by admin | Jul 10, 2023 | Human Resources

Artificial intelligence (AI) is creating a swirling sense of anxiety, depression, excitement, and joy all at once. Many people want to use AI to make their work easier, to become more efficient. However, they are also fearful that the robots may replace them.

Human Resources professionals have an obligation to prepare the workforce for a future in which AI is at the center. At the moment, the job requires calming people about their concerns and devising a clear and credible game plan for AI as tool and threat.

Recently, HR Exchange Network asked respondents on Terkel.io to share how they are working with their teams to understand AI’s role in the workplace. Here is what business and HR leaders had to say:

Create a Culture of Continuous Learning

“To prepare employees for the more extensive use of ChatGPT and other AI and automation tools that may replace some of their work, I focus on encouraging them to become lifelong learners.

I also intentionally use language about adaptation versus replacement, clarifying that my team’s jobs will evolve rather than disappear. I want to arm them with the skills they need to stay current in this ever-changing world.

For instance, I firmly believe in providing courses about advanced analytics, machine learning algorithms, and data science so employees can understand what is happening under the hood of new technology. This helps our team develop a better understanding of how these systems operate and may help them gain more meaningful roles as the development of artificial intelligence grows.”-Carly Hill, Operations Manager, Virtual Holiday Party

Integrate AI into Work Functions

“The extensive use of ChatGPT and other AI and automation tools is inevitable in the future of work. We, as a company, have been proactively preparing our employees through continuous learning and development programs.

We have integrated AI tools into our workflows to reduce manual workload and make operations more efficient. Our employees are encouraged to learn and explore these tools, and we have offered training sessions to upskill them on how to use AI tools and automation software.

We emphasize that AI and automation do not necessarily replace their job functions, but rather enhance their productivity and efficiency. We assure our employees that we are committed to their growth and will support them in adapting to the latest technologies to build a better future for our company.”-Jefferson McCall, Co-founder and HR Head, TechBullish

Use AI as a Tool

“We believe that the rise of AI and automation tools like ChatGPT represent an evolution of work rather than a replacement of human effort.

We make it clear to our employees that while AI is powerful, it doesn’t replace the unique human skills they bring to the table. Creativity, critical thinking, emotional intelligence, and nuanced understanding of complex issues are irreplaceable human strengths.

We’re also investing in training programs to help our employees understand and work alongside AI tools. The goal is to upskill our workforce, enabling them to use AI to augment their capabilities and improve productivity, rather than viewing it as a threat.

We see AI as a tool that can take over routine tasks, thereby freeing up our team members to focus on more complex, creative, and strategic aspects of their roles.”-Bowen Khong, CEO, GameDayr

Use AI to Enhance Efficiency

“We are training our employees to use ChatGPT and other AI and automation tools and to take advantage of these new technologies to increase their productivity. We are emphasizing to employees that these tools represent an opportunity to do more meaningful work and to improve their skills.

We are also emphasizing that these tools are not a replacement for employees, but rather an enhancement that can help them be more successful in their roles.”-Ranee Zhang, VP of Growth, Airgram

Be Honest: Robots Will Replace Some

“To prepare for the possible effects of AI and automation on their workforce, businesses should anticipate potential job losses because of automation and develop strategies for relocating affected workers.

To help workers adjust to shifting work requirements and schedules, businesses can consider offering alternatives like job sharing, flexible schedules, and remote work.

However, AI might also be investigated for its potential to supplement and improve the job of existing employees rather than replace them.

Data research, AI development, and automation engineering are just a few of the fields where AI is spawning new employment opportunities. These positions call for expertise in great demand, yet may be hard to fill.”-Aleksandar Ginovski, Career Expert, Resume Expert, and Product Manager, Enhancv

Consider Tools to Simplify AI

“While we are preparing our team for the inevitable integration of ChatGPT’s AI, we also want them to understand that companies are bringing out easier-to-use tools that make ChatGPT significantly easier to use.

Right now, many of those tools are glitchy and not all that helpful, but some are proving to be extremely powerful. So at our company, we are paying attention to the integration tools as much as the AI.”-Jason Vaught, Director of Content, SmashBrand

Embrace Artificial Intelligence

“For years, I have said to my students and employees to embrace technology and keep up with it. I have seen the difference that being tech-savvy (and the efficiency that comes with it) makes in hiring and layoff selections.

ChatGPT, AI, and automation are fascinating to me, not just for what they do but for the conflicting emotions they bring—fear and excitement. I see them more as how they help us leverage the unique skills our employees bring and let these tools enable us in our work. I contend that a core competency for the future of employees’ work will (it already does) require and demand a mindset for change.

Taking a less fatalistic view of technology, understanding and learning how it can help us, and using it helps diminish that anxiety, helps employees learn the technology, and start or continue their journey to embrace it.”-Patty Hickok, SPHR, GPHR, SHRM-SCP, Sr. Director Employee Relations, HRIS and HR Operations, NANA Regional Corporation

Be Transparent

“If you’re establishing a position for AI in your workplace, then it’s important that you let your employees know about AI and how it could affect their current positions. This is especially important for older employees who might need to be more adaptable to this type of technology.

Talk to your employees about the fact that AI and the range of automation tools are here to stay—and it’s only going to get bigger in the future. If your employees may find their positions at risk in the long run, tell them and be honest. This would allow employees to make important decisions, such as whether they want to stay in the career path they are in right now or rather want to move to a different career line.

At the same time, empower employees and show them how AI can be used alongside them in the workplace.-Joe Flanagan, Founder, 90s Fashion World

Stay on the Cutting Edge

“While AI and automation can replace some marketing tasks, they will not replace marketing employees altogether. Instead, AI and automation will free up marketing employees to focus on more creative and strategic tasks.

We are working on educating employees about the benefits of AI and automation. AI and automation can help marketing employees to be more productive, efficient, and effective.

Then, we move to help employees develop new skills. As AI and automation take over some marketing tasks, employees will need to develop new skills to stay relevant in the workforce. Some skills that will be in high demand include data analysis, creativity, and strategic thinking.

And finally, we are creating a culture of continuous learning. The marketing landscape is constantly changing, so creating a culture of continuous learning within your organization is important. This will help employees to stay up-to-date on the latest trends and technologies.”-Brenton Thomas, CEO, Twibi

Get Smarter with AI

“In the SEO industry, we’re preparing for AI tools like ChatGPT by integrating AI literacy into our training programs. Our teams are learning to use AI for deeper keyword research, smarter content optimization, and predictive SEO analytics.

We also encourage employees to develop soft skills like strategic thinking and creativity, which are vital in interpreting and leveraging AI-driven insights.”-Jaya Iyer, Marketing Assistant, Teranga Digital Marketing

Embrace Humanity

“I think it’s important that we don’t frame AI as the enemy; rather, it is going to be helpful across all industries and help with all sorts of tasks. But AI will not replace the human experience, and we need to set the understanding with employees that at the end of the day, AI can help increase the greater good in a business setting.

Given the value ChatGPT has already brought, AI will continue to present itself as intelligence that can be used universally. Rather than creating stigmas, managers should be continuously trying to answer the question: ‘What can AI do to help my current business processes, and how can my employees make AI-driven processes the best they can be?'”.-Ryan Igo, Revenue Marketing Manager, Surety Systems

Think of AI as an Ally

“Our message is clear: AI is not here to replace our employees but to assist and enhance their work. We emphasize that staying ahead means embracing these advancements. We encourage employees to view AI as a powerful ally that can streamline tasks and create new opportunities for growth and innovation.

By fostering a culture of continuous learning and reskilling, we empower employees to harness AI’s potential while emphasizing the irreplaceable value of their unique skills, creativity, empathy, and problem-solving abilities.”-Marco Genaro Palma, Co-founder, TechNews180

By Francesca DiMeglio

Originally posted on HR Exchange Network

by admin | Jun 27, 2023 | Hot Topics, Human Resources

Workers want higher pay, more flexibility, and support from employers, according to ADP’s People at Work 2023 survey. HR professionals can compare the results with their own responses in the most recent HR Exchange Network State of HR report.

Specifically, more than 40% of employees said they are underpaid. The most satisfied employees were those with a hybrid schedule, and the least satisfied were those who worked exclusively in-person. About 47% of respondents said that their work is suffering because of their poor mental health, and about 65% said stress impacts their work.

Recently, ADP Chief Economist Nela Richardson sat down with HR Exchange Network to provide insight into worker’s needs during this fraught time in history, when organizations are simultaneously facing a labor shortage and a possible looming recession.

Important Takeaways about What Employees Want

HREN: What are the biggest takeaways from your study?

I think there are a couple of really good takeaways. We’ve been asking people [questions] for this work study for three years, and we’ve seen some amazingly impactful results from the pandemic.

The first takeaway is that the trends we’re seeing are starting to stabilize. When we first did this research after the pandemic, the global workforce was really shaken up. You had one-quarter of folks who had lost their jobs or were furloughed, people taking pay cuts, they saw their hours reduced, they saw their friends leave the company, they were given more responsibilities than they had before just to fill in those gaps.

Many of them reported that they took on more responsibilities without an increase in pay. Add on top of that the fact that there’s a global pandemic happening, and it is affecting your friends, your family and yourself. Still, they were optimistic, according to the first survey in 2021. They said that they thought that there could be a silver lining in the pandemic in terms of flexibility, and the chance for career progression.

Let’s fast forward three years, and that’s where we are. The global workforce is really focused on career progression. In the United States, the need for flexibility has stabilized and has been cemented. It’s what people want here. In the rest of the world, we saw progression dominate flexibility. Last year, we saw flexibility dominating career progression globally. In the United States, flexibility is still a big, big deal.

We found in the survey that the happiest workers are the ones who can get that hybrid schedule. It’s not that people want to be fully remote. They really care about flexibility and hours. And they care more about that than flexibility of where they work. That was true last year; it’s true this year.

We’re also seeing people want a caring workforce still. There was a lot of movement in the corporate sector in response to the murder of George Floyd that everyone watched. That seems so long ago, but it had an impact on corporate response, a bigger impact than any singular event people can point to. Much of that response was tied to diversity and inclusion. What the global workforce says is that they don’t want those things to disappear.

Now that the labor market is stabilizing, they want that stuff. Oh, and yeah, they want to get paid like they got paid last year. Many families are battling inflation. They earned about a 6.3% raise in the United States last year. They’re thinking about having about the same raise this year, so the expectations are high in 2023.

Future of Work

HREN: What do you think all this means for the future of work? What’s coming next?

There’s some good news. I think we are experiencing the stabilization of worker priorities. Last year, we were talking a lot about the Great Resignation. That is starting to stabilize but stabilized doesn’t mean go back to normal. Stabilize means reset at a different rate.

The expectation, even as we’re heading into a softer economy, is that peak workers are more likely to come and go than before. With remote and hybrid options, it’s easier to change jobs, it’s also easier to come back to jobs. You should negotiate that exit interview, so it does not feel quite so permanent. How do you engage people who may come back to you in two to three years? That should be the mindset of the HR manager these days. It’s a revolving door, not an exit door.

With these expectations around pay so high, there are creative things that companies are going to do in the future. Maybe people will be willing to pay for vacation days to get more flexibility. Or they will take a pay cut if it means that they have a little more autonomy in their schedule. There are other things that caring corporate culture can do in lieu of pay to get an engaged workforce. The great thing about the pandemic is it forced innovation. It’s important to keep innovating, keep evolving, and keep learning from your workforce and incorporating that in your process.

If people are starting to lean more into career progression, how do companies meet that need, especially when you think about the other trends that are going on like AI and tech? What are the skills needed for the future? Those in the workforce think that they just need people management skills. The workforce isn’t always spot on. We have to make sure that the workforce is aligned with corporate objectives, too.

What comes out of our study is that when people look at future-proof industries, they look to tech. If used correctly, AI can be inclusive. It can actually expand and it has. If you think about the way we’re communicating now, it expands your ability to interact with others, and it could get some sideline workers back into the labor market during a period of labor shortage. It doesn’t require the physical demands that keep people on the sidelines. There’s a way to be inclusive with all these technologies, and it’s really the corporate sector that can set the tone for how they’re used.

By Francesca Di Meglio

Originally posted on HR Exchange Network

by admin | Jun 22, 2023 | Compliance

CLAIMS SUBSTANTIATION FOR PAYMENT OR REIMBURSEMENT OF MEDICAL AND DEPENDENT CARE EXPENSES

A memorandum released by the IRS Chief Counsel responds to a request for assistance regarding the reimbursement of medical and dependent care expenses. Addressed is whether reimbursements of medical expenses from a health flexible spending arrangement (FSA) provided in a cafeteria plan should be included in an employee’s gross income if the expenses are not properly substantiated. The conclusion is that if any expenses, including those below a certain threshold, are not substantiated, the reimbursements must be included in the employee’s gross income.

The second issue concerns the method of substantiation for expenses. The document examines different scenarios, such as self-certification, sampling of expenses, not requiring substantiation for small amounts, and not requiring substantiation for charges with favored providers. The conclusion is that if a cafeteria plan does not require proper substantiation, it fails to operate in accordance with the regulations and the benefits must be included in the employee’s gross income.

Read the full description of the scenarios, an analysis of the relevant laws and regulations on income tax withholding and the regulations for cafeteria plans and substantiation of expenses.

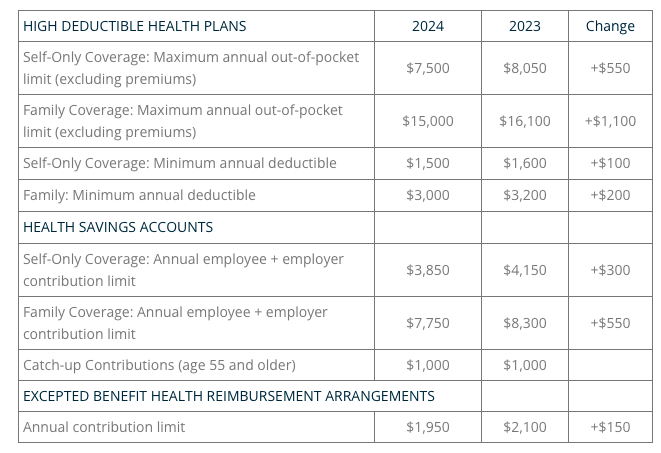

2024 LIMITS ANNOUNCED FOR HDHPS, HSAS, AND EXCEPTED BENEFIT HRAS

The Internal Revenue Service (IRS) announced the new limits for high-deductible health plans (HDHPs), health savings accounts (HSAs), and excepted benefit health reimbursement arrangements (EBHRAs).

The new limits for both HDHPs and HSAs will go into effect for calendar year 2024 while the HRA limits will go into effect for plan years beginning in 2024.

PREVENTIVE HEALTH SERVICES COVERAGE AND THE BRAIDWOOD DECISION

On May 15, 2023, the Fifth Circuit Court of Appeals temporarily halted the enforcement of a district court’s ruling in the Braidwood Management Inc. v. Becerra case. The district court had invalidated a portion of the Affordable Care Act (ACA) that required coverage of certain preventive care services without cost-sharing, citing religious beliefs as the reason for the violation. The Justice Department appealed the decision, and while the appeal is ongoing, the Fifth Circuit issued an administrative stay, effectively reinstating the ACA’s requirement for full coverage of preventive care. A final decision from the Fifth Circuit is expected later this year.

The Braidwood decision concluded that the determination of certain preventive care requirements under the ACA violated the Appointments Clause of the United States Constitution. These requirements are typically based on recommendations from entities such as the United States Preventive Services Task Force (USPSTF) and the Health Resources and Services Administration (HRSA). However, the court’s ruling specifically targeted recommendations made by the USPSTF after March 23, 2010.

The Departments of Labor, Health and Human Services, and the Treasury, responsible for enforcing the preventive service coverage requirements, have appealed the court’s decision. The Departments have issued an FAQ clarifying the impact of the Braidwood ruling, stating that it only applies to services recommended by the USPSTF after March 23, 2010, and does not affect guidance related to immunizations recommended by the Advisory Committee on Immunization Practices (ACIP) or comprehensive guidance supported by the HRSA. State laws may still require coverage of USPSTF-recommended services.

Although the Braidwood decision suspends the enforcement of certain preventive care coverage, it is expected that few employers will make significant changes until the outcome of the case is determined through the appeals process.

QUESTION OF THE MONTH

Q: Throughout the pandemic, our company’s group health plan has covered COVID-19 testing and vaccines at no cost to plan participants. Is this still required now that the public health emergency has ended?

A: During the COVID-19 public health emergency (PHE), group health plans had to cover COVID-19 testing and vaccines without cost-sharing or restrictions. Coverage requirements for diagnostic testing no longer apply after the PHE, but plans are encouraged to continue providing coverage at no cost. However, plans may choose not to cover tests or impose cost-sharing. The requirement to cover COVID-19 vaccines as a preventive service remains in effect for non-grandfathered health plans, but coverage for out-of-network providers is no longer mandatory if there is an in-network option. Plans are encouraged to notify participants of any changes to COVID-related coverage, and modifications must be disclosed at least 60 days in advance, except for changes that revert to pre-PHE conditions.

© UBA. All rights reserved.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. |

by admin | Jun 12, 2023 | Employee Benefits

As much as employers might prefer that employees’ personal affairs do not interfere with their work, the reality is that problems outside of the workplace can and do impact job performance. Many of these issues go unaddressed due to fear of stigmatization, leading to further declines in employee health and productivity. Anxiety and stress, financial troubles, substance abuse and other personal problems can also lead to increased absenteeism. To help combat these issues, many employers offer a workplace benefit called an Employee Assistance Program (EAP) that is designed to help employees address everyday challenges.

What is an EAP?

An EAP provides voluntary, confidential services to employees who need help managing personal difficulties or life challenges. The idea is to address personal issues before they interfere with work performance. The employee assistance program is one of the top benefits employers offer in America—for a good reason. They are one way that companies support the well-being of their employees. An EAP generally offers confidential assessment, short-term counseling, referrals and follow-up services for employees.

Typically, an EAP grants employees access to a set number of sessions with a therapist, and the employee would not accrue any co-pay, deductible, or other out-of-pocket costs for the service. For example, Nick has been struggling with depression. To sooth his anxiety, he has begun drinking every day. It’s gradually escalated to the point where he is late to work, has frequent absences, and is missing deadlines. He knows he needs to talk with someone who can offer him alcohol abuse resources. He accesses his company-sponsored EAP.

Meredith is a full-time, married employee with two small children and is also caring for her aging mother who suffers from Alzheimer’s. She is constantly stressed due to the heavy burden of her daily life. The schedule has left her exhausted and she misses work each month due to feeling burnt out. She reaches out to her EAP counselor for time management and mental health tips.

Here are some other common services included in EAPs:

One reason behind the popularity of EAPs is that it’s a mutually beneficial program for employers and employees. After all, your employees are the foundation of your company. Healthy and happy employees are more productive and engaged in their jobs which is great for your company’s bottom line!