed to ensure that a significant portion of the premiums paid by plan participants goes toward covering healthcare expenses and quality improvements, rather than the insurer’s administrative costs and profits. These rebates must be distributed by insurers annually, typically by September 30.

YOU CAN PREPARE NOW

While the checks are still forthcoming, employers can prepare now for the actions they will need to consider. The way employers can use the MLR rebate depends on how health coverage premiums are paid. If the employer covers 100% of the premiums for employees and their dependents, any rebate belongs to the employer to use as the employer sees fit. However, if participants contribute to the premiums, a portion of the rebate is considered “plan assets,” which must be used exclusively for the benefit of plan participants. Calculating the plan asset portion of the MLR rebate involves determining the percentage of total plan premiums assigned to employee contributions. This can be challenging, especially when employers offer various premium payment strategies. Nevertheless, it is crucial to accurately calculate and allocate the plan asset portion to remain compliant with regulations. Employers have a couple of options for using rebates considered plan assets: they can improve plan benefits or return the appropriate amount to plan participants. Improving benefits can be tricky due to the rebate’s often modest amount and uncertainty about future rebates. The more popular option is returning the rebate to participants, either as a cash payment or a temporary reduction in premium contributions. Tax considerations come into play depending on whether contributions were made on a pre-tax or after-tax basis. ERISA regulations require timely distribution of employee portions of the MLR rebate, typically within 90 days of receiving the rebate from the insurer. Decisions on how to allocate these rebates among participants are subject to fiduciary standards, ensuring that participants’ interests are served fairly and impartially. DOL guidance generally advises against distributing rebates to former plan participants due to administrative costs outweighing the rebate’s value.

EMPLOYER CONSIDERATIONS

Employers are not required to provide a specific notice about the MLR rebate to employees; instead, insurers are responsible for notifying plan participants. Employers may choose to communicate with participants to manage expectations regarding rebate amounts, as these are often relatively small on a per-participant basis. This communication can help avoid potential misunderstandings among employees.

PRESIDENT BIDEN ESTABLISHES OVERDOSE AWARENESS WEEK

A Proclamation released by President Biden addressed the nationwide crisis of drug overdose and barriers to treatment. The declaration addresses the impact untreated addiction has on millions of Americans, creating an urgent need for decisive action to combat the epidemic. “My Administration has worked hard to ensure that substance use disorder is treated like any other disease, funding the expansion of prevention, treatment, harm reduction, and recovery support services.” – President Biden The administration has implemented a National Drug Control Strategy targeting recovery support, along with making it easier for doctors to prescribe effective treatments, providing critical assistance to millions of Americans.

SICK LEAVE EXPANDS IN COLORADO

Colorado recently expanded the rights of employees to take paid time off. This expands the Colorado Healthy Families and Workplace Act (HFWA), which was originally created during the COVID-19 pandemic to ensure all employees in the state have access to paid sick leave, regardless of their job or employer size. Previously, the HFWA permitted employees to use paid sick leave for:

The employee’s inability to work due to a mental or physical illness, injury, or health condition.

The employee’s need to obtain preventive medical care or medical diagnosis, care, or treatment.

The employee’s needs due to domestic abuse, sexual assault, or criminal harassment, including medical attention, mental health care or other counseling, legal or other victim services, or relocation.

To care for a family member who needs the sort of care listed above.

The employee’s need for leave during a public health emergency when a public official closed the employee’s workplace or the school or place of care of the employee’s child.

Effective Aug. 7, 2023, Colorado employees may take paid leave for the following additional uses:

Bereavement or to handle the financial and legal needs arising after a death of a family member.

When an employee must evacuate their residence or care for a family member whose school or place of care was closed due to inclement weather, power/heat/water loss, or other unexpected event.

The HFWA requires that paid sick leave accrues over time, with at least one hour earned for every 30 hours worked, up to a minimum of 48 hours per year. Any unused hours can carry over to the next year. Employees must be paid their regular hourly rate when they take sick leave, and employers can ask for documentation only if an employee is absent for four or more consecutive workdays.

EMPLOYER CONSIDERATIONS

Employers must update their policies to include these new reasons for paid sick leave and inform their employees about their rights. Failure to do so may result in fines or liability for unpaid wages.

LEAVE LAWS EXPANDED IN ILLINOIS

The Illinois Victims’ Economic Security and Safety Act (VESSA) has recently undergone significant amendments aimed at expanding the leave provisions available to employees dealing with the aftermath of a family member’s death resulting from a crime of violence. VESSA is applicable to all employers in Illinois and mandates that they provide unpaid leave to employees who are victims of domestic, sexual, or gender violence, as well as those affected by crimes of violence, including their family or household members. Prior to these changes, VESSA allowed employees to take leave for various reasons related to violence, such as seeking medical attention, counseling, victim services, legal assistance, and safety planning. The new amendments to VESSA introduce three additional reasons for leave. Employees can now take time off to:

Attend the funeral or alternative service of a family or household member who was killed in a crime of violence.

Make necessary arrangements following the death.

Grieve the loss of a loved one due to a violent crime.

To substantiate their need for leave, employees can provide documentation such as a death certificate, obituary, or written verification from relevant authorities. The amount of VESSA leave an employee is entitled to varies based on the size of the employer. For the new, amended purposes related to deaths involving crimes of violence, employees are entitled to two workweeks (10 workdays) of unpaid leave, to be taken within 60 days after receiving notice of the victim’s death. This additional leave does not affect an employee’s entitlement to other qualifying VESSA leave during the same 12-month period.

EMPLOYER CONSIDERATIONS

VESSA overlaps with the Illinois Family Bereavement Leave Act (FBLA), which provides bereavement leave for eligible employees following the death of a covered family member. However, VESSA covers all Illinois employees, while FBLA is limited to those eligible for federal Family and Medical Leave Act (FMLA) leave.

QUESTION OF THE MONTH

Q: We have a group in Canada with both U.S. and Canadian employees. For COBRA eligibility purposes, do we count the Canadian employees with the U.S. employees? A: Yes, you must count the foreign employees with the U.S. employees of the same company for purposes of determining whether the employer is subject to COBRA.

About UBA United Benefit Advisors® (UBA) is the nation’s leading independent employee benefits advisory organization with more than 200 offices throughout the United States, Canada, and Europe. UBA empowers 2,000+ advisors to maintain independence while capitalizing on each other’s shared knowledge and market presence to provide best-in-class services and solutions.The content contained in this website, including but not limited to all text, images, trademarks, and logos, is owned by United Benefit Advisors® (UBA) except as otherwise expressly stated or provided by third parties. UBA Partner Firms must keep all copyright, trademark, and copy intact. All others may link directly to the UBA website to share UBA copyrighted material; they may not duplicate, distribute, create derivative works, or otherwise use this site’s content.

PROPOSED CHANGES TO SHORT-TERM, LIMITED-DURATION INSURANCE

On July 7, 2023, the U.S. Department of Health and Human Services (HHS), the Department of Labor (DOL), and the Department of the Treasury proposed changes to modify the definition of short-term, limited-duration insurance (STLDI) and the conditions for fixed indemnity insurance to be considered an excepted benefit. The proposal also asks for comments on specified disease plans and level-funded plans. The proposal looks to clarify the tax treatment of certain benefit payments under group health plans.

Short-term, limited-duration insurance is meant to fill temporary gaps in coverage during transitions. The proposal suggests limiting the initial contract period to no more than three months and the maximum coverage period to no more than four months, including renewals. This change aims to differentiate STLDI from comprehensive coverage and reduce financial risk for individuals using it as a long-term alternative.

The proposal also forbids the same issuer from issuing multiple STLDI policies to the same policyholder within a year (known as “stacking”). STLDI sales mainly occur through group trusts or associations, and the proposal clarifies that such sales are not group coverage for federal law purposes.

Fixed indemnity plans provide income replacement rather than full medical coverage. The proposed regulations look to clarify that this coverage should not pay benefits on a per-service basis, to avoid mimicking comprehensive coverage without providing the same consumer protections. The proposal also includes payment standards for fixed indemnity plans and clarifies that such coverage must be offered independently without coordination with other health plans.

Consumer notices would provide clearer information on the differences between STLDI, fixed indemnity excepted benefits coverage, and comprehensive coverage.

PCORI FEE PAYMENT

Plan sponsors of self-funded medical plans, including health reimbursement arrangements (HRAs), were required to report and pay fees to the Patient-Centered Outcomes Research Institute (PCORI) by July 31. This fee on group health plans was created through the 2010 Patient Protection and Affordable Care Act (ACA).

Research funded by PCORI concentrates on healthcare challenges faced by families every day, including cancer, diabetes, maternal mortality, opioid addiction, mental health, and equitable access to care, among many others.

If you believe you should have paid this fee, contact your broker for information, and access additional information including Form 720 for to submit the fee.

GROUP HEALTH PLANS ENCOURAGED TO EXPAND ENROLLMENT PERIOD FOR INDIVIDUALS LOSING MEDICAID AND CHIP

In a letter dated July 20, 2023, from the Center for Medicare and Medicaid Services (CMS) to employers, plan sponsors, and issuers, the Biden Administration encouraged these entities to offer additional enrollment opportunities in group health plans for employees and their dependents who are losing coverage under Medicaid.

The U.S. is experiencing a health coverage transition due to the COVID-19 pandemic. The pause on Medicaid coverage verifications and terminations ended on March 31, 2023, and state Medicaid agencies are now resuming regular eligibility and enrollment operations, which include renewing coverage for eligible individuals and terminating coverage for those no longer eligible.

According to a Department of Health & Human Services report, about 3.8 million individuals who lose Medicaid eligibility could be eligible for employment-based coverage. The Administration believes that many people may need more than the typical 60-day window after losing Medicaid or Children’s Health Insurance Program (CHIP) coverage to apply for and enroll in other coverage, especially considering the unique circumstances surrounding the resumption of Medicaid and CHIP renewals.

To address this concern, CMS has announced a temporary special enrollment period on HealthCare.gov. Marketplace-eligible individuals who lose Medicaid or CHIP coverage and come to HealthCare.gov between March 31, 2023, and July 31, 2024, will be able to enroll. Employers are encouraged to follow suit by expanding special enrollment periods for individuals losing Medicaid or CHIP coverage. These changes would require a plan amendment and approval from the insurance carrier.

Employers interested in sharing this with employees should provide information about Medicaid and CHIP renewals to employees and encourage them to update their contact information with their state agency, using CMS resources available at www.medicaid.gov/unwinding. Employers can voluntarily open enrollment in their employment-based plan for those losing Medicaid or CHIP coverage.

PROPOSED RULES MAY IMPACT MHPAEA AND NQTL DATA COLLECTION

On July 25, 2023, the U.S. Departments of Treasury, Labor, and Health and Human Services (the “Departments”) issued a comprehensive set of guidelines to help employers comply with the requirements of the Mental Health Parity and Addiction Equity Act (MHPAEA). The guidelines, including definitions and examples, emphasize the importance of access to mental health and substance abuse treatment, and data collection for the production of analysis reports.

A new rule focuses on networks having an adequate number of appropriate providers. Low reimbursement rates for behavioral health care providers compared to primary care providers negatively impact access to care. Plans must collect and analyze network adequacy data and provider reimbursement rates to address this issue.

The guidelines also establish specific content and delivery requirements for the non-quantitative treatment limitations (NQTL) comparative analysis and set minimum data collection standards. The Departments expressed dissatisfaction with the current state of plans compliance with the NQTL analysis requirements and aim to bridge the gap with the proposed regulations.

These regulations are still in the proposal stage, and incoming comments may lead to modifications. Employers should review the guidelines with their brokers, paying particular attention to their network providers, as access to mental health and substance abuse disorder care is a top priority.

QUESTION OF THE MONTH

Q: My staff count has been fluctuating around 50 for some time. How do I know if or when I need to offer health insurance to my employees?

A: Whether an employer is an applicable large employer (ALE) is determined each calendar year, and generally depends on the average size of an employer’s workforce during the prior year.

If an employer has fewer than 50 full-time employees, including full-time equivalent employees, on average during the prior year, the employer is not an ALE for the current calendar year and therefore not subject to the employer shared responsibility provisions or the reporting provisions for the current year.

If an employer has at least 50 full-time employees, including full-time equivalent employees, on average during the prior year, the employer is an ALE for the current calendar year, and is therefore subject to the employer shared responsibility provisions and the reporting provisions.

This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors.

AFFORDABLE CARE ACT INFORMATION REPORTING

AFFORDABLE CARE ACT INFORMATION REPORTING