by admin | Nov 20, 2023 | Health & Wellness

You may have heard the saying attitude of gratitude. It’s a great little rhyme to remind us to live a life of gratitude – and practice it! When we practice being thankful on a regular basis, it not only impacts our mental and physical health, but those around you as well.

The Definition of Gratitude

The emotion of gratitude is defined as “the quality of being thankful; readiness to show appreciation for and to return kindness.” We are familiar with the act of “thank you” to represent gratitude, but it also includes thinking on positive things that have happened during the day or your life, meditating on positive thoughts, and feeling grateful.

The Health of Gratitude

Beyond making someone feel appreciated, gratitude also has other benefits. In fact, there are physical health benefits associated with the act of gratitude. The Greater Good Science Center produced a list of benefits to gratitude.

For the individual:

- increased happiness and optimism for the future

- improved mental wellbeing

- greater satisfaction with life

- increased self-esteem

- better physical health

- better sleep

- less fatigue

- lower levels of cellular inflammation

- encourages the development of patience, humility, and wisdom

Research has shown that consciously practicing gratitude can reduce feelings of stress and anxiety. In fact, studies have found that a single act of thoughtful gratitude produces an immediate 10% increase in happiness and a 35% reduction in depressive symptoms. These effects disappeared within 3-6 months, which reminds us to practice gratitude over and over.

In addition to these above benefits, psychologically, the act of gratitude has been shown to reduce toxic emotions like envy, frustration, resentment, and regret. Those who focus on gratitude have even been reported to visit the doctor less!

The Act of Gratitude

So, how do you practice gratitude in your everyday life? Here are some easy-to-do exercises to strengthen your gratitude muscles:

- Say thank you

- Keep a gratitude journal or gratitude jar

- Write handwritten thank-you notes

- Think/meditate on positive thoughts

- Create gratitude rituals

- Put sticky notes around your home and workspace to remind you to be grateful

Our daily lives are fill of distractions and stress, and we often let our small achievements go unnoticed, even internally. Think about the past few days – what have you accomplished that went unnoticed? Did you cook a delicious meal, start a new book or chat with a loved one? Take a moment to celebrate that, to express gratitude for life’s everyday joys. Perhaps you might even write it down in a journal. This simple act that we’ve all been taught since we were born (Moms always remind you to say “thank you!”), has far-reaching benefits so start flexing your muscles of gratitude today.

by admin | Nov 14, 2023 | Health Insurance

Accidents happen. Whether you fall off a ladder, slip and break an arm, or get injured just living everyday life, an accident can happen. Anytime. Anywhere.

What Is Accident Insurance?

Accident insurance helps provide support when life’s most unexpected moments happen. It makes an accident less painful financially because it helps to pay the bills that your medical insurance doesn’t completely cover. It is important to understand that accident insurance is not intended to be a substitute for medical coverage. Instead, it is used as additional coverage and financial assistance.

Accident insurance may be offered by your employer as a voluntary benefit. Medical insurance doesn’t cover all of the expenses that result from an injury – you will likely owe a deductible and co-pays – and accident insurance helps fill in the gaps.

Examples of What Accident Insurance Covers:

- Emergency treatment and medical exams

- Hospital stays and surgical care

- Diagnostic tests such as X-rays and CAT scans

- Physical therapy and rehabilitation

- Family lodging and travel needs related to follow-up care

Examples of What Accident Insurance Does Not Cover:

- Injury due to extreme sports like bungee jumping or skydiving

- Self-inflicted wounds or suicide attempts

- Injury that occurs while doing criminal activities

- Injury that occurs while under the influence of drugs or alcohol

How Does Accident Insurance Work?

You pay a premium every month for coverage which is often automatically paid through payroll deductions. If you get injured, you submit a claim as well as any required verification for the accident. Then, once approved, the insurance payment will be sent directly to you – often in a one-time lump sum. Some plans pay out according to your expenses up to a maximum specified in the policy while others pay out a predetermined amount based on the injury.

One of the biggest advantages of accident insurance is that the payouts come in cash, which can relieve the financial burden after an injury. Additionally, there isn’t a waiting period, so you get the money immediately. This money is given to you in addition to what your health insurance pays. When you receive your payout, you can use the money to pay for any of your expenses – rent or mortgage payment, groceries, childcare, medical expenses, or other needs. How you use the payment after your injury is up to you as you recover.

No one wants to think accidents can happen, but they do. So, while life may dose out the accidents, remember there is insurance that can help.

by admin | Nov 9, 2023 | Compliance

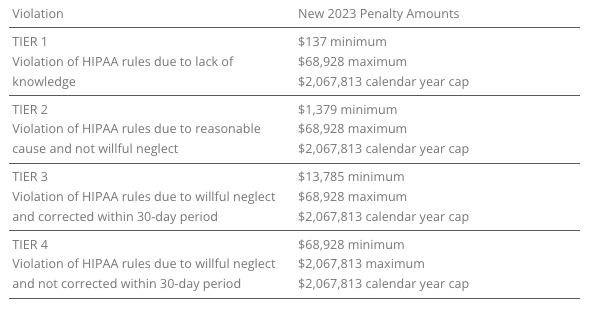

ADJUSTED CIVIL PENALTIES

The U.S. Department of Health and Human Services (HHS) has recently announced adjustments to civil penalties related to violations of the Health Insurance Portability and Accountability Act (HIPAA), the Affordable Care Act (ACA), and the Medicare Secondary Payer (MSP) rules. These penalty adjustments take into account inflation and are applicable to violations that occurred on or after November 2, 2015, and for which penalties are assessed on or after October 6, 2023.

HIPAA, which focuses on privacy and security rules, categorizes penalties based on the level of intention behind the violation.

The maximum penalty for failing to provide an SBC to eligible individuals before enrollment (or re-enrollment) in a group health plan has increased from $1,264 to $1,362.

The Medicare Secondary Payer (MSP) rules prevent employers from providing incentives to Medicare beneficiaries to waive or terminate primary group health plan coverage. The maximum penalty for not complying with MSP rules has increased to $11,162 from $10,360. Furthermore, the maximum penalty for failing to inform HHS when a group health plan is or was primary to Medicare has risen to $1,428 from $1,325.

EMPLOYER CONSIDERATIONS

To avoid these penalties, employers should carefully review their plan documents and operations to ensure compliance with the HHS-related requirements.

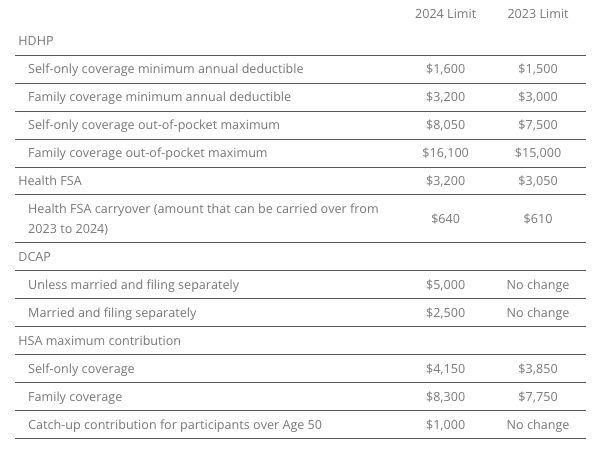

2023 LIMITS ANNOUNCED FOR HDHPS, HSAS, FSAS

The Internal Revenue Service (IRS) announced the new limits for high-deductible health plans (HDHPs), health savings accounts (HSAs), and Dependent Care Assistance Plans (DCAPs), and health flexible spending arrangements (FSAs). The new limits take effect beginning January 1, 2024.

MINNESOTA PAID SICK AND SAFE LEAVE LAW

Minnesota has recently passed a statewide paid sick and safe time leave law set to take effect on January 1, 2024. This law mirrors similar laws already in place in four Minnesota cities—Minneapolis, St. Paul, Duluth, and Bloomington. The key feature of the state law is the “front loading method,” which allows employers to provide employees with 48 hours of earned sick and safe time (ESST) in the first year of employment. Employers can pay out the value of unused hours at the end of the year and avoid carrying over unused hours into the next year.

EMPLOYER CONSIDERATIONS

This option provides flexibility for employers in managing employee leaves of absence. Local ordinances are not preempted by the state law, and employers must follow the most protective provisions of the state or local ordinances. The determination of which is more protective depends on whether more leave or monetary benefits are considered more beneficial for employees. See the FAQs for more information.

CALIFORNIA EXPANDS PAID SICK LEAVE

On October 4, 2023, Governor Gavin Newsom signed Senate Bill No. 616 into law, amending California’s paid sick leave regulations. The key changes introduced by SB 616 are:

- Starting January 1, 2024, California employers must provide employees with five days or 40 hours of paid sick leave, an increase from the previous requirement of three days or 24 hours.

- Employers can continue to provide paid sick leave at a rate of one hour for every 30 hours worked. If they use a different accrual rate, employees must accrue a minimum of 40 hours by their 200th day of employment and at least 24 hours by the 120th day of employment. Employers can also front load the entire paid sick leave amount.

- Employers may still limit the annual use of paid sick leave, but SB 616 increases the annual usage cap from 24 hours to 40 hours. The bill allows employers to cap paid sick leave accrual at 80 hours or 10 days, up from the previous limit of 48 hours or six days.

- While SB 616 continues to exempt certain collective bargaining agreement employees from the accrual requirement, it extends some provisions of California’s paid sick leave law to non-construction industry collective bargaining agreement employees. These employees may use paid sick leave for specific reasons, such as health-related issues or domestic violence, without facing retaliation. Employers cannot require these employees to find replacement workers when using sick days.

EMPLOYER CONSIDERATIONS

To comply with SB 616, employers are advised to review and update their paid sick leave policies to align with the new requirements and usage caps. Human resources and managers should also ensure proper implementation and adherence to the law.

QUESTION OF THE MONTH

Q: My wife and I work in the same small company. Is having her on my plan as spouse allowed? Can we both contribute separately from our own paychecks into our own Health Savings Account (HSA)? Or does it need to be my deduction only since I am the policy holder?

A: Yes, each spouse can have an HSA. The family limit, however, is divided between the two spouses, meaning the contributions to both HSAs combined cannot exceed the family HSA contribution limit.

Answers to the Question of the Week are provided by Kutak Rock LLP. Kutak Rock provides general compliance guidance through the UBA Compliance Help Desk, which does not constitute legal advice or create an attorney-client relationship. Please consult your legal advisor for specific legal advice.

| This information is general in nature and provided for educational purposes only. It is not intended to provide legal advice. You should not act on this information without consulting legal counsel or other knowledgeable advisors. |

| ©2023 United Benefit Advisors |

by admin | Nov 2, 2023 | Employee Benefits

The connection between employee wellness and the benefits of the job might seem obvious. But the conversation should be more nuanced than merely a discussion about health insurance, access to mental healthcare like employee assistance programs (EAPs), and well-being apps to reach zen.

Indeed, Human Resources professionals must reconsider their definition of benefits. It must extend to all the pros of working at a company. This includes the compensation and benefits packages but also other benefits like the team vibe, how managers treat employees, the expectations of employees, the ability for work-life balance, etc.

The New Human Resources

Thinking about this link between wellness and benefits is a key differentiator between traditional approaches to HR and the transformational employee-centric approach of the here and now. In the wake of the pandemic and the arrival of Gen Z employees to the workforce, expectations of employment have changed. HR must put emphasis on empathetic leadership, collegiality, and support for the health and wellness of the team for both recruiting and retention purposes.

HR’s Desire to Support Employee Wellness

The will to support employee mental health and wellness is there. Dating back to the State of HR 2022, when HR leaders who responded to the HR Exchange Network survey made employee engagement the top priority, organizations have been clamoring to improve recruiting, engagement, and retention. The foundation for this crusade is focusing on employee wellness. After all, at the heart of these efforts is job satisfaction.

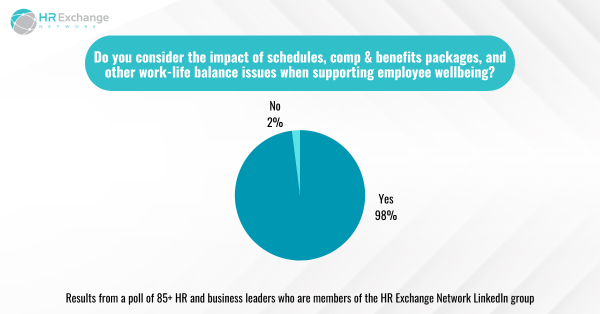

Many HR professionals have great intentions when considering a broader definition of benefits of a job. A whopping 98% of respondents to an HR Exchange Network LinkedIn poll say they consider the impact of schedules, compensation and benefits packages, and other work-life balance issues when supporting employee wellbeing.

Is HR Living Up to Its Ambition?

While most in HR say they want to help employees manage their mental health and wellness, they know employees might not have realized their efforts yet.

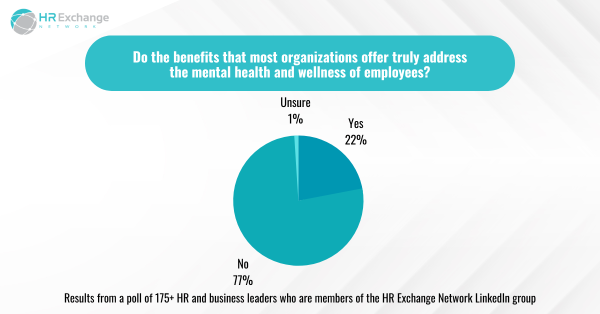

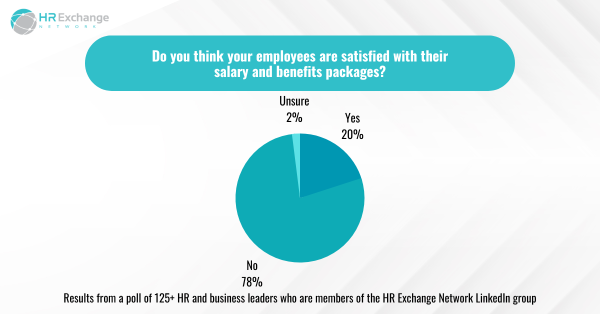

More than 75% – an overwhelming majority – of respondents to another HR Exchange Network LinkedIn poll said that the benefits most organizations offer do not truly address the mental health and wellness of employees. In addition, 78% in another poll on LinkedIn said employees were not satisfied with their salary and benefits packages.

Clearly, most in HR have more work to do when it comes to wellness and benefits. The first step would be to evaluate the company’s offerings. In 2022, respondents to the State of HR said the following were the top five benefits to offer or under consideration:

- Medical, dental, or vision insurance (55%)

- Wellness programs (53%)

- EAPs (45%)

- Mental health coaching (38%)

- Retirement savings (33%)

Worth noting, in the 2023 survey, 20% said they planned to invest in EAPs. In addition, the respondents of that survey shared their top priorities for addressing mental health and wellness:

- Creating a supportive environment for employees to talk about mental health concerns (40%)

- Implementing policies and procedures that address mental health in the workplace (37%)

- Providing accommodations for employees with mental health conditions (34%)

- Encouraging employees to take time off or seek medical attention (33%)

- Gyms/partnerships/fitness apps/fitness classes (27%)

Next Steps

Transformation requires effort and can be slow. Human Resources realizes that employees expect employers to support their mental health and wellness. Until now, that expectation – if ever met – was simply about offering the right kind of insurance and access to mental healthcare. Now, leaders and managers are meant to be empathetic and able to recognize those in need of help. Frankly, most have not had any sort of training, and it’s probably unfair to expect this of them. HR professionals are honest about the lack of support managers are receiving:

Presumably, the next step is to better train managers to provide mental health and wellness support and ensure the business builds itself around a people-centric culture. Certainly, the top priorities of HR professionals in 2023 suggest that employees are gaining leverage with HR:

- Developing and implementing diversity, equity, and inclusion (DEI) initiatives (22%)

- Improving employee engagement and retention (21%)

- Recruiting and retaining top talent (15%)

In fact, DEI is directly related to wellness at work because those efforts contribute to people feeling as though they are treated fairly and included. Providing that sense of belonging is an essential part of wellness, as is improving engagement and retention. To recruit and keep top talent, employers must continue to care for employees and lead HR with heart.

By Francesca Di Meglio

Orignally Posted on HR Exchange Network

by admin | Oct 25, 2023 | Employee Benefits, Health Insurance

Not understanding benefits terminology is near the top of the list of ways that open enrollment and benefits selection can stress you out. Open enrollment is coming quickly and soon you will be talking about benefit options. The world of benefits and insurance can be confusing. In-network, out-of-network, deductibles, co-pays and co-insurance? What?

Let us help break it down:

Premium – a monthly payment you make to your health insurance provider- it is the cost of having health insurance coverage. It’s perhaps the easiest component of a health plan – it’s the equivalent of a sticker price.

Here’s how it works: Coverage itself varies considerably from one health plan to another but in general, the less you pay for your coverage, the more you’re likely to have to pay when you need health care – and vice versa.

Co-insurance – A percentage of a health care cost—such as 20 percent—that the covered employee pays after meeting the deductible.

How it works: Let’s say you’ve paid $1,500 in health care costs and met your deductible. When you go to the doctor, instead of paying all costs, you and your plan share the cost. For example, your plan may pay 80% so then your share would be the remaining 20%.

Co-payment – The fixed dollar amount—such as $25 for each doctor visit—that the covered employee pays for medical services or prescriptions.

How it works: After your co-pay, your insurance picks up the rest of the bill for that visit. Co-pays typically count toward your annual out-of-pocket maximum (but there can be exceptions depending on your plan). The amount can vary depending on where you go for care, the type of doctor you see, and the type of prescription you are taking.

Deductible – How much you pay before your health insurance coverage kicks in. Your deductible resets every year.

How it works: If your plan’s deductible is $1,500, you’ll pay 100% of health care expenses until the bills total $1,500. After that, you share the cost with your plan by paying co-insurance.

Network – “In-network” refers to doctors and other health providers that are part of the insurer’s preferred network. Insurers sign contracts and negotiate prices with these in-network providers. This isn’t the case for “out-of-network” providers.

Here’s why that matters: Expenses you incur for services provided by out-of-network professionals may not be covered or may only be partially covered by your insurance; you will generally have a higher deductible and out-of-pocket limit when you see an out-of-network provider.

Out-of-pocket Maximum (OOPM) – the absolute most you pay in one year for your health care expenses before your insurance covers 100% of the bill.

Here’s how it works: What you pay toward your plan’s deductible, co-insurance and co-pays are all applied to your out-of-pocket max. If your plan covers more than one person, you will likely have a family out-of-pocket max and an individual out-of-pocket max. That means:

- When the deductible, co-insurance and co-pays for one person reach the individual maximum, your plan then pays 100% of the expenses for that person.

- When what you’ve paid toward individual maximums adds up to your family’s out-of-pocket max, your plan will pay 100% of the expenses for everyone on the plan.

Picking health insurance can be a dizzying adventure and making a mistake can be costly since you are generally locked into your health insurance for one year, with very limited exceptions. But when you understand how open enrollment works and how it impacts your family’s household budget, you can make wise, informed choices.