by admin | Aug 15, 2023 | Health Insurance

Health insurance may not be the most exciting thing to shop for but it’s one of the most important things that you can buy for yourself and for your family. Having health insurance has many benefits. It protects you and your family from financial loss in the same way that home or car insurance does. Even if you are in good health, you never know when you might have an accident or get sick.

Here are some key advantages of having health insurance:

- Access to Medical Care: Health insurance provides you with access to a network of healthcare providers, hospitals, and specialists. It ensures that you can receive timely medical attention when needed, promoting early diagnosis and treatment.

- Financial Protection: One of the most significant benefits of health insurance is the financial protection it provides. Medical expenses can be substantial, especially in the case of major illnesses, surgeries, or emergencies. Health insurance helps mitigate these costs, preventing individuals from facing overwhelming medical bills and potential debt.

- Preventive Care: Health insurance plans cover preventive services at no cost if you use an in-network provider. This includes routine check-ups, vaccinations, screenings, and counseling services.

- Coverage for Essential Health Services: Health insurance plans typically cover essential health services, such as hospitalization, emergency care, prescription drugs, maternity care, mental health services, and rehabilitation.

- Health and Wellness Programs: Some health insurance plans offer additional benefits such as wellness programs, gym memberships, and access to health management tools. These initiatives encourage you to adopt a healthier lifestyle, manage chronic conditions, and take proactive steps towards improving your overall well-being.

- Specialist Care and Treatment: Health insurance often covers specialized medical care, including consultations with specialists, diagnostic tests, and treatments. Having access to specialists can be crucial for managing complex or chronic conditions effectively.

- Family Coverage: Health insurance plans often provide coverage for family members, including spouses and dependent children.

- Peace of Mind: Knowing that you have health insurance can bring peace of mind, reducing stress and anxiety about potential medical expenses. It allows you to focus on your health and recovery without the added burden of worrying about the financial implications.

Your health is your most valued asset. With a good health insurance plan, you help protect the health and financial future of yourself and your family for a lifetime. It’s important to note that the specific benefits and coverage may vary depending on the health insurance plan, provider, and local regulations. Make sure to review and understand the terms and conditions of a health insurance policy before enrolling.

by admin | Aug 7, 2023 | Human Resources

Gallup recently sounded the alarm on the employee engagement crisis. A survey revealed that nearly 60% of 120,000 of the world’s workers are quiet quitting or not engaging, and 18% are actively disengaged, which Gallup labeled as loud quitting.

This is a surprise to the public, but Human Resources professionals saw this coming. In the State of HR survey, they listed employee engagement as their number one priority and burnout as the biggest challenge. In 2022, employees had returned to pre-pandemic levels of engagement before media attention turned to quiet quitting. This was a phrase used to describe people setting boundaries with their employees, sticking to a fixed schedule, and meeting requirements of their job without going above and beyond.

What Is Loud Quitting?

In the early days of quiet quitting, many in HR rolled their eyes because this was nothing new and workers have a right to set boundaries. Not everyone has to be ambitious. Sometimes, it’s just about fulfilling basic duties to earn that paycheck.

Loud quitting is distinctly different. It’s akin to burning bridges, which HR Exchange Network does not recommend in any instance. Workers simply don’t know if their paths will ever cross with these employers, HR professionals, or colleagues again. It breeds a lack of trust and can mar one’s reputation. Gallup uses this definition to describe loud quitting:

“These employees take actions that directly harm the organization, undercutting its goals and opposing its leaders. At some point along the way, the trust between employee and employer was severely broken. Or the employee has been woefully mismatched to a role, causing constant crises.”

This is a serious charge. At a time when the world is grappling with an uncertain economy, and the World Bank warned that businesses may be facing a decade of decline without economic growth, this news is even more disturbing. After all, Gallup estimates that low engagement costs the global economy $8.8 trillion and accounts for 9% of global GDP. Imagine how that plays out in one company.

How Should HR Respond?

Human Resources must pay close attention to employee engagement and experience. This is a challenging time for everyone. People are experiencing anxiety that lingers from the pandemic and is exacerbated by financial concerns. In addition, many companies, especially in the tech sector, are conducting layoffs, hiring freezes, budget cuts, and restructuring. This means those who are still employed are taking on more work, which can lead to feeling overwhelmed at best and burnout at worst.

ADMIT YOU HAVE A PROBLEM

Human Resources must be attentive to what’s happening with employees. Using feedback surveys allows HR to hear from workers and recognize if there are problems. However, even without feedback surveys, HR professionals can use their eyes and ears to recognize if people are being overworked, having issues with managers and colleagues, or simply checking out.

MAINTAIN FOCUS ON MENTAL HEALTH AND WELLNESS

In the Gallup survey, 44% of workers said they experienced a lot of stress the previous day. The circumstances of work today by themselves are causing anxiety. Therefore, mental health and wellness benefits must remain a priority. Employees have come to expect companies to show their care and concern by providing them with the means to tend to their physical and mental health. When employers are asking people to do more with less, they should be prepared to help them deal with the consequences.

KEEP AN EYE ON DEI EFFORTS

In the last year, diversity and inclusion programs have taken a hit. Employers laid off DEI leaders or cut resources. But DEI is vital to employee engagement. Providing people with that sense of belonging and making them feel heard and valued, which are all part of any decent DEI program, are essential to keeping people engaged.

HELP MANAGERS BE BETTER

Many in HR have said, “People quit managers, not jobs!” This mantra is often said because it is true. In fact, Gallup suggests that HR address this engagement crisis by focusing on top talent and giving them better managers. The fact is that HR has been asking much of managers these days.

In addition to ensure tasks get done, projects are completed, and results improve, they also must show empathy, help people with their wellness and well-being, and encourage a culture of inclusiveness. These are not easy tasks, and many never get training or help meeting these goals. Training managers on both hard and soft skills prepares them for the new expectations of employees and positions them to garner more engagement.

By Francesca Di Meglio

Originally posted on HR Exchange Network

by admin | Aug 1, 2023 | Employee Benefits, Hot Topics

- Fertility Treatments Coverage: Fertility treatments, such as in vitro fertilization (IVF) or intrauterine insemination (IUI), can be expensive and may not be covered by traditional health insurance plans. Fertility treatment coverage can help employees overcome financial barriers and access the fertility treatments they need to start or expand their families.

- Egg Freezing: Egg freezing allows individuals to preserve their eggs for future use. This can be particularly beneficial for employees who want to delay starting a family due to personal or professional reasons.

- Fertility Preservation: Some medical treatments, such as chemotherapy or radiation therapy, can have a negative impact on fertility. Fertility preservation options, such as freezing embryos or sperm freezing, can help individuals protect their fertility before undergoing such treatments.

- Adoption Assistance: In addition to fertility treatments, companies are expanding their benefits to include adoption assistance programs. These programs can provide financial support, counseling services, and resources to employees who are going through the adoption process. By offering adoption assistance, employers show their commitment to supporting various pathways to parenthood and promoting inclusivity.

- Fertility Education and Support: Many employers are going beyond financial coverage and offering educational resources and support for employees navigating fertility challenges. This can include access to fertility experts, educational seminars, counseling services, and fertility wellness programs.

Since fertility coverage is relatively new, fertility benefits can vary greatly. However, essentially there are two options for coverage:

- Cover specific treatments under their health plan

- Offer to pay a portion of treatment costs as a voluntary benefit

Employee expectations around benefits and workplace support have evolved in step with the growing desire for fertility and family-forming benefits. By offering emerging fertility benefits, employers demonstrate their commitment to supporting employees’ family-building journeys and recognizing the diverse needs of their workforce. These benefits can enhance employee satisfaction, improve work-life balance, and contribute to a more supportive workplace culture.

Did you know that in 2017 the American Medical Association and the World Health Organization recognized infertility as a disease? Approximately 17.5% – roughly one in six couples– are affected by infertility in the U.S.

As societal norms and employee expectations continue to evolve, companies are recognizing the importance of offering comprehensive benefits packages that cater to the needs of their workforce. One area that has gained attention in recent years is fertility benefits. Here’s an overview of emerging fertility benefits and their significance:

- Fertility Treatments Coverage: Fertility treatments, such as in vitro fertilization (IVF) or intrauterine insemination (IUI), can be expensive and may not be covered by traditional health insurance plans. Fertility treatment coverage can help employees overcome financial barriers and access the fertility treatments they need to start or expand their families.

- Egg Freezing: Egg freezing allows individuals to preserve their eggs for future use. This can be particularly beneficial for employees who want to delay starting a family due to personal or professional reasons.

- Fertility Preservation: Some medical treatments, such as chemotherapy or radiation therapy, can have a negative impact on fertility. Fertility preservation options, such as freezing embryos or sperm freezing, can help individuals protect their fertility before undergoing such treatments.

- Adoption Assistance: In addition to fertility treatments, companies are expanding their benefits to include adoption assistance programs. These programs can provide financial support, counseling services, and resources to employees who are going through the adoption process. By offering adoption assistance, employers show their commitment to supporting various pathways to parenthood and promoting inclusivity.

- Fertility Education and Support: Many employers are going beyond financial coverage and offering educational resources and support for employees navigating fertility challenges. This can include access to fertility experts, educational seminars, counseling services, and fertility wellness programs.

Since fertility coverage is relatively new, fertility benefits can vary greatly. However, essentially there are two options for coverage:

- Cover specific treatments under their health plan

- Offer to pay a portion of treatment costs as a voluntary benefit

Employee expectations around benefits and workplace support have evolved in step with the growing desire for fertility and family-forming benefits. By offering emerging fertility benefits, employers demonstrate their commitment to supporting employees’ family-building journeys and recognizing the diverse needs of their workforce. These benefits can enhance employee satisfaction, improve work-life balance, and contribute to a more supportive workplace culture.

by admin | Jul 26, 2023 | Compliance

PCORI FEE DUE DATE APPROACHES

Employers offering self-funded medical plans, including health reimbursement arrangements (HRAs) must report and pay fees to the Patient-Centered Outcomes Research Institute (PCORI) by July 31. If the plan was fully insured, employers can rely on their insurance carriers to handle the fee payment.

The current annual fees are:

- For plan years that end on or after Oct. 1, 2021, and before Oct. 1, 2022, the indexed fee is $2.79.

- For plan years that end on or after Oct. 1, 2022, and before Oct. 1, 2023, the indexed fee is $3.00.

Self-funded plans have three options to determine the average number of covered individuals for reporting and paying the PCORI fee: (i) actual count method, (ii) snapshot method, or (iii) Form 5500 method. There are special rules for counting if employers offer multiple self-funded plans or have an HRA integrated with a fully insured plan. Additional information and payment instructions are available.

MHPAEA OPT-OUT EXPIRES

The Centers for Medicare & Medicaid Services (CMS) has issued guidelines regarding changes to the Mental Health Parity and Addiction Equity Act (MHPAEA) for self-insured non-federal governmental health plans.

The Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA) requires group health plans and health insurance issuers to ensure that financial requirements (such as co-pays, deductibles) and treatment limitations (such as visit limits) applicable to mental health or substance use disorder (MH/SUD) benefits are no more restrictive than the predominant requirements or limitations applied to substantially all medical/surgical benefits.

The new guidelines state that these health plans cannot choose to opt out of complying with the MHPAEA if they have not already done so by December 29, 2022. Additionally, any existing opt-out elections that expire 180 or more days after that date cannot be renewed.

However, there is a special rule for certain health plans that are collectively bargained. If a self-insured, non-federal governmental plan is subject to multiple collective bargaining agreements (CBAs) of different lengths and had an MHPAEA opt-out election in effect on December 29, 2022, which expires on or after June 27, 2023, the plan can extend the election until the last CBA expires. To do so, the plan needs to follow a specific process, including providing documentation of the effective date and duration of existing CBAs to CMS, obtaining CMS approval, and submitting a renewal opt-out election to extend the plan’s existing election.

The guidelines also emphasize that CMS has the authority to take enforcement action, such as imposing civil money penalties, against non-federal governmental health plans that do not comply with the MHPAEA requirements.

PREGNANT WORKERS FAIRNESS ACT GOES INTO EFFECT

Part of the Consolidated Appropriations Act, 2022, effective June 27, 2023, the Pregnant Workers Fairness Act (PWFA) requires employers with 15 or more employees to provide reasonable accommodations for job applicants and employees with known limitations related to pregnancy, childbirth and related medical conditions. The PWFA covers only accommodations and does not replace federal, state, or local laws that are more protective of workers. Existing laws enforced by the Equal Employment Opportunity Commission (EEOC) protect workers from discrimination or termination based on these conditions.

Reasonable accommodations must be made unless the accommodation would impose an undue hardship on the employer’s business operations.

Covered employers cannot:

- Require an employee to accept an accommodation without a discussion about the accommodation between the worker and the employer

- Deny a job or other employment opportunities to a qualified employee or applicant based on the person’s need for a reasonable accommodation

- Require an employee to take leave if another reasonable accommodation can be provided that would let the employee keep working

- Retaliate against an individual for reporting or opposing unlawful discrimination under the PWFA or participating in a PWFA proceeding (such as an investigation)

- Interfere with any individual’s rights under the PWFA

The EEOC will issue proposed regulations for comment before the final regulations take effect.

RXDC REPORT DUE TO CMS FOR 2022

The deadline for group health plans and plan issuers to submit information about prescription drugs and health care spending to the Department of Health and Human Services (HHS), the Department of Labor (DOL), and the Department of the Treasury was June 1, 2023, for the 2022 reporting year. Failure to comply with the reporting requirement may incur penalties of $100/day.

Although the reporting requirement is imposed on the group health plan, plan sponsors will certainly want to contract with the insurance carrier for fully insured plans and third-party entities such as their administrator for self-insured plans to provide the reporting on their behalf. Transferring the responsibility to an insurance carrier shifts the liability to the insurance carrier, but plan sponsors of self-insured plans remain liable for reporting assumed by a third-party entity.

FORM I-9 FLEXIBILITIES COME TO AN END

The COVID-19 flexibilities for employment eligibility verification through Form I-9 will end on July 31, 2023, according to U. S. Immigration and Customs Enforcement (ICE). The temporary flexibilities stated that employees hired on or after April 1, 2021, who worked exclusively in a remote setting due to COVID-19-related precautions were temporarily exempt from the physical inspection requirements of Form I-9 documentation. Employers will have until Aug. 30, 2023, to complete in-person physical document inspections for employees whose documents were inspected remotely. See I-9 Central Questions and Answers for more information.

QUESTION OF THE MONTH

Q: Is there a penalty for failure to file or pay the PCORI fee?

A: Although the PCORI statute and its regulations do not include a specific penalty for failure to report or pay the PCORI fee, the plan sponsor may be subject to penalties for failure to file a tax return because the PCORI fee is an excise tax. The plan sponsor should consult with its attorney about late filing or late payment of the PCORI fee. The PCORI regulations note that the penalties related to late filing of Form 720 or late payment of the fee may be waived or abated if the plan sponsor has reasonable cause and the failure was not due to willful neglect.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. |

| ©2023 United Benefit Advisors |

by admin | Jul 18, 2023 | Employee Benefits

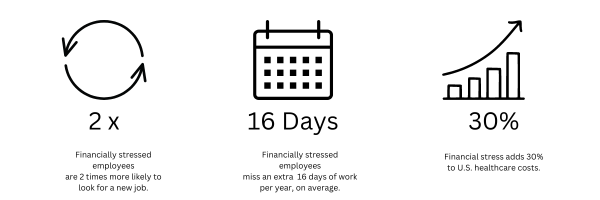

In the wake of the Great Depression and WWII, employers started to add benefits packages. Healthcare had fallen by the wayside for families working to access the basic necessities of life. The idea was to support the employee’s personal needs while keeping and attracting the best talents in the workforce. This trend of offering benefits has continued into the 21st century. In the present era, most employees that join the workforce are Millennials (born between 1981-1996) and Generation Z (born between 1997-2012). Over half of them have said they want help building a more secure financial future. Over half of them have said they want help building a more secure financial future.

Employee benefits play a crucial role in providing financial safety nets for employees. When employees experience less financial stress, employers see better employee productivity and fewer work absences. To aid with financial guidance and resources, many employers are offering financial wellness benefits beyond typical retirement plans. Here are some common financial safety nets that may be included in employee benefit packages:

- Retirement Plans: Employer-sponsored retirement plans, such as 401(k) or pension plans, enable employees to save for their post-employment years. These plans typically offer contributions from both the employer and employee, providing a safety net for financial stability during retirement.

- Disability Insurance: Disability insurance provides income replacement if an employee becomes unable to work due to a disability. It helps protect against loss of income during an extended period of absence from work. More disabilities are caused by illness rather than injury – including common conditions like heart disease, back pain or arthritis.

- Life Insurance: Life insurance offers financial protection to employees’ beneficiaries in the event of their death. It provides a lump sum payment or regular income to dependents, helping them cope with financial obligations.

- Paid Time Off (PTO): Paid leave policies, such as vacation days, sick leave, and personal days, offer employees the flexibility to take time off while still receiving their regular pay. This benefit supports employees during times of illness, personal emergencies, or the need for work-life balance.

- Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): FSAs and HSAs allow employees to set aside pre-tax dollars for qualified healthcare expenses or dependent care expenses. These accounts reduce the financial burden of medical or childcare costs.

- Tuition Reimbursement or Assistance Programs: Realizing student loans burden many employees, a growing number of employers are willing to offer help. Employers may also offer educational assistance programs to help employees pursue further education or skill development.

- Financial Education and Counseling: Employers may provide financial education programs and counseling services to help employees manage their finances effectively. Financial planning provides access to financial advisors who can help employees develop an overall financial plan including retirement savings and investing. Financial coaching helps employees manage their personal finances, such as budgeting and managing credit.

- Employee Assistance Programs (EAP): EAPs offer confidential counseling, mental health support, and resources to employees and their families. These programs help employees address personal and work-related challenges and promote overall well-being.

It’s important to note that the specific benefits offered by employers can vary widely. When it comes to benefits, employers know the cost of providing the best options pays off with better talent and more productive workers. Ultimately, having some financial safety nets in place for employees helps workers achieve their financial goals and save more of their hard-earned money for both expected and unexpected expenses.