by admin | Feb 12, 2024 | Health Insurance

What is Health Insurance and Why is it Important?

Health insurance is a legal entitlement to payment or reimbursement for your health care costs, generally under a contract with a health insurance company. Health insurance provides important financial protection in case you have an accident or sickness. For example, health insurance may help to pay for doctors’ services, medications, hospital care, and special equipment when someone is sick or injured, often in exchange for a monthly premium. It may help cover a stay at a rehabilitation hospital or even a portion of home health care. Heath insurance can also keep a consumer’s costs down when they are not sick. For example, it can help pay for routine check-ups. Most health insurance also covers many preventive services at no cost, such as immunizations and cancer screening and counseling.

What is a Health Insurance Plan (also called a health plan or policy)?

A health insurance plan includes a package of covered health care items and services and sets how much it will pay for those items and services. In other words, a health plan will describe the types of health care items and services it will cover (help pay for), how much it will pay for those items and services (or groups of items and services), and for how long. Plans are often designed to last for a year at a time (known as a “plan year” or “policy year”). A health plan may be a benefit that an employer, union, or other group sponsor provides to employees or members to pay for their health care services.

What are Some Types of Health Care Coverage?

Health care coverage is often grouped into two general categories: private and public. The majority of people in the U.S. have private insurance, which they receive through their employer (which may include nongovernment employers or government employers at the federal, state or local level), buy directly from an insurance company, or buy through a Health Insurance Marketplace®.1 Some people have public health care coverage through government programs such as Medicare, Medicaid, or the Veteran’s Health Administration. Health care coverage can also be categorized by the scope of benefits it offers or how long the coverage lasts. Health insurance often includes a wide range of covered services, including emergency and nonemergency services as well mental health benefits. Some people have very limited insurance plans, such as plans with benefits for only specific conditions or diseases (included in the list of “excepted benefits” under the Affordable Care Act, such as vision-only plans or cancer plans).

As noted above, many health plans offer coverage for a year. However, some plans offer coverage for less than 12 months, including plans created to fill gaps in coverage. These plans are called short-term limited duration plans, and they often offer fewer benefits as compared to other health plans and lack some of the consumer protections available under other forms of coverage.

Self-Insured Employer Plans vs. Fully-Insured Plans

For consumers who receive health insurance through their employer, there are typically two different funding structures employers use to provide coverage:

- Some employers offer health care coverage to their employees through a self-insured plan. This is a type of health plan that is usually offered by larger companies where the employer collects contributions from employees via payroll deductions and takes on the responsibility of paying all related medical claims. These employers can contract with a thirdparty administrator (in some cases, a health insurance company acting as an administrator) for services such as enrollment, claims processing, and managing provider networks. Alternatively, these employers can self-administer the services. Self-insured plans are regulated by the federal government and are generally not subject to state insurance laws.

- A fully-insured employer plan is a health plan purchased by an employer from an insurance company. The insurance company, instead of the employer, takes on the responsibility of paying employees’ and dependents’ medical claims in exchange for a premium from the employer.

Originally posted on CMS.gov

by admin | Feb 6, 2024 | Hot Topics

Critical illness insurance is known by many names: heart attack insurance, catastrophic illness insurance and sick insurance are just a few. No matter what it’s called, it’s designed to guard against the financial costs of a serious disease or condition.

As the average life expectancy in the United States continues to increase, insurance brokers are finding ways to make sure Americans can afford the privilege of getting older. Critical illness insurance was developed in 1996, as people realized that surviving a heart attack or stroke could leave a patient with a mountain of medical bills.

Before you learn what critical illness insurance is, you should understand what it is not: medical insurance. This coverage is not meant to stand alone; it’s meant to be supplementary to other forms of coverage.

Critical illness insurance is simple – it provides a lump sum payment when you have a verified diagnosis of a covered illness. Critical illness insurance is offered as a voluntary benefit by some employers to supplement your regular medical coverage. You can use the critical illness benefit to pay for treatment, recovery or transportation costs associated with your illness, but unlike your existing health insurance, you’re not limited to medical costs. You can also use the money from a critical illness insurance policy to pay for a babysitter while you recover, utility bills, or however you see fit.

Common Critical Illnesses Covered

1. Cancer

2. Heart Attack

3. Stroke

4. Kidney Failure

5. Major Organ Transplant

Additional Illness and Conditions

Many policies also cover additional illnesses and conditions, such as Alzheimer’s Disease, Multiple Sclerosis, and severe burns.

Key Facts to Understand About Critical Illness Insurance:

- Critical illness insurance takes care of expenses that health insurance doesn’t normally cover and helps you meet your out-of-pocket costs

- Critical illness insurance only pays for certain conditions – you still need to rely on traditional health coverage for other illnesses

- You’ll receive just one large payment upon diagnosis, which may need to last for several years

- No networks, deductibles or co-payment

- Critical illness insurance does not cover pre-existing conditions

- Premiums become more expensive the older you are

- No restrictions on how you can use the funds, allowing you to choose what’s best for you

While it may not cover every disease, a critical illness insurance policy safeguards against many common and financially disruptive conditions. This coverage shields you from the impact of serious illnesses and unforeseen medical procedures by providing financial support for various needs—making up for lost wages, funding additional time off work, covering medical expenses, and even supporting travel for treatment. This support allows you to focus on the most important during this challenging time – getting better.

by admin | Feb 2, 2024 | Employee Benefits

The challenges that influenced the benefits landscape in 2023 persist—perhaps even more so. Rising costs, due to inflation and increasing health care prices, will continue to present challenges this new year. But employers who understand the benefits landscape for 2024 can mold their approach for the upcoming year.

A new year means revisiting your existing benefits strategy and looking at the top benefit trends:

Financial Wellness Benefits

Employees worry and stress about their finances and are searching for financial wellness education and guidance. Nearly 80% of employees say a financial wellness benefit is an important part of a comprehensive benefits package. Some of the popular financial wellness benefits are:

- Retirement Plan Options with Matching Contributions

- Health Savings Accounts

- Flexible Spending Accounts

- Financial Planning Assistance

- Flexible Paydays

- Employee Discount Program

- Financial Reimbursements (Ie. student loan repayment plans, child-care support funds and professional development stipends)

Voluntary Benefits

You can please some of the people some of the time, but you can’t please all the people all the time – unless you embrace voluntary benefits, that is. Voluntary benefits are optional perks that are offered to employees at a discounted group rate which their employer has negotiated with providers. While employees still need to pay to use these benefits, the amount is usually far less than it would be without company subsidies.

Moving forward, we can expect to see more sophisticated customization tools that allow employees to choose the benefits that best align with their individual circumstances and priorities. Whether it’s affordable veterinary insurance for pet owners, subsidized pre-K childcare for parents, or student loan repayment programs, offering these types of policies can directly improve the quality of life for employees who choose to take advantage of them.

Enhanced Family Benefits

Employers are increasingly looking to expand their family-friendly benefits for employees to better support employees in their caregiving roles.

- Paid family leave is not guaranteed by law in the U.S. but it is a highly sought-after perk. A parental leave policy – one that considers both parents and accounts for adoption and fostering in addition to childbirth – can show your employees you care about supporting their home lives.

- Childcare assistance supports working parents facing rising costs of living. While some larger employers may offer on-site childcare, smaller businesses can show their commitment to working parents by helping to subsidize the cost of childcare through employer contributions or pre-tax deductions.

- Fertility assistance supports employees who are going through costly infertility treatments, surrogacy, and IVF.

With four generations represented in the workforce, the support offered by employers can look different to Baby Boomers caring for their parents than a Millennial or Gen Zer caring for their children.

Inclusive and Flexible Care

The diverse workforce of 2024 is prioritizing a better work-life balance. It’s important to develop a benefits package that recognizes a healthy environment for your employees.

- Mental health benefits are in demand since mental health is a crucial part of overall health. Offering an employee assistance program (EAP) is a great way to support workers in tough situations.

- Work flexibility includes not only remote or hybrid work options, but you can also consider flexible start and stop times, a four-day work week or unlimited PTO to attract top talent and increase retention.

Overall, your benefits offerings for 2024 should reflect your organization’s values. Remember, your company depends on being able to keep your employees happy, healthy, and productive. Benefits that show respect for employees and promote a strong, vibrant culture are worth the investment.

by admin | Jan 15, 2024 | Hot Topics

As we begin to settle into 2024, many of us are thinking about New Year’s resolutions. The start of a New Year signals a time for change, reflection and a sense of ‘starting afresh’. This year, you can seize the new year’s spirit of renewal and make mental health your top priority!

A healthy mind will increase your self-esteem, attract positivity, and help you break those persistent bad habits. Don’t make the mistake of only writing ‘improve mental health’ on your New Year’s resolution list. To ensure success, you need to have a plan.

6 Tips to Improve Your Mental Health

Make a clear plan

Rather than attempting to overhaul several areas of your life, focus on one area at a time to maximize your chances of success. Checklists and timelines can help you track everything.

Set achievable health goals by making small, practical changes, like swapping out a meal or ingredient for a healthier option, rather than trying to quit all unhealthy foods at once.

Prioritize Sleep

Sleep is often the first thing to go. Poor sleep, especially over a period of a few weeks, leads to poor functioning: it impacts your immune system, ability to concentrate and your mood – all things that make you even more stressed out. It’s a vicious circle.

Prioritize “Me Time”

Taking some much needed “me time” isn’t selfish; taking care of yourself is one of the best mental wellness gifts you can receive. Do some yoga, take a walk, relax in the bathtub, or simply take some time to catch up on some reading. Your mental health will thank you for it.

Get Some Exercise

Exercise is an excellent way to destress. Focus on simply moving your body. Take the stairs or park your car further away from your destination to get some more steps in!

Enjoy Time with Friends and Family

Nurturing relationships with friends and family is crucial for a fulfilling life. Research shows that interacting with people we’re close to boosts our mood and makes us feel more connected. A strong support systems transforms challenges into manageable tasks and reassures you that you’re not alone.

Start a Gratitude Journal

Write down at least five things you’re grateful for and then reflect on why those things are important to you. It might be difficult at first, but the more you do it the easier it will become. You’ll find yourself feeling happier and more optimistic about life.

In a recent Forbes health survey, 50% of the respondents between the ages of 18 and 25 and 49% of those between 26 and 41 cited mental health as a top priority. Among respondents overall, 45% said improving their mental health was one of their top priorities.

Mental health is centered around the social and psychological aspects of our lives. Human beings are filled with complex thoughts and emotions — we are not preprogrammed to simply perform daily tasks. Our ability to think, feel, and navigate various experiences is tied to our mental state.

Good mental health gives us the resilience to process life’s challenges and helps us make wise decisions about the future. As you step into the new year, it’s essential to give your mental health the attention it deserves to ensure a balanced approach to your well-being.

by admin | Jan 8, 2024 | Employee Benefits

For most organizations, employee benefits communication kicks into high gear during open enrollment season. During this time, there is a surge in emails, educational webinars, fliers throughout the office, and a barrage of forms demanding signatures.

Post open enrollment, however, employees often receive minimal information about their benefits. While sporadic email updates or new laminated signs in the office kitchen may occur, a comprehensive, year-round employee benefits communication plan is often lacking.

This oversight represents a significant missed opportunity. An annual approach is insufficient to ensure that employees genuinely comprehend and effectively utilize their benefits.

When employers use a year-round approach to fully educate their employees on their benefits offerings, employees benefit both in their personal well-being and financial security. Employers also benefit from increased employee engagement, leading to a more creative work environment, reduced stress levels, higher employee retention rates, and potentially higher profitability. Establishing a year-round employee benefits communication plan is crucial.

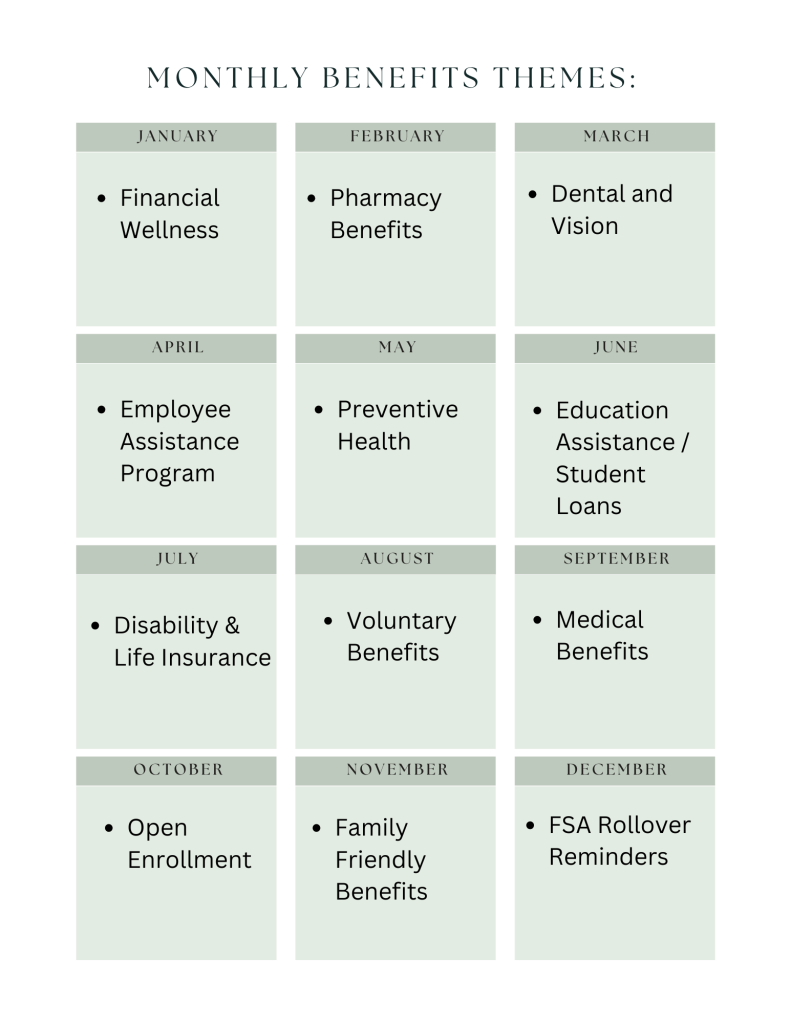

One way to establish an engaging year-round employee communication plan is through a calendar-based approach. Creating a monthly or quarterly calendar allows for the concentration on a series of topics related to benefits throughout the year. Q4 is the optimal period to highlight open enrollment, while the remaining three quarters provide an opportunity to dive into specific benefit categories such as health, lifestyle, and wealth.

Think about what will be on the top of employee’s minds over the next several months and create a calendar that speaks to those needs. Here is an example of a quarterly calendar:

Q1: In the beginning of the new year, the mantra is “New Year, New You!” What benefits can help employees plan for their future throughout the year – and take the stress out of the decision-making process?

Q2: With the weather beginning to warm up and the beginning of spring, many employees start to be more active and spend more time outdoors. What benefits address overall health and well-being?

Q3: Summertime means vacations for many families. This is a good time to address a healthy work-life balance and to give reminders about time off and childcare benefits.

Q4: When the weather starts to turn cooler, Q4 is in full gear! And that means one thing: Open Enrollment Season. Do your employees have the information to help them pick the right plan for the upcoming year?

Here is an example of some themes to incorporate into a monthly calendar:

Benefits education is communicating information about available benefits in ways that employees can connect to and understand. Communicating benefits information year-round is important because employees’ lives – and their situations – are constantly changing. They get married, divorced, adopt a child or have medical challenges arise. They are thinking about their health and financial security and how to adapt to it. If employees are engaged with their benefits throughout the year, they are more likely to value and use their benefits and will be better informed about their decisions and/or changes they need to make during the next Open Enrollment period!